Emerging Market Links + The Week Ahead (June 26, 2023)

European business sentiment in China deteriorates, nearshoring favors small caps + IT stocks, El Niño’s back, Singapore stock picks, how to manage EM volatility & the week ahead for emerging markets.

The latest 2023 Business Climate Survey from the European Union Chamber of Commerce in China shows a significant deterioration in business sentiment. Nevertheless, a Singapore based portfolio manager has likened the environment in China to the old joke about three blind men looking at an elephant. Depending on which part of the elephant you’re touching, you get a very different view of what that elephant looks like…

Meanwhile, one fund manager expects reshoring and nearshoring to favor small-cap stocks (along with the IT sector). They also predict that China and other Asian emerging markets will be affected sooner than other suppliers as nobody wants a repeat of the COVID snarled supply chains.

However, another fund manager has pointed out China’s economic structure has made it the world’s factory and that won’t unravel quickly. Other manufacturing bases such as Vietnam or Mexico may experience an increase in manufacturing demand, but they will consequently need to import more components from China in order to meet that demand.

Finally, a fund manager in a recent podcast made the interesting observation that if you create a basket (portfolio) of emerging or frontier markets, you generally end up with something that (in aggregate) is much less volatile than if you were to look at emerging markets at the index level. The fund manager explained:

There are generally minimal trade flows between smaller emerging and frontier countries, so problems in the real estate market in Vietnam will tend to have no impact on the level of oil production in Argentina. The recent election in Thailand had no impact on the subsequent Greek election. Constitutional change in Chile won’t impact interest rate movements in Saudi Arabia.

Definitely thoughts worth remembering whenever you read scary media headlines about something negative happening in an emerging market country somewhere.

Emerging Market Stock Pick Tear Sheets

$ = behind a paywall

Southern Sun (JSE: SSU): Almost Normalcy for Southern Africa's Leading Hospitality Stock

Tsogo Sun Ltd (JSE: TSG / FRA: G5E): Africa's Biggest Casino Operator is Getting Bigger

moneycontrol India Stock of the Day (May 2023) Partly $

Includes: Indraprastha Gas (IGL), Star Health & Allied Insurance, Aditya Birla Capital, Amber Enterprises, Apcotex Industries, Coromandel International, CEAT Ltd, Karur Vysya Bank, Godrej Consumer Products, Devyani International, Sona BLW Precision Forgings, Home First Finance, KEC International, Crompton Greaves, CMS Info Systems, PI Industries, CSB Bank, IndusInd Bank, Laurus Labs & Tata Consumer Products

Emerging Market Stock Picks / Stock Research

$ = behind a paywall

Alibaba’s Chairman & CEO, Daniel Zang Faces a Downgrade (Smartkarma) $

Daniel Zhang's transition to a less prominent role within Alibaba's Cloud business, after previously serving as CEO and Chairman of Alibaba Group (NYSE: BABA), could be seen as a demotion.

We suspect that there could be some government influence on these proposed leadership changes.

Nonetheless, the situation is not encouraging, especially as the company enters a turbulent phase with multiple units poised to pursue IPOs in the near future.

Alibaba’s Cainiao IPO: The First Look (Smartkarma) $

Alibaba Group’s (NYSE: BABA) aims to complete the IPO of Cainiao Smart Logistics (1437124D HK) in the next 12 to 18 months. Alibaba holds a 67% stake in Cainiao.

Cainiao's revenue growth, while on a declining trend, remains in double digits. Encouragingly. narrowing losses set a path to profitability.

On 30 March, Bloomberg reported that Cainiao is currently valued at more than US$20 billion. Our valuation analysis suggests that such a valuation is justifiable.

J&T Express: Highlights Of Draft IPO Prospectus (Momentum Works)

J&T Express, a leading ecommerce logistics company in Southeast Asia & China, filed its draft IPO prospectus to Hong Kong Stock Exchange on 16 June 2023.

We have put together some highlights of the prospectus which we think are quite relevant to stakeholders of Southeast Asia’s ecommerce ecosystem.

