Emerging Market Links + The Week Ahead (June 19, 2023)

Demand grows for investment products excluding China, Chinese HNWIs leave, Taiwan earnings season tech insights, India poised for LT growth, Mexico’s Bull Run & the week ahead for emerging markets.

The FT has noted how there is growing demand for Asian investment products that exclude China as history repeats itself e.g. thirty years ago, the size and volatility of the post-bubble Japanese market skewed Asian portfolios too much. This led to the creation of ex-Japan funds and indices.

Today, more investors have realized China’s weight in the indices is far too large. Add geopolitical tensions and the weakening Chinese economy, and many foreign investors are already heading for the exits (or, if they are MNCs, are looking for ways to “ringfence” their China businesses with separate listings, etc) - or looking for exposure to China via other markets.

And its not just foreign investors heading for the exits. The just released Henley Private Wealth Migration Report 2023 is forecasting for China to loose another 13,500 HNWIs or millionaires this year - up from an estimated 10,800 for last year.

Finally, I have fixed the website (but I may still need to deal or tweak some things such as old links, mobile appearance plus make sure the security certificate keeps working so visitors don’t get scary browser warnings) - its now much cleaner and loads much faster. On the mostly static front page, all the links to relevant emerging market investment firms, research, newspapers, podcasts, Substacks, YouTube channels, etc. are back (let me know if I missed any good resources…) plus the menu has more resources (which appears as a hamburger or accordion on mobile…).

An IT friend had commented to me:

The speed of changes in frontend development is so fast, it's also frustrating. So whatever system you set up nowadays, in a couple of years, the chances are high, that the website won't run anymore because of either security reason or out-of-date code. So you need to constantly keep s**t up-to-date. Unless you run a old-fashioned static html site.

Emerging Market Stock Pick Tear Sheets

$ = behind a paywall

CMBI Research Focus List of China Stock Picks (June 2023)

Includes: Li Auto, Great Wall Motor, Zoomlion Heavy Industry, Yancoal Australia, SANY International, CR Gas, Xtep, Yum China, Xiabu Xiabu Catering (XBXB), Midea, CR Beer, Tsingtao, Prada SpA, Kweichow Moutai, Innovent Biologics, AK Medical, AIA, Tencent, Pinduoduo, NetEase, Alibaba, Kuaishou, CR Land, BOE Varitronix, Wingtech & Kingdee

Emerging Market Stock Pick Tear Sheets (June 1-18, 2023)

Includes: LG Chem, LG Energy Solution, SK Innovation, SMIC, NAURA Technology Group, Hua Hong Semiconductor, AMEC, CATL, Legend Biotech, ACM Research, Mercurity Fintech Holdings, Fangdd Network, etc. Plus CMBI's Chinese & Mirae Asset Securities' Korean stock picks.

Emerging Market Stock Picks / Stock Research

$ = behind a paywall

Hidden champions among China's ADRs (Asian Century Stocks) $

I’ve identified 12 companies among China’s ADRs that qualify as “hidden champions” - companies that dominate their niches and enjoy strong competitive advantages. While frauds are common, I’ve tried to exclude them from the list.

Note: The actual stock picks are behind a paywall, but this table is useful:

LINK REIT – the Largest REIT in Asia, Firmly on a Post-Covid Recovery with Attractive Valuation (Smart Karma) $

Note: Link Real Estate Investment Trust (HKG: 0823 / STU: L5R / OTCMKTS: LKREF) is the first REIT in Hong Kong and currently the largest in Asia.

We conducted fundamental analysis on Link REIT, the largest REIT In Asia, who owns and operates retail assets, office buildings and logistics in the APAC region

Link REIT has strong track record for capital management, we expect that to continue. In the LT, Link REIT is on the path to grow its fund management business

Link REIT is currently trading at 0.64x P/B and 6% dividend yield, which is attractive from a historical perspective

Taiwan Tech: Insights from 1Q23 Earnings Season Into Where We Are in the Cycle (Smart Karma) $

Note: Also see our Taiwan ADRs list.

Our aggregate analysis of the 1Q23 earnings season showed a more balanced beat/miss ratio than 4Q22 likely due to already-downgraded forecasts presenting a lower expectations hurdle.

Semiconductor's inventory situation overall appeared to get worse in 1Q23... Excess inventory digestion is still a few quarters away for many semiconductor companies. Margins fell to the last cycle lows.

Hardware showed small signs of overall inventory improvement. Margins fell further but remained pretty high relative to the previous cycle.

Moody’s downgrades NagaCorp’s rating on refinancing woes (GGRAsia)

Note: NagaCorp (HKG: 3918 / FRA: N9J / OTCMKTS: NGCRF) has a long-life monopoly casino licence for the Cambodian capital, Phnom Penh, where it operates its NagaWorld resort complex.

“The rating downgrade and negative outlook reflect NagaCorp’s lack of refinancing progress for its US$472 million U.S. dollar bond coming due in July 2024. The bond forms all of the company’s debt in its capital structure,” said Moody’s analyst Yu Sheng Tay, as cited in the report.

“Despite NagaCorp having reduced its discretionary spending, its ability to repay the bond depends on the pace of earnings recovery, which currently remains uncertain,” added the analyst.

Moody’s stated that there was “increased likelihood of a distressed exchange as funding conditions for Asian high-yield companies remain tight”.

“NagaCorp has limited liquidity sources, given its lack of bank facilities and divestible non-core assets,” it added.

Uchi Technologies (UCHI MK): Coffee and Cash Machine (Smart Karma) $

Uchi Technologies (KLSE: 7100), a manufacturer of controllers for coffee machines, has a 23-year track record of operating margins of over 40% and ROCEs of over 20%.

Trading at 11.9x trailing PE, with a dividend yield of 9%, and 15% of the market cap in cash, the company has been serially paying dividends (payout > 70%).

In its 2022 annual report, for the first time in its history, the company mentioned it has exciting growth plans that will be revealed over the year.

"Uchi Technologies is a company that has a fabulous track record of 40% operating margins and 20% ROCEs over the last 23 years. It's a great stock, trading at 11.9x PE trailing with a 9% div yield." - Sameer Taneja

GEN Malaysia shareholders nod US$1.2bln sale of Miami land (GGRAsia)

Genting Malaysia (KLSE: GENM) has for some time been identified as a likely suitor for a downstate casino licence in New York. The New York State Gaming Commission in January launched a request for applications (RFA) process for three downstate New York gaming licences.

A number of investment analysts has suggested that Genting group could be a front-runner there. It already runs an electronic games facility called Resorts World Casino New York City; and has investment in Empire Resorts Inc, which runs the full-service casino Resorts World Catskills, in upstate New York.

Indonesia's United Tractors to buy $633m stake in Australian miner (Nikkei Asia) (Archived Article)

Note: The Nickel Industries investor presentation about the deal is here. Astra is controlled by Hong Kong’s Jardine Matheson (SGX: J36 / FRA: H4W / OTCMKTS: JARLF).

Top conglomerate Astra International (IDX: ASII / FRA: ASJA / OTCMKTS: PTAIF) seeks entry into EV battery materials

Indonesian heavy equipment distributor United Tractors (IDX: UNTR / FRA: UTY) on Friday announced the signing of an agreement to acquire a stake in Australia-listed Nickel Industries (ASX: NIC / FRA: NM5 / OTCMKTS: NICMF) -- an affiliate of Chinese stainless steel giant Tsingshan Holding -- for 943 million Australian dollars ($633 million).

United Tractors is the heavy equipment and mining arm of top Indonesian conglomerate Astra International. The share subscription agreement marks a plan for a major foray by Astra into the nickel and electric vehicle battery sector. Astra's business units include local assembling and distribution of Japanese cars and motorcycles.

Beximco Pharma GDR (Emerging Value) $

Beximco Pharma (LON: BXP / FRA: R2WA) is a Bangladeshi company. It has a global deposit receipt trading in London, It is very cheap and had growth in the past decade. However, the current year has seen performance worsen, as the Bangladesh local currency, the Taka crashed, and elevated covid pharmaceutical sales in the previous years.

“Beximco Pharma currently produces more than 300 generic medicines which are available in well over 500 different presentations and the broad portfolio encompasses all key therapeutic categories including antibiotics, analgesics, anti-diabetic, respiratory, cardiovascular, central nervous system, dermatology, gastrointestinal etc.”

Glencore, automakers to back $1 bln nickel, copper SPAC deal in Brazil (Reuters) (Archived Article)

Global miner Glencore (LON: GLEN / JSE: GLN / FRA: 8GC / OTCMKTS: GLNCY / OTCMKTS: GLCNF), Chrysler parent Stellantis (STLAM.MI) and Volkswagen's (VOWG_p.DE) battery unit PowerCo have agreed to back a $1 billion deal by blank-cheque fund ACG Acquisition Company to buy two mines in Brazil, ACG said on Monday.

ACG Acquisition Company (LON: ACG / FRA: Y9C), a London-listed special purpose acquisition company (SPAC), will buy the Santa Rita nickel sulphide and Serrote copper mines from private equity funds advised by Appian Capital…

Diageo - A Taste of Success in the Beverage Industry (StockOpine’s Newsletter)

Further Suggested Reading

$ = behind a paywall

Henley Private Wealth Migration Report 2023 (Henley & Partners)

Note: Press Release, Dashboard (HNWI Global Migration, Country Inflows/Outflows & Country Benchmarking), Global Insights, Regional Insights (North America, UK and Europe, South Africa, Middle East, China and Hong Kong, Southeast Asia and Oceania & Singapore) & Regional Insights.

The data represents the countries and territories with net inflows or net outflows of 100 or more HNWIs (namely, the difference between the number of high-net-worth individuals who relocated to and who emigrated away from a particular country during a given year, with all figures rounded to the nearest 100). Notably, nine of the top 10 countries for net inflows of HNWIs in 2023 host formal investment migration programs and actively encourage foreign direct investment in return for residence rights:

Demand grows for Asian investment products that exclude China (FT) (Archived Article)

Also see: China stocks: a strong Caisse for disinvestment - Canada’s second-largest pension fund is following others and retreating from China / Distributor Bunzl shifts more sourcing out of China - FTSE 100 distributor of everything from plastic spoons to PPE looks to ‘de-risk’ its supply chain

Christopher Lees, senior fund manager at J O Hambro Capital Management, said he had heard about potential client demand for “emerging markets ex-China and Asian allies products” as a way to tap into the region’s growth while concentrating exposure in countries with strong ties to the US.

“At the same time, clients are seeing that they can get a lot of exposure to China through other markets like Australia, Japan and South Korea.”

However the main driver of the trend towards ex-China investment was “economic, not geopolitical”, he added, because many emerging markets investors viewed China’s weighting in investment benchmarks from the likes of MSCI and FTSE as too large, tilting the balance away from markets such as Vietnam, Thailand and Indonesia.

“This would be a clear echo of what we had with Japan 30 years ago,” said Lees. Back then, when both the size and volatility of the post-bubble Japanese market skewed Asian portfolios too much, demand rose for Asia ex-Japan products that have remained the fundamental approach to investing in the region.

How Hong Kong’s multinationals and global funds are preparing for the worst (FT) (Archived Article)

“There is a huge terror among US and European investors now that if something happens with China, you get wiped out,” says a senior US asset manager. “As the main centre of allocation of foreign capital into China, Hong Kong is acutely sensitive to that terror.”

At the same time, Hong Kong is a sensible place for multinationals and global funds to begin forming a plan. They should start with an assumption of the abrupt end of life as we know it, recommends one fund manager, and work backwards.

One of the first big signs of a radical shift in thinking, say bankers and other advisers, has been what they report as a rising number of US and European multinationals exploring the idea of entirely carving out their China businesses and listing them separately.

But the fundamental idea of ringfencing the China business would be to secure two forms of protection. The main company would no longer face interrogation on its China exposure; the China business might, in the event of some crackdown on foreign firms, be allowed to survive if its local listing meant Beijing now deemed it a domestic player.

Investors sour on Beijing’s bid to boost state-owned enterprises (FT) (Archived Article)

The 1,432 state-owned enterprises listed in China have long been seen as a tool of government policy and frequently underperform their peers in the west. Listed banks, all of them state-owned, have seen their price-to-book ratios fall below 0.6 from 1.2 over the past five years, compared with PB ratios of more than one for US banks in that period.

Elsewhere, the Wind State-owned Key Enterprises Concept Index, which tracks 55 major SOEs, has lost 9.2 per cent since hitting a peak early last month. The Hang Seng China Central SOEs Index of state-owned companies listed in Hong Kong has lost 9 per cent since hitting a 15-month high in May. The indices remain up in the year to date.

China’s economy is way more screwed than anyone thought (Insider)

Note: Comprehensive and well sourced with links to many other articles or research.

The mechanisms that drove the "Chinese miracle," a triple-decade transformation that made the country an international force, have broken down. The bubble in China's property market finally popped. And because of real estate's central role in the economy, the painful process of absorbing those losses will continue to suck money away from Chinese households, banks, and China's massive web of local governments.

Chinese President Xi Jinping has instead been preparing his people for an era of lower growth, making it clear that's what the economy can achieve in its current state, and it's also the structure he likes.

"The root causes of the disappointing recovery look increasingly structural — a deleveraging mindset and a more permanent loss of animal spirits," Societe Generale's Yao warned in her recent note.

For years, China's local governments funded themselves largely by selling land to property companies. In the US, we fund local governments through property taxes. China doesn't have that, and smaller, poorer provinces are already begging for help because the way they used to raise funds is no longer available.

Some starved local governments are raising college tuition fees as high as 54% at a time when youth unemployment is over 20% and a record number of students are trying to get a higher education.

Is China investable? We think so. (JPMorgan Wealth Management)

Note: From July 31, 2021 - mentioned in the previous article. This is still relevant to consider:

Onshore equities have a higher degree of Chinese domestic ownership, so regulators will probably have a lighter touch so as not to hurt Chinese savers. Further, there is less exposure in the onshore market to the industries in the regulatory crosshairs. 50% of the offshore MSCI China is related to internet, healthcare, education and real estate, but only ~15% of the onshore CSI 300.

State-owned banks, semiconductor manufacturers, clean energy and electric vehicle suppliers, and companies involved with automation should be more insulated from regulatory ire given their strategic importance.

Finally, after a dramatic selloff, the valuations of large profitable tech companies are at trough levels and they are well into the regulatory review process. A lot of bad news seems to be priced in. The odds could be in investor’s favor from here as it relates to the big, profitable tech names.

FTSE Russell Convenes ASEAN (Youtube Playlist)

Ecommerce in Southeast Asia 2023 (Momentum Works)

Note: The 60-page Momentum Works Ecommerce in Southeast Asia 2023 report is $27.95. A 32 minute podcast about the report can be found here.

There are interesting topline dynamics across platforms and geographies:

Shopee registered US$ 47.9 billion GMV, almost half of the region’s GMV;

Lazada remained the 2nd largest player in all countries except Indonesia. Its GMV of US$ 20.1 billion remained at the level of 2021;

TikTok Shop has become a meaningful player, clocking US$ 2.5 billion GMV in Indonesia;

Indonesia contributed 52% of the region’s total GMV; while

Singapore and Malaysia ranked top in GMV per capita;

We see 4 key trends in ecommerce: 1) Geopolitics and shifts of supply chain, 2) Increased investment in logistics and payment infrastructure, 3) Disruption of TikTok, and 4) Brand’s evolving involvement in ecommerce.

We forecast the total GMV to reach US$ 175 billion in 2028 under the normal scenario, with the potential of upside to US$ 232 billion under the best case scenario.

Indian assets are poised for growth in investors' portfolios (Amundi)

Note: See our India ADRs list.

Leaner cost structures, corporate tax reforms, and policy initiatives should support a strong investment cycle in the medium term.

In equities, investor preferences are turning to value stocks, cyclical industries, and mid- and small-capitalisation companies, which have been faring well in the post-Covid recovery. As inflation cools, consumption should also start to pick up.

India seems poised for a prolonged period of upward economic growth and improved earnings, primarily fuelled by a revival in manufacturing and investments.

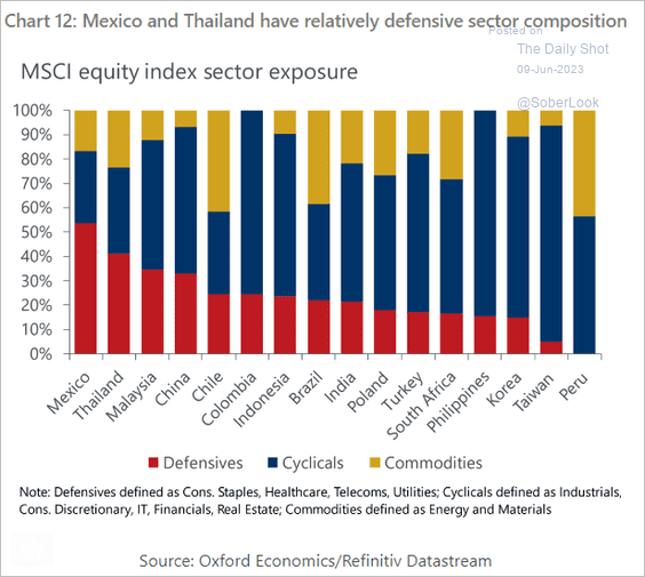

Mexico’s Bull Run (The Emerging Markets Investor)

Note: See our Mexico ADRs list.

The ten largest stocks in the MSCI Mexico index are listed below. With the possible exceptions of Banorte and Cemex, these are profitable world class companies with dominant market positions, all trading at near all-time high stock prices.

Earnings Calendar

Note: Investing.com has a full calendar for most global stock exchanges BUT you may need an Investing.com account, then hit “Filter,” and select the countries you wish to see company earnings from. Otherwise, purple (below) are upcoming earnings for US listed international stocks (Finviz.com):

Economic Calendar

Click here for the full weekly calendar from Investing.com containing frontier and emerging market economic events or releases (my filter excludes USA, Canada, EU, Australia & NZ).

Election Calendar

Frontier and emerging market highlights (from IFES’s Election Guide calendar):

Greece Greek Parliament Jun 25, 2023 (t) Confirmed May 21, 2023

Uzbekistan Uzbekistani Presidency Jul 9, 2023 (t) Confirmed Dec 31, 2021

Cambodia Cambodian National Assembly Jul 23, 2023 (d) Confirmed Jul 29, 2018

Argentina Argentinian Presidency Aug 13, 2023 (d) Confirmed Oct 22, 2023

Zimbabwe Zimbabwean National Assembly Aug 23, 2023 (d) Confirmed Jul 30, 2018

Zimbabwe Zimbabwean Presidency Aug 23, 2023 (d) Confirmed Jul 30, 2018

Singapore Singaporean Presidency Sep 13, 2023 Date not confirmed Sep 23, 2017

Slovakia Slovakian National Council Sep 30, 2023 (t) Confirmed Feb 29, 2020

Pakistan Pakistani National Assembly Oct 1, 2023 (t) Date not confirmed Jul 25, 2018

Argentina Argentinian Chamber of Deputies Oct 22, 2023 (d) Confirmed Oct 24, 2021

Argentina Argentinian Senate Oct 22, 2023 (d) Confirmed Nov 14, 2021

Argentina Argentinian Presidency Oct 22, 2023 (d) Confirmed Aug 13, 2023

Ukraine Ukrainian Supreme Council Oct 29, 2023 (d) Confirmed Jul 21, 2019

Poland Polish Sejm Oct 31, 2023 (t) Date not confirmed Oct 13, 2019

Poland Polish Senate Oct 31, 2023 (t) Date not confirmed Oct 13, 2019

Emerging Market IPO Calendar/Pipeline

Frontier and emerging market highlights from IPOScoop.com and Investing.com (NOTE: For the latter, you need to go to Filter and “Select All” countries to see IPOs on non-USA exchanges):

Note: Two are not emerging market IPOs but interesting companies targeting Asian Americans and others who like Asian food.

Maison Solutions MSS, 3.8M Shares, $4.00-4.00, $15.0 mil, 6/19/2023 Week of

Maison Solutions is a specialty Asian grocery retailer. (Incorporated in Delaware)

We are a fast-growing specialty grocery retailer offering traditional Asian food and merchandise to modern U.S. consumers, in particular to members of Asian-American communities. We are committed to providing Asian fresh produce, meat, seafood, and other daily necessities in a manner that caters to traditional Asian-American family values and cultural norms, while also accounting for the new and faster-paced lifestyle of younger generations and the diverse makeup of the communities in which we operate. To achieve this, we are developing a center-satellite stores network.

Our merchandise includes fresh and unique produce, meats, seafood and other groceries which are staples of traditional Asian cuisine and which are not commonly found in mainstream supermarkets, including a variety of Asian vegetables and fruits such as Chinese broccoli, bitter melon, winter gourd, Shanghai baby bok choy, longan and lychee; a variety of live seafood such as shrimp, clams, lobster, geoduck, and Alaska king crab, and Chinese specialty products like soy sauce, sesame oil, oyster sauce, bean sprouts, Sriracha, tofu, noodles and dried fish. With an in-house logistics team and strong relationships with local and regional farms, we are capable of offering high-quality specialty perishables at competitive prices.

Our multi-pronged approach allows us to provide customers with multiple shopping channels, including integrated online and offline operations, according to Maison Solutions Inc.’s website.

“Customers can place orders on our mobile app “FreshDeal24,” or through our WeChat Applet “Good Luck to Home” for either home delivery or in-store pickup,” the company’s website says.

(Note: Maison Solutions Inc. filed an S-1/A dated June 2, 2023, in which it increased the size of its IPO – to 3.75 million shares – up from 3.0 million shares – and kept the assumed IPO price at $4.00 – to raise $15 million. Under the new terms, Maison Solutions will raise 25 percent more than the $12 million in estimated IPO proceeds under its original terms. Background: Maison Solutions filed its S-1 on May 22, 2023, after submitting confidential IPO documents to the SEC on Dec. 23, 2022.)

GEN Restaurant Group, Inc. GENK, 3.0M Shares, $10.00-12.00, $33.0 mil, 6/22/2023 Thursday

We are a fast-growing Korean barbecue restaurant chain. (Incorporated in Delaware)

GEN Korean BBQ is one of the largest Asian casual dining restaurant concepts by total revenue in the United States. Founded by two Korean immigrants, we have grown over the last eleven (11) years to 32 company-owned restaurants as of May 26, 2023, by delivering an engaging and interactive dining experience where our guests serve as their own chefs. We offer an extensive menu of traditional Korean and Korean-American food, including high-quality meats, poultry, seafood and mixed vegetables, all at a superior value. Our restaurants have modern décor, lively Korean pop music playing in the background and embedded grills in the center of each table. Our food is served family style and requires guests to share and coordinate their cooking responsibilities, which fosters more meaningful interaction than traditional casual dining. We believe our unique culinary experience appeals to a vast segment of the population, particularly Millennials and Gen Z.

Our co-founders, Jae Chang and David Kim, both highly experienced and successful restaurateurs, joined forces to create our new Korean barbeque concept, opening our first restaurant in 2011 in Tustin, California. Since then, we have successfully opened profitable restaurants in multiple new markets. As of May 26, 2023, we operated 32 locations across California, Arizona, Nevada, Hawaii, Texas and New York. Our revenues in the year ended December 31, 2022 surpassed the revenue levels in 2021. In 2022, we achieved a Net Income Margin of 6.3%, a Restaurant-Level Adjusted EBITDA Margin of 20.5% and an Adjusted EBITDA Margin of 13.1%. In the three months ended March 31, 2023, we achieved a Net Income Margin of 9.4%, a Restaurant-Level Adjusted EBITDA Margin of 19.2% and an Adjusted EBITDA Margin of 11.9%.

**Note: Revenue and net income figures are for the 12 months that ended March 31, 2023.

(Note: GEN Restaurant Group disclosed its IPO terms on June 14, 2023, in an S-1/A filing: 3.0 million shares at $10.00 to $12.00 to raise $33.0 million. GEN Restaurant Group filed its S-1 on May 26, 2023. The company submitted confidential IPO documents to the SEC in November 2021.)

AGIIPLUS INC. AGII, 4.5M Shares, $4.50-6.00, $23.6 mil, 6/23/2023 Friday

Note: AgiiPlus Inc., or AgiiPlus, is not an operating company but a Cayman Islands holding company with operations conducted by its subsidiaries, including subsidiaries in China. Investors in our securities are not purchasing equity interests in AgiiPlus’ operating entities in China but instead are purchasing equity interests in a Cayman Islands holding company. (Incorporated in the Cayman Islands)

AgiiPlus’ vision is to build the future of work and to connect businesses with technology, data, services, workspaces and more.

Through its subsidiaries, AgiiPlus is, according to the Frost & Sullivan Report, one of the fastest-growing work solutions providers with a one-stop solution capability in China and Singapore. By leveraging its proprietary technologies, AgiiPlus, through its subsidiaries, offers transformative integrated working solutions to its customers, including brokerage and enterprise services, customizable workspace renovations with smart building solutions, and high-quality flexible workspaces with plug-in software and on-demand services.

AgiiPlus has established an innovative business model called “S²aaS — Space & Software As A Solution,” which combines “Software As A Service”, or SaaS, and “Space As A Service.” This business model relies on proprietary technology, SaaS-based systems, and high-quality physical workspaces to provide customers with integrated work solutions for optimal work efficiency.

AgiiPlus, through its subsidiaries, has created an integrated platform connecting onsite workspaces and digital services through technology. Through its subsidiaries, AgiiPlus offers office leasing and enterprise services under the brand “Tangtang,” and, through its subsidiaries, AgiiPlus maintains the Distrii app, the proprietary official app for workspace members, offering AgiiPlus’ workspace members a seamless experience beyond physical spaces with easy access to enterprise services offered by AgiiPlus’ subsidiaries. As of Dec. 31, 2021, AgiiPlus’ subsidiaries had 35,771 enterprise customers and 322,252 digitally registered members.

Founded in 2016, AgiiPlus has established a network of workspaces in China and Singapore through its subsidiaries. Through Shanghai Distrii Technology Development Co., Ltd., a PRC subsidiary, AgiiPlus offers enterprise customers flexible and cost-effective space solutions in centrally located business districts in tier-one and new tier-one cities in China and Singapore. As of Dec. 31, 2021, through its subsidiaries, AgiiPlus maintained a network of 61 Distrii workspaces that covered seven different cities, namely Shanghai, Beijing, Nanjing, Suzhou, Jinan and Xiong’an in China, and Singapore, with a total managed area of about 256,291 square meters (approximately 2.8 million square feet) and approximately 41,455 workstations in total.

In addition, AgiiPlus’ asset-light model offers design, build, management and operating services to landlords who bear the costs in building and launching new spaces. This asset-light model allows AgiiPlus’ subsidiaries to economically expand and scale up while enabling landlords to turn their spaces into revenue-generating properties backed by professional services offered by AgiiPlus’ subsidiaries and AgiiPlus’ brand image. As of Dec. 31, 2021, through its subsidiaries, AgiiPlus had eight workspaces under the asset-light model, with a total managed area of about 22,947 square meters (approximately 247,000 square feet) and approximately 4,161 workstations available for members.

**Note: Revenue and net loss figures are in U.S. dollars (converted from China’s renminbi) for the year ended Dec. 31, 2022.

(Note: AgiiPlus Inc. cut the size of its IPO by 40 percent in an F-1/A filing dated March 22, 2023: The number of Class A ordinary shares was cut to 4.5 million shares – down from 8.7 million shares previously – and the price range was increased to $4.50 to $6.00 – up from $4.00 to $5.00 – to raise $23.63 million. The new terms cut the IPO’s estimated proceeds by 40 percent from the initial estimate of $39.15 million under the original terms – 8.7 million shares at $4.00 to $5.00 – that were disclosed in an F-1/A filing dated Nov. 7, 2022. The F-1 was filed on Sept. 16, 2022; confidential filing was submitted on June 17, 2022.)

Cheetah Net Supply Chain Service Inc. CTNT, 2.0M Shares, $4.00-6.00, $10.0 mil, 6/26/2023 Week of

Cheetah Net Supply Chain Service Inc. imports luxury cars, including Mercedes and BMW, to China. (Incorporated in the Cayman Islands)

We are a supplier of parallel-import vehicles sourced in the U.S. to be sold in the PRC market. In the PRC, parallel-import vehicles refer to those purchased by dealers directly from overseas markets and imported for sale through channels other than brand manufacturers’ official distribution systems.

We purchase automobiles, primarily luxury brands such as Mercedes, BMW, Porsche, Lexus, and Bentley, from the U.S. market and resell them to our customers, including both U.S. and PRC parallel-import car dealers. We derive profits primarily from the price difference between our buying and selling prices for parallel-import vehicles.

The primary driver for our industry is the continued growth of wealthy groups in China. The core of our business is the ability to identify the type of parallel-import vehicles that are in high demand and to procure them in a timely manner. Since our inception in 2016, our management has focused on building our procurement team. We procure our automobiles from U.S. automobile dealers via a network of independent contractors acting as purchasing agents on our behalf. As of Dec. 31, 2022, and 2021, we actively worked with 342 and 300 purchasing agents, respectively.

As of Dec. 2022, and 2021, we had an active customer base of 17 and eight dealers, respectively. Specifically, we had eight U.S. customers and nine PRC customers in 2022 and had four customers in each of the U.S. and the PRC in 2021. During the years ended Dec. 31, 2022, and 2021, we sold 434 and 167 parallel-import vehicles to Chinese parallel-import car dealers, respectively. During the same period, we sold 29 and 220 parallel-import vehicles to our U.S. domestic customers, respectively.

We sold 463 and 387 vehicles during the years ended Dec. 31, 2022, and 2021, respectively.

**Note: Net income and revenue are for the 12 months that ended Dec. 31, 2022.

(Note: Cheetah Net Supply Chain Service Inc. filed an S-1/A on April 28, 2023, in which it disclosed its IPO terms: 2.0 million shares at $4.00 to $6.00 to raise $10.0 million. Cheetah Net Supply Chain Service Inc. filed its S-1 on April 7, 2023.)

Emerging Market ETF Launches

Climate change and ESG are clearly the latest flavours of the month for most new ETFs. Nevertheless, here are some new frontier and emerging market focused ETFs:

03/16/2023 - JPMorgan Active China ETF JCHI - Active, equity, China

03/03/2023 - First Trust Bloomberg Emerging Market Democracies ETF EMDM - Principles-based

1/31/2023 - Strive Emerging Markets Ex-China ETF STX - Passive, equity, emerging markets

1/20/2023 - Putnam PanAgora ESG Emerging Markets Equity ETF PPEM - Active, equity, ESG, emerging markets

1/12/2023 - KraneShares China Internet and Covered Call Strategy ETF KLIP - Active, equity, China, options overlay, thematic

1/11/2023 - Matthews Emerging Markets ex China Active ETF MEMX - Active, equity, emerging markets

12/13/2022 - GraniteShares 1.75x Long BABA Daily ETF BABX - Active, equity, leveraged, single stock

12/13/2022 - Virtus Stone Harbor Emerging Markets High Yield Bond ETF VEMY - Active, fixed income, junk bond, emerging markets

9/22/2022 - WisdomTree Emerging Markets ex-China Fund XC - Passive, equity, emerging markets

9/15/2022 - KraneShares S&P Pan Asia Dividend Aristocrats Index ETF KDIV - Passive, equity, Asia, dividend strategy

9/15/2022 - OneAscent Emerging Markets ETF OAEM - Active, Equity, emerging markets, ESG

9/9/2022 - Emerge EMPWR Sustainable Select Growth Equity ETF EMGC - Active, equity, emerging markets

9/9/2022 - Emerge EMPWR Unified Sustainable Equity ETF EMPW - Active, equity, emerging markets

9/8/2022 - Emerge EMPWR Sustainable Emerging Markets Equity ETF EMCH - Active, equity, emerging markets, ESG

7/14/2022 - Matthews China Active ETF MCH - Active, equity, China

7/14/2022 - Matthews Emerging Markets Equity Active ETF MEM - Active, equity, emerging markets

7/14/2022 - Matthews Asia Innovators Active ETF MINV - Active, equity, Asia

6/30/2022 - BondBloxx JP Morgan USD Emerging Markets 1-10 Year Bond ETF XEMD - Passive, fixed income, emerging markets

5/2/2022 - AXS Short CSI China Internet ETF SWEB - Active, inverse, thematic

4/27/2022 - Dimensional Emerging Markets High Profitability ETF DEHP - Active, equity, emerging markets

4/27/2022 - Dimensional Emerging Markets Core Equity 2 ETF DFEM - Active, equity, emerging markets

4/27/2022 - Dimensional Emerging Markets Value ETF DFEV - Active, equity, emerging markets

4/27/2022 - iShares Emergent Food and AgTech Multisector ETF IVEG - Passive, equity, thematic [Mostly developed markets]

4/21/2022 - FlexShares ESG & Climate Emerging Markets Core Index Fund FEEM - Passive, equity, ESG

4/6/2022 - India Internet & Ecommerce ETF INQQ - Passive, equity, thematic

2/17/2022 - VanEck Digital India ETF DGIN - Passive, India market, thematic

2/17/2022 - Goldman Sachs Access Emerging Markets USD Bond ETF GEMD - Passive, fixed income, emerging markets

1/27/2022 - iShares MSCI China Multisector Tech ETF TCHI - Passive, China, technology

1/11/2022 - Simplify Emerging Markets PLUS Downside Convexity ETF EMGD - Active, equity, options strategy

1/11/2022 - SPDR Bloomberg SASB Emerging Markets ESG Select ETF REMG - Passive, equity, ESG

Emerging Market ETF Closures/Liquidations

Frontier and emerging market highlights:

06/23/2023 - Invesco PureBeta FTSE Emerging Markets ETF - PBEE

3/30/2023 - Invesco BLDRS Emerging Markets 50 ADR Index Fund - ADRE

3/30/2023 - Invesco BulletShares 2023 USD Emerging Markets Debt ETF - BSCE

3/30/2023 - Invesco BulletShares 2024 USD Emerging Markets Debt ETF - BSDE

3/30/2023 - Invesco RAFI Strategic Emerging Markets ETF - ISEM

2/17/2023 - Direxion Daily CSI 300 China A Share Bear 1X Shares - CHAD

1/13/2023 - First Trust Chindia ETF - FNI

12/28/2022 - Franklin FTSE Russia ETF - FLRU

12/22/2022 - VictoryShares Emerging Market High Div Volatility Wtd ETF CEY

8/22/2022 - iShares MSCI Argentina and Global Exposure ETF AGT

8/22/2022 - iShares MSCI Colombia ETFI COL

6/10/2022 - Infusive Compounding Global Equities ETF JOYY

5/3/2022 - ProShares Short Term USD Emerging Markets Bond ETF EMSH

4/7/2022 - DeltaShares S&P EM 100 & Managed Risk ETF DMRE

3/11/2022 - Direxion Daily Russia Bull 2X Shares RUSL

1/27/2022 - Legg Mason Global Infrastructure ETF INFR

1/14/2022 - Direxion Daily Latin America Bull 2X Shares LBJ

Check out our emerging market ETF lists, ADR lists (updated) and closed-end fund (updated) lists (also see our site map + list update status as some ETF lists are still being updated as of Summer 2022).

I have changed the front page of www.emergingmarketskeptic.com to mainly consist of links to other emerging market newspapers, investment firms, newsletters, blogs, podcasts and other helpful emerging market investing resources. The top menu includes links to other resources as well as a link to a general EM investing tips / advice feed e.g. links to specific and useful articles for EM investors.

Disclaimer. The information and views contained on this website and newsletter is provided for informational purposes only and does not constitute investment advice and/or a recommendation. Your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content. Seek a duly licensed professional for any investment advice. I may have positions in the investments covered. This is not a recommendation to buy or sell any investment mentioned.

Emerging Market Links + The Week Ahead (June 19, 2023) was also published on our website under the Newsletter category.