Emerging Market Links + The Week Ahead (December 5, 2022)

Apple shifting out of China, Bimchip (Brazil, India, Mexico, Chile, Indonesia & Peru), South Africa's Farmgate scandal, South Korea + Taiwan, Robeco's EM case and the week ahead for emerging markets.

Apple possibly planning to shift production out of China (and to ship up to 45% from India) would be another nail in their economic coffin and a further reason for emerging market investors to start shifting attention to other countries. And one strategist has come up with yet another catchy acronym for EM investors: Bimchip - as in Brazil, India, Mexico, Chile, Indonesia and Peru.

Meanwhile, South African President Ramaphosa’s “farmgate” scandal threatens to further damage the country’s political and economic stability as a divided ANC decides what to do about him. The scandal appears to center on “donations” involving regimes or individuals based in multiple countries - Saudi Arabia, Qatar and Equatorial Guinea. [LIVE BLOG: Phala Phala Farmgate fallout - What will President Cyril Ramaphosa's next move be?]

Finally, I recommend watching Sleeping giants – the case for emerging markets - a 47 minute roundtable discussion (plus a Q&A for questions submitted by listeners) webinar from Robeco who (maybe because they are also Dutch) I find to usually be a no-nonsense research provider. Although the short webinar summary talks up the [obligatory] ESG [nonsense!], there was limited “sustainability” talk in the webinar itself - just useful investing tips for emerging market investors to consider (which I have summarized below).

Suggested Reading

$ = behind a paywall

Apple Makes Plans to Move Production Out of China (WSJ)

Apple has accelerated plans to move its productions outside Zhengzhou, China - where iPhone City is located - in recent weeks

COVID-19 protests and wage disputes have broken out in the city, leaving Apple's busiest time of year in shambles with production and delivery delays

Consumers are facing the longest wait times in the iPhone's 15-year history

It is now eyeing India and Vietnam to reduce its dependency on Taiwanese-based assemblers led by Foxconn Technology Group, which runs the factory

Apple is hoping, long-term, to ship up to 45 percent from India, which currently only does single digits, and Vietnam could handle AirPods and laptops

Variant view: China's zero-COVID policy is dead (Asian Century Stocks Substack)

NOTE: Good objective overview of recent events in China surrounding zero-COVID and associated protests.

The sectors that have suffered the most from China’s zero-COVID policy are consumer related. Consumer spending has been weak, especially regarding offline retail, restaurants and so on. These businesses are likely to recover at some point.

The transportation sector has also been weak. Toll road volumes, airport passenger numbers and railway ridership are still much lower than they were before the pandemic. I expect mean reversion as restrictions lift in the next few months or quarters.

I believe that oil demand will also shift upwards as air travel resumes and cars get back on the road. This will have implications for oil & gas producers as well retailers of gasoline.

Emerging & Global Markets Catch Up With Reality (Krane Shares)

[NOTE: This is from mid-November - so its already dated but the points below are worth noting.]

First, we have seen very little internet regulation over the summer, confirming a possible end to reforms.

Second, the China Securities Regulatory Commission (CSRC) and the Securities Exchange Commission (SEC) have signed a statement of protocol allowing the Public Company Accounting Oversight Board to conduct full audit reviews of US-listed Chinese companies, which should lift investor sentiment toward China.

US officials are currently in Hong Kong auditing the data of more than 160 Chinese companies. We believe all the major internet companies will pass the test and help to establish a path to the final agreement.

Third, we believe the conclusion of the National Party Congress (NPC) on October 22nd,5 may allow leaders to focus on supporting the real economy once again and potentially pursue more easing of China's zero COVID policy.

Fourth, CSPC Pharma, China's third largest pharmaceutical company, announced favorable numbers for their mRNA COVID vaccine, potentially leading to emergency approval as soon as November.

Lastly, for the first time since 2019, China brought back the Pledged Supplementary Lending (PSL) program in October. The program was created in 2014 and is meant to capitalize policy banks to support the property sector. The return of the discontinued program indicates that China is looking to bring the real estate sector under control in the near term and protect against systematic risk.

Sustained growth slowdown in China would spill over to Asia-Pacific region and beyond (Moody’s Talk) 10 Minutes

Emerging Markets Decoded, Deborah Tan of the Credit Strategy & Research team joins host Shirin Mohammadi to discuss what a sustained economic growth slowdown in China implies for the rest of the world, particularly the Asia-Pacific region and lower-income countries that rely on Chinese investment flows.

China faces a cyclical downturn that could turn structural and end up centred on these medium to long term problems: 1) Demographics (lower labor force participation due to an aging population), 2) Regulatory uncertainty (leading to lower private investment), and 3) Trade (less global trade and the re-routing of trade alliances).

Japan, Korea and Taiwan would have high manufacturing supply chain exposure to China. SE Asia countries like Malaysia, Singapore, Indonesia and Thailand would have moderate to high exposure in certain areas while Australia and Mongolia have high commodities exposure.

In long term absolute return portfolio, I have about 20 stocks which are still dominantly India: Chris Wood (The Economic Times)

“Tactically, there is definitely a good case to reduce India and add to China but structurally, I still remain firmly of the view that India is the best story in a 10-year view in Asian emerging market equities,” says Chris Wood, Global Head of Equity Strategy, Jefferies

“My relative return is marginally overweight China and India. But in my long term absolute return portfolio, I have about 20 stocks which are still dominantly India because that is long term. The more short-term you are, the more you should want to be underweight in India. The more long term you are, stay structurally overweight. It all depends on your time horizon.”

Emerging market investors: drop a Bric and pick up a Bimchip (Financial Times)

My view is that investors should embrace a more targeted approach by picking specific countries or, at the very least, invest in funds run by people who will do that active allocation between countries in an intelligent fashion. Mobius and Templeton spring to mind.

I would also suggest two distinct opportunities. First, aim for a select band of countries that actually outperformed their peers in the past year of crisis; second, put EM bonds on your radar.

He [Vincent Deluard, a strategist at StoneX, a trading services company] suggests ditching old-fashioned terms such as the Brics and Gems (global emerging markets) and embracing your inner Bimchip. This dreadful acronym embraces the idea that you only invest in the following countries: Brazil, India, Mexico, Chile, Indonesia and Peru.

I’d suggest the following combination of actively managed investment trusts and country specific exchange traded funds.

Brazil, Peru and Chile: Abrdn Latin American Income and BlackRock Latin America

India: India Capital Growth and Ashoka India Equity

Mexico: Xtrackers MSCI Mexico UCITS ETF 1C, ticker XMEX

Indonesia: HSBC MSCI Indonesia UCITS ETF USD, ticker HIDR

Asian tigers: South Korea and Taiwan (Franklin Templeton)

South Korea and Taiwan strongly outperformed most of their peers quarter-to-date.

A strong US dollar and receding energy prices support solid macroeconomic fundamentals of export-oriented economies.

Optimism is further spurred by what we consider attractive valuations, positive outlook for the chip and materials industries despite the current demand slump.

Long-term supply-chain realignments could benefit both economies.

The primary factors driving the recent surge in relative performance appear to be: 1) Investor bargain hunting, 2) Semiconductor chips and electric vehicles (EV) market optimism, 3) Strong fundamentals

Bloodbath for banks on JSE as Ramaphosa uncertainty weighs (Business Report)

The news sent shock waves through the local markets and put the rand under pressure as Ramaphosa, investors’ preferred candidate for president, is now facing possible removal.

Anchor Capital’s co-chief investment officer Nolan Wapenaar said stocks could trade weaker for a prolonged period because of uncertainty.

Business Leadership SA said the fact that allegations against Ramaphosa had been investigated was a positive sign of the health of South Africa’s democracy and its institutions.

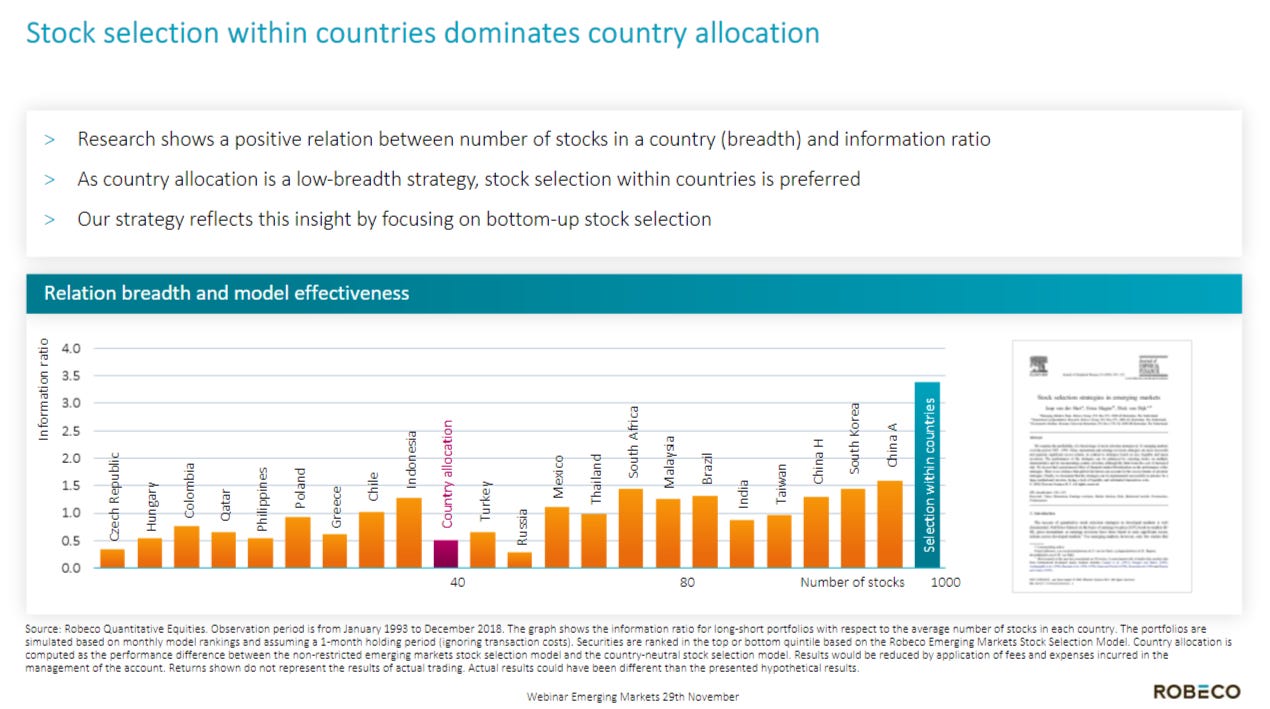

Sleeping giants – the case for emerging markets (Robeco Webinar) 47 Minutes

NOTE: You need to register to see the replay.

What ‘sleeping giant’ countries, sectors and companies offer the best picks

Why sustainability is vital when assessing risks in emerging market economies

How quant techniques can be applied to lower volatility or relative risk

Stock selection is key, but you can still make money from the right country allocation. You also need to look beyond short term volatility and “stick to your guns.”

Defensive value stocks e.g. stocks (like telcos, consumer etc) you don’t see in the news who are in the business to survive rather than disrupt.

Reliance on foreign capital has come down tremendously.

Currencies are an outcome of underlying macro economic variables and they are also “silent assassins.” So you need to be comfortable with the currency. Over the last 30 years, you would have lost 3% of your return per year due to currency movements.

You have to be “out of your mind” to do passive in emerging markets when active has won hands down (e.g. China).

Sustainability data is inconsistent and unreliable - making sustainable investing more challenging.

Their big allocations are in China, South Korea, Taiwan, India and Brazil. Vietnam is one of the frontier markets they have entered.

Countries with no domestic investors will be at the mercy of foreign investors and their opinion of the country (e.g. China has negative international opinion right now but many local investors).

Earnings Calendar

Note: Investing.com has a full calendar for most global stock exchanges BUT you may need an Investing.com account, then hit “Filter,” and select the countries you wish to see company earnings from. Otherwise, purple (below) are upcoming earnings for US listed international stocks (Finviz.com):

Economic Calendar

Click here for the full weekly calendar from Investing.com containing frontier and emerging market economic events or releases (my filter excludes USA, Canada, EU, Australia & NZ).

Election Calendar

Frontier and emerging market highlights (from IFES’s Election Guide calendar):

Fiji Fijian House of Representatives Dec 14, 2022 (d) Date not confirmed

Tunisia Tunisian Assembly of People's Representatives Dec 17, 2022 (d) Confirmed Oct 6, 2019

Nigeria Nigerian House of Representatives Feb 25, 2023 (d) Confirmed Feb 23, 2019

Nigeria Nigerian Senate Feb 25, 2023 (d) Confirmed Feb 23, 2019

Check out:

IPO Calendar/Pipeline

Frontier and emerging market highlights from IPOScoop.com and Investing.com (NOTE: For the latter, you need to go to Filter and “Select All” countries to see IPOs on non-USA exchanges):

Erayak Power Solution Group Inc. RAYA, 3.0M Shares, $4.00-4.00, $12.0 mil, 12/7/2022 Wednesday

Erayak Power Solution Group Inc. was formed in 2019 under the laws of the Cayman Islands. We conduct business primarily through our wholly owned subsidiaries, Zhejiang Leiya and Wenzhou New Focus, in the People’s Republic of China, or the PRC. Our company specializes in the manufacturing, research and development (“R&D”), and wholesale and retail of power solution products. Zhejiang Leiya’s product portfolio includes sine wave and off-grid inverters, inverter and gasoline generators, battery and smart chargers, and custom-designed products. Our products are customized and built to order, or BTO. Our BTO business model maximizes our flexibility in production scheduling, material procurement and delivery to meet our customers’ unique demands.

Our products are used principally in agricultural and industrial vehicles, recreational vehicles (“RVs”), electrical appliances and outdoor living products. Our primary office is located in Zhejiang province, where we serve a large customer base throughout PRC and expand our reach to international clients. Our goal is to be the premier power solutions brand and a solution for mobile life and outdoor living. We seek to leverage our flexibility and passion for quality to provide a personalized mobile living solution for each customer.

Since the founding of Zhejiang Leiya in 2009, it has grown to be a manufacturer that not only designs, develops and mass produces our own brand of premium power solution products, but has also established e-commerce channels in the retail chain. We, through our PRC subsidiaries, also offer our products in Japan, England, Germany, France, Spain, Switzerland, Sweden, the Netherlands, the U.S., Canada, Mexico, Australia, Dubai and nine other countries. Zhejiang Leiya manufactures all of our products in factories operating under quality management systems accredited by the International Organization for Standardization (ISO 9001:2015).

CBL International Limited BANL, 3.8M shares, $4.00-4.80, $16.7 mil, 12/16/2022 Friday

We are an established marine fuel logistics company providing a one-stop solution for vessel refueling, which is referred to as bunkering facilitator in the bunkering industry, in the Asia Pacific. (Incorporated in the Cayman Islands)

We purchase and arrange our suppliers to actually deliver marine fuel to our customers, some of which we provide certain credit term of payment while we also receive payment credit from our suppliers. We rely on the permits and licenses of our suppliers for the actual delivery of marine fuel at each port. Since the establishment of our Group in 2015, container liner operators have been identified as our target customers. Container liner operators provide liner services which operate on a schedule with a fixed port rotation and fixed frequency, which is similar to bus operation under which buses go on fixed routes and calling at fixed stops for passengers to board and alight. Knowing the nature of the business of our target customers, we continually look to broaden our operations by (a) expanding our servicing network to cover more ports; and (b) providing more value-added services to tailor for our customers’ growing demands with respect to vessel refueling.

Our operations are based in Malaysia, Hong Kong and Singapore, but nearly all of our revenues were generated from China and Hong Kong (based on the location at which the marine fuel is delivered to the customer). For FY2020, FY2021 and the six months ended June 30, 2022, revenue generated from services provided in ports in China and Hong Kong accounted for a total of 88.8%, 95.9% and 92%, respectively, of our total revenue; whilst revenue generated from services provided in ports in Malaysia and Singapore accounted for a total of 10.7%, 2.9% and 7%, respectively, of our total revenue. Although we deliver our services mainly in China and Hong Kong, nearly all our customers are international container liner operators from outside of China and Hong Kong: of our five largest customers from whom we generated 92.9%, 83.6% and 77% respectively of our total revenue for FY2020, FY2021 and the six months ended June 30, 2022, three customers are Taiwanese companies, one is a German company, and one is a Singaporean company.

ParaZero Technologies Ltd. PRZO, 1.6M Shares, $4.25-6.25, $8.4 mil, 12/16/2022 Friday

(Note: This is a unit IPO again – as of its F-1/A filing dated Nov. 3, 2022 – with each unit consisting of one share of common stock and two warrants – each to buy a share of common stock. See notes at the end of the IPO Profile on the the updated terms and the history of filings.)

We are an aerospace company that is focused on drone safety systems and engaged in the business of designing, developing, and providing what we believe are best-in-class autonomous parachute safety systems for commercial drones, also known as unmanned aerial systems or UAS. (Incorporated in Israel)

Our company was founded by a group of aviation professionals, together with veteran drone operators, to address the drone industry’s safety challenges. Our goal is to enable the drone industry to realize its greatest potential through increasing safety and mitigating operational risk.

Our unique patented technology for drones, the SafeAir system, is designed to protect hardware, people and payload in the event of an in-flight failure. The SafeAir system is a smart parachute system that monitors UAS flight in real time, identifies critical failures and autonomously triggers a parachute in the event that certain parameters indicative of a free fall are present. The system contains a flight termination system, a black box to enable post-deployment analysis, and a warning buzzer to alert people of a falling drone. In addition to being fully autonomous, the SafeAir system includes a separate remote control for manual parachute deployment capability.

We have a global distribution footprint and have forged partnerships all around the world, including India, South Korea, the United States, Latin America and Europe. We sell our drone safety systems as off-the-shelf solutions, as well as perform integrations with original equipment manufacturers, or OEMs, offering customized, bespoke safety solutions for a large variety of aerial platforms.

Our technology has been sold to and used by some of the world’s top companies and organizations, including drone companies such as LIFT Aircraft, Airobotics, SpeedBird Aero and Doosan Corporation, and other leading brands such as CNN, The New York Times, Hensel Phelps, Verizon Media (Skyward), Fox Television, the Chicago Police Department and Fortis Construction.

ETF Launches

Climate change and ESG are clearly the latest flavours of the month for most new ETFs. Nevertheless, here are some new frontier and emerging market focused ETFs:

9/22/2022 - WisdomTree Emerging Markets ex-China Fund XC - Passive, equity, emerging markets

9/15/2022 - KraneShares S&P Pan Asia Dividend Aristocrats Index ETF KDIV - Passive, equity, Asia, dividend strategy

9/15/2022 - OneAscent Emerging Markets ETF OAEM - Active, Equity, emerging markets, ESG

9/9/2022 - Emerge EMPWR Sustainable Select Growth Equity ETF EMGC - Active, equity, emerging markets

9/9/2022 - Emerge EMPWR Unified Sustainable Equity ETF EMPW - Active, equity, emerging markets

9/8/2022 - Emerge EMPWR Sustainable Emerging Markets Equity ETF EMCH - Active, equity, emerging markets, ESG

7/14/2022 - Matthews China Active ETF MCH - Active, equity, China

7/14/2022 - Matthews Emerging Markets Equity Active ETF MEM - Active, equity, emerging markets

7/14/2022 - Matthews Asia Innovators Active ETF MINV - Active, equity, Asia

6/30/2022 - BondBloxx JP Morgan USD Emerging Markets 1-10 Year Bond ETF XEMD - Passive, fixed income, emerging markets

5/2/2022 - AXS Short CSI China Internet ETF SWEB - Active, inverse, thematic

4/27/2022 - Dimensional Emerging Markets High Profitability ETF DEHP - Active, equity, emerging markets

4/27/2022 - Dimensional Emerging Markets Core Equity 2 ETF DFEM - Active, equity, emerging markets

4/27/2022 - Dimensional Emerging Markets Value ETF DFEV - Active, equity, emerging markets

4/27/2022 - iShares Emergent Food and AgTech Multisector ETF IVEG - Passive, equity, thematic [Mostly developed markets]

4/21/2022 - FlexShares ESG & Climate Emerging Markets Core Index Fund FEEM - Passive, equity, ESG

4/6/2022 - India Internet & Ecommerce ETF INQQ - Passive, equity, thematic

2/17/2022 - VanEck Digital India ETF DGIN - Passive, India market, thematic

2/17/2022 - Goldman Sachs Access Emerging Markets USD Bond ETF GEMD - Passive, fixed income, emerging markets

1/27/2022 - iShares MSCI China Multisector Tech ETF TCHI - Passive, China, technology

1/11/2022 - Simplify Emerging Markets PLUS Downside Convexity ETF EMGD - Active, equity, options strategy

1/11/2022 - SPDR Bloomberg SASB Emerging Markets ESG Select ETF REMG - Passive, equity, ESG

ETF Closures/Liquidations

Frontier and emerging market highlights:

12/21/2022 - VictoryShares Emerging Market High Div Volatility Wtd ETF CEY

8/22/2022 - iShares MSCI Argentina and Global Exposure ETF AGT

8/22/2022 - iShares MSCI Colombia ETFI COL

6/10/2022 - Infusive Compounding Global Equities ETF JOYY

5/3/2022 - ProShares Short Term USD Emerging Markets Bond ETF EMSH

4/7/2022 - DeltaShares S&P EM 100 & Managed Risk ETF DMRE

3/11/2022 - Direxion Daily Russia Bull 2X Shares RUSL

1/27/2022 - Legg Mason Global Infrastructure ETF INFR

1/14/2022 - Direxion Daily Latin America Bull 2X Shares LBJ

Check out our emerging market ETF lists, ADR lists (updated) and closed-end fund (updated) lists (also see our site map + list update status as some ETF lists are still being updated as of Summer 2022).

I have changed the front page of www.emergingmarketskeptic.com to mainly consist of links to other emerging market newspapers, investment firms, newsletters, blogs, podcasts and other helpful emerging market investing resources. The top menu includes links to other resources as well as a link to a general EM investing tips / advice feed e.g. links to specific and useful articles for EM investors.

Disclaimer: EmergingMarketSkeptic.Substack.com and EmergingMarketSkeptic.com provides useful information that should not constitute investment advice or a recommendation to invest. In addition, your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content.

Emerging Market Links + The Week Ahead (December 5, 2022) was also published on our website under the Newsletter category.