LG Chem: Considering a Block Deal Sale of About 2 Trillion Won of LG Energy Solution: A Big Overhang (Smartkarma) $

Note: See LG Chem (KRX: 051910): Owns Battery Stock LG Energy Solution (And Might Be the Better Stock to Own) & LG Energy Solution (KRX: 373220): World's Biggest Non-Chinese EV Battery Stock.

"It was reported in the local media that LG Chem (KRX: 051910) is close to selling about 2 trillion won worth of LG Energy Solution (KRX: 373220), which is likely to pose overhang on LG Energy Solution's share price." - Douglas Kim

After the market close on 16 June, it was reported in the local media that LG Chem is close to selling about 2 trillion won worth of LG Energy Solution.

This block deal sale is likely to pose overhang on more stake sales of LG Energy Solution (about 10% stake) in the next 3-5 years.

Our NAV valuation analysis of LG Chem suggests an implied price of 1,057,770 won per share, which is 41% higher than current share price.

3 Singapore Blue-Chip Stocks Are Growing Their Businesses: Can Their Share Prices Outperform? (The Smart Investor)

These three blue-chip stocks are undertaking business development initiatives to grow their top and bottom lines.

Jardine Cycle & Carriage (SGX: C07 / FRA: CYC), or JC&C, is an investment holding company under the Jardine Matheson (SGX: J36 / FRA: H4W / OTCMKTS: JARLF) group.

Keppel Corporation Limited (SGX: BN4 / FRA: KEP1 / OTCMKTS: KPELY / KPELF) is a global asset manager with strong expertise in the infrastructure, real estate, and connectivity industries. The group has been busy with a flurry of business development activities.

SATS Ltd (SGX: S58 / FRA: W1J / OTCMKTS: SPASF) is a leader in gateway services for airlines and also provides them with food catering and ground handling services. On 31 May, the group announced that it had executed a concession agreement to build a multi-modal cargo hub (MMCH) at Noida International Airport in Uttar Pradesh, India.

Here Are 3 Singapore Healthcare Stocks That Can Deliver Both Growth and Dividends (The Smart Investor)

Healthcare is a key focus of the Singapore government, which is why these stocks are well-positioned to deliver the best of both worlds.

IHH Healthcare (SGX: Q0F / KLSE: IHH / OTCMKTS: IHHHF) is an integrated healthcare provider with a portfolio of trusted hospital brands such as Mount Elizabeth, Gleneagles, Parkway, Fortis, and Acibadem.

The group plans to grow organically by adding more than 2,000 new beds in Malaysia, India, and Turkey over the next three years. It is also looking for acquisition opportunities across Asia and Europe and expects revenue growth to continue.

Econ Healthcare (SGX: EHG) is a private nursing home operator in Singapore and Malaysia and a pioneer in providing eldercare services. The group’s network comprises 11 Medicare centres and nursing homes in Singapore and Malaysia along with two nursing homes in China.

Thomson Medical Group (SGX: A50 / FRA: 3H5), or TMG, is one of the largest private providers of healthcare services for women and children in Singapore.

TMG seeks to grow its Pan-Asian footprint and has been actively seeking out investment opportunities that may involve acquisitions or collaborations with healthcare businesses in the region.

4 Industrial REITs Yielding 5% or More with Good Potential for Upping Their DPU (The Smart Investor)

When scouting for good industrial REITs to own, you want sustainable distribution yields with a high probability of rising DPU too.

Mapletree Logistics Trust (SGX: M44U / OTCMKTS: MAPGF), or MLT, is a logistics REIT with a portfolio of 185 properties across eight countries.

It has announced a proposed acquisition of eight logistics assets in Japan, Australia, and South Korea for S$904.4 million along with a potential acquisition of two more logistics assets in China for S$209.6 million.

Mapletree Industrial Trust (SGX: ME8U / OTCMKTS: MAPIF), or MIT, has a portfolio of 85 properties in Singapore and 56 in the US with an AUM of S$8.8 billion as of 31 March 2023.

The manager also announced the REIT’s first acquisition in two years, that of a data centre in Osaka, Japan, for S$500.1 million.

AIMS APAC REIT (SGX: O5RU / OTCMKTS: ACIRF), or AAREIT, has a portfolio comprising 29 properties, of which 26 are located in Singapore and three in Australia.

The REIT just announced an equity fundraising exercise to raise approximately S$100 million which will be used to fund AEIs, redevelopments, or acquisitions as well as pay down debt.

Frasers Logistics & Commercial Trust (SGX: BUOU / OTCMKTS: FRLOF), or FLCT, owns 107 industrial and commercial properties across five countries with an AUM of around S$6.8 billion as of 31 March 2023.

Southeast Asia Plantations: El Niño’s Back, with a Vengeance? (Smartkarma) $

FYI… Plus California had significant rain-cool weather last winter-spring impacting almonds and store prices for coffee in Malaysia have noticeably risen a bit as there are problems with one crop variety. See: Time for Coffee ETF On El Nino-Driven Shortage?

The NOAA has confirmed that the world is at the start of an El Niño, which means less rainfall in Southeast Asia and pressure on oil palm yields.

Early signs point to a severe event, which would cause a significant edible oil deficit in 2024. Ongoing drought in the U.S. is a budding wild card, affecting soybeans.

The report projects a 40% YoY higher average crude palm oil price in 2024. Given depressed consensus expectations and undemanding valuation, the risk-reward is bullish on a 6-12 month horizon.

Suitor pulls out of US$1.2bln Miami land sale by Genting (GGRAsia)

The filing added: “Genting Malaysia (KLSE: GENM) has seen the value of its investment in Miami increase approximately 400 percent in just over a decade and firmly believes in the sustained strength and growth of the Miami market.”

Genting Malaysia has for some time been identified as a likely suitor for a downstate casino licence in New York.

MTN Group: Connecting Africa (Business Breakdowns Podcast) 1 Hour

Note: MTN (JSE: MTN) has the largest fixed and mobile network in Africa.

This is Zack Fuss, an investor at Irenic Capital, and today we’re breaking down MTN Group. MTN is the largest mobile network operator in Africa and one of the 10 largest in the world. It has over 270 million subscribers, operates in 20 different markets, and is also one of the largest FinTech’s in the continent.

To break down MTN, I’m joined by Benjamin Isaac, founder and Chief Investment Officer at Brizo Capital. We unpack their mobile money business in some detail, contrast the development of Telcos in Africa with what we’ve experienced in the US, and explore the competitive dynamics of operating in Africa.

Quick ideas #2 (Turtles all the way down!)

The first one is Genomma Lab (BMV: LABB / FRA: GEKA / OTCMKTS: GNMLF), a Mexican branded OTC pharma and personal care products company. The stock trades at a cheap multiple of about 10x earnings. But if you adjust for currency losses, the stock is cheaper. Although it is questionable how ‘one of’ those currency losses are given that some of their operations are in countries suffering high inflation like Argentina.

This seems cheapish given that historically this stock traded closer to 15x earnings.

There was an incident of channel stuffing almost a decade ago that is worth mentioning. This VIC write-up goes into more detail. But that was under previous management and I don’t think is really an issue here.

MORAM - Arcos Dorados $ARCO investment thesis + Options strategies + Inter Cars (Investment theses in Small Caps & Macroeconomic analysis)

The Arcos Dorados (NYSE: ARCO) investment thesis - $2Bn US listed company which is the main franchisee of McDonald’s, it has a presence in 20 Latin American countries, and we believe that it is an interesting moment to analyse it in detail.

The royalty fee expected to be paid to McDonald’s is around 6% of total revenues in 2023 and 2024. We think it will probably rise slightly onwards. This is why McDonald’s EBITDA margin is an extraordinary c.50%, and Arcos stays around 10%. The royalty fee from sub-franchised restaurants to Arcos is 5%.

We were initially attracted to Arcos mainly for two reasons:

The opportunity to gain exposure to South America with a defensive approach. This is, having a clear view on what is the dynamics affecting the company (trends on food and labor inflation, customer demand, etc.), and limiting the country risk that would have investing in only one country of Latin America or the Caribbean.

The strength of McDonald’s brand and the disparity in valuations with other public restaurant chains.

Further Suggested Reading

$ = behind a paywall

2023 Business Climate Survey + Press Release (The European Union Chamber of Commerce in China)

The 20th edition of the annual survey shows that there has been a significant deterioration of business sentiment.

64% of respondents reported that doing business in China became more difficult in the past year, the highest on record.

30% of respondents reported year-on-year (y-o-y) revenue decreases, an increase of 20 percentage points, and the highest on record.

11% of respondents have shifted existing investments out of China, and 8% have taken the decision move future investments previously planned for China elsewhere.

One in ten report they have already shifted, or plan to shift, their Asia headquarters (HQ) or business unit HQ out of Mainland China.

There has been a 13-percentage point reduction y-o-y in the number of respondents that view China as a top-three destination for future investments.

75% have reviewed their supply chain strategies over the past two years, with 24% reporting plans to at least partially onshore their supply chains into Mainland China and 12% having already shifted parts of them out of the country.

Decoupling of HQ and China operations has increased primarily to manage risk, with nearly three quarters of respondents having localised IT and data storage infrastructure. Significant localisation of company staff has also taken place over the last half decade, with 16% reporting their China operations no longer employ any foreign nationals.

These developments come at a considerable cost to companies and to China. The need to create divergent systems for China and the rest of the world means that the overall efficiency brought by global economies of scale is lost; and the reduction of foreign nationals is resulting in reduced transfer of knowhow and best practices, communication difficulties, deferred investment plans, and even China operations being closed.

The Implications of China's Far-From-Typical Recovery (PGIM Fixed Income)

In an economic context, the geopolitical strain is highlighted by the expanding technology divide between China and much of the developed world where the latter is increasingly hesitant to share advancements and data with China. Although China is a significant market, the divide exposes China’s risk of becoming a data and technology island with its attendant growth implications.

When applying these considerations to investment implications, we’ll summarize the points from our recent podcast [OUTLOOK ON CHINA—DISCUSSING THE RE-OPENING, GROWTH FORECAST, AND MORE 29:36 minutes, from May 3]. Bonds at the sovereign/quasi-sovereign level appear overly rich, and while the corporate sector provides plenty to analyze, we’ve been very defensively positioned across our emerging market and multi-sector portfolios. As we alluded to above, we see further weakening in the Chinese yuan, hence we’re maintaining a slight underweight to the currency as well.

Although excess capacity exists, China’s economic structure has made it the world’s factory, and that won’t unravel quickly. For those pointing to other manufacturing bases, such as Vietnam or Mexico, that may experience an increase in manufacturing demand, they will consequently need to import more components from China in order to meet that demand.

The second point pertains to the prospect that, over time, the Chinese yuan will usurp the U.S. dollar as the world’s reserve currency. But for any currency to do so, capital needs to flow freely. The steps that China will need to take in order to manage its debt load— notably lower interest rates with a resultant drag on the yuan—require capital controls, lest capital flight becomes an increasingly tangible risk.

Won’t Get Fooled Again: Global Firms Secure Their Supply Chains (American Century Investments)

Businesses are reshoring, nearshoring and friendshoring operations to avoid repeating the supply chain snarls set off during the pandemic.

Information technology companies, especially those in IT services, logistics software and semiconductor supply chains, appear to be forerunners of reshoring and nearshoring.

As companies reshore jobs and operations, we expect China and other Asian emerging markets to be affected sooner than other suppliers.

We believe the shift to reshoring and nearshoring should favor small-cap stocks. Reasons for this thinking include the following:

Reshoring implies increased capital expenditure as companies build new facilities at or near home. Small-cap revenue growth has historically shown a high correlation with CapEx spending, according to Bank of America research.

New production facilities require vast support networks. For example, spurred by the availability of federal subsidies in the CHIPS Act, Taiwan Semiconductor Manufacturing Co. (TSMC) will invest $40 billion to open two chip plants in North Phoenix, Arizona. TSMC Arizona and its workforce will need new infrastructure, housing, restaurants, retailers, medical facilities and more. We expect the new jobs in TSMC’s supporting industries to skew toward small-cap companies.

Small-caps tend to derive more revenue generation and earnings growth from local operations than large-caps, given their greater domestic focus. We believe this should bode well for them in a reshoring environment.

2023 Equity Midyear Outlook: Potential in Emerging Markets (Allspring) 11:34 Minutes (Includes Transcript)

We’re bottom-up stock pickers, right? So, I spend my day worrying about business models and margins and companies and whatnot. But the reality is the dollar is incredibly important to the trajectory for emerging market equity prices. It does appear that the dollar peaked last year after really about a 10-year bull run versus emerging markets. And it was a very significant drag for emerging market equities. And we think that certainly, if not reversing entirely, the drag the dollar could have on emerging market equities does seem to be dissipating.

Gary Tan, one of our team members and a portfolio manager who sits in Singapore, was just in China and he likened the environment there to that old joke about three blind men looking at an elephant, right? Depending on which part of the elephant you’re touching, you get a very different view of what that elephant looks like.

Outside of that, as I mentioned, Brazil is at an inflection point from a top-down standpoint and that’s creating interesting bottom-up opportunities, particularly on the domestic consumption side, which has been very, very weak for some time and we think will begin to recover through 2023 and 2024.

And then one of the areas we’re looking at are companies that might be beneficiaries of what has been described as nearshoring, or onshoring, or the movement of supply chains, from China to other countries. Mexico, India, and the rest of Southeast Asia, as well, are clear beneficiaries here and we’re able to find interesting opportunities at the company level.

And it’s very interesting because so much of the artificial intelligence supply chain sits in emerging markets, whether it’s the chip makers, memory in Taiwan, and Korea. And then as we look at the eventual development of artificial intelligence over the next few years, there really is a whole other ecosystem of software companies that potentially really can dominate the emerging markets ecosystem, which is very different than what we’re seeing in developed markets.

An active investor’s guide to emerging markets stocks (BlackRock)

Emily Fletcher, an emerging markets portfolio manager within BlackRock Fundamental Equities recently joined The Bid podcast to offer her observations as an investor who is meeting with companies and handpicking stocks across the world’s developing economies. We offer excerpts of that conversation here….

How can investors manage the volatility inherent in EM investing?

That’s a very fair point to pull out and especially in some of these smaller markets. In and of themselves, they can be inherently and deeply risky and volatile. But one of the really interesting things about these smaller markets is that if you create a basket of them, put together a portfolio of them, you generally end up with something that in aggregate is much less volatile than if you were to look at emerging markets at the index level.

These are places in the world where you can still find diversification. There are generally minimal trade flows between smaller emerging and frontier countries, so problems in the real estate market in Vietnam will tend to have no impact on the level of oil production in Argentina. The recent election in Thailand had no impact on the subsequent Greek election. Constitutional change in Chile won’t impact interest rate movements in Saudi Arabia. So, it’s very interesting that you still have huge benefits of diversification from looking at some of these smaller markets.

Note: 17 Minutes long and a bit of a weird format…

Russian ADRs and GDRs – what's next? (Undervalued Shares)

Noteworthy developments have since taken place, few of which will have been covered by the mainstream media.

If you are affected by this issue, today's Weekly Dispatch is a must-read, and it will point you towards experts who can help with individual cases.

In Argentina, Inflation Passes 100% (and the Restaurants Are Packed) (NYT) (Archived Article)

Interesting article about how locals deal with inflation in an emerging market…

Argentina’s financial crisis has a surprising side effect: a flourishing dining scene in Buenos Aires, as residents rush to spend pesos before they lose more value.

The economist Santiago Manoukian said the restaurant boom was a phenomenon that cuts across classes as people seek to spend Argentine pesos before they continue to lose value.

For members of the middle class in particular, expenditures like a vacation or a car have become largely out of reach, so they are indulging in other ways.

But even lower-income gig workers, who saw their earnings shrink by 35 percent since 2017, according to data gathered by Ecolatina, are dining out before their money devalues even more, Mr. Manoukian said.

“It’s a product of the distortions that the Argentine economy suffers from,” he said. “You have extra pesos that are going up in smoke because of inflation, and you have to do something because you know the worst thing you can do is nothing.”

Earnings Calendar

Note: Investing.com has a full calendar for most global stock exchanges BUT you may need an Investing.com account, then hit “Filter,” and select the countries you wish to see company earnings from. Otherwise, purple (below) are upcoming earnings for US listed international stocks (Finviz.com):

Economic Calendar

Click here for the full weekly calendar from Investing.com containing frontier and emerging market economic events or releases (my filter excludes USA, Canada, EU, Australia & NZ).

Election Calendar

Frontier and emerging market highlights (from IFES’s Election Guide calendar):

GreeceGreek ParliamentJun 25, 2023 (t) Confirmed May 21, 2023Uzbekistan Uzbekistani Presidency Jul 9, 2023 (t) Confirmed Dec 31, 2021

Cambodia Cambodian National Assembly Jul 23, 2023 (d) Confirmed Jul 29, 2018

Argentina Argentinian Presidency Aug 13, 2023 (d) Confirmed Oct 22, 2023

Ecuador Ecuadorian Presidency Aug 20, 2023 (t) Confirmed Apr 11, 2021

Ecuador Ecuadorian National Congress Aug 20, 2023 (t) Confirmed Feb 7, 2021

Zimbabwe Zimbabwean National Assembly Aug 23, 2023 (d) Confirmed Jul 30, 2018

Zimbabwe Zimbabwean Presidency Aug 23, 2023 (d) Confirmed Jul 30, 2018

Singapore Singaporean Presidency Sep 13, 2023 Date not confirmed Sep 23, 2017

Slovakia Slovakian National Council Sep 30, 2023 (t) Confirmed Feb 29, 2020

Pakistan Pakistani National Assembly Oct 14, 2023 (t) Date not confirmed Jul 25, 2018

Argentina Argentinian Chamber of Deputies Oct 22, 2023 (d) Confirmed Oct 24, 2021

Argentina Argentinian Senate Oct 22, 2023 (d) Confirmed Nov 14, 2021

Argentina Argentinian Presidency Oct 22, 2023 (d) Confirmed Aug 13, 2023

Ukraine Ukrainian Supreme Council Oct 29, 2023 (d) Confirmed Jul 21, 2019

Poland Polish Sejm Oct 31, 2023 (t) Date not confirmed Oct 13, 2019

Poland Polish Senate Oct 31, 2023 (t) Date not confirmed Oct 13, 2019

Chile Referendum Dec 17, 2023 (t) Confirmed Sep 4, 2022

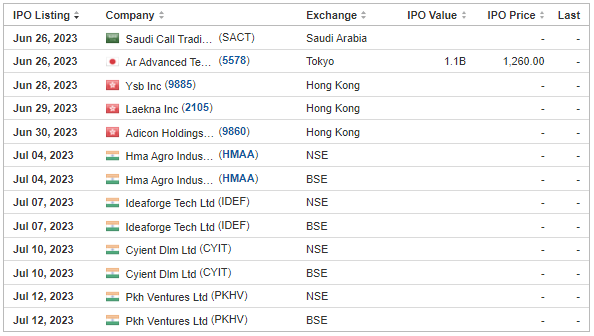

Emerging Market IPO Calendar/Pipeline

Frontier and emerging market highlights from IPOScoop.com and Investing.com (NOTE: For the latter, you need to go to Filter and “Select All” countries to see IPOs on non-USA exchanges):

GEN Restaurant Group, Inc. GENK, 3.0M Shares, $10.00-12.00, $33.0 mil, 6/27/2023 Tuesday

We are a fast-growing Korean barbecue restaurant chain. (Incorporated in Delaware)

GEN Korean BBQ is one of the largest Asian casual dining restaurant concepts by total revenue in the United States. Founded by two Korean immigrants, we have grown over the last eleven (11) years to 32 company-owned restaurants as of May 26, 2023, by delivering an engaging and interactive dining experience where our guests serve as their own chefs. We offer an extensive menu of traditional Korean and Korean-American food, including high-quality meats, poultry, seafood and mixed vegetables, all at a superior value. Our restaurants have modern décor, lively Korean pop music playing in the background and embedded grills in the center of each table. Our food is served family style and requires guests to share and coordinate their cooking responsibilities, which fosters more meaningful interaction than traditional casual dining. We believe our unique culinary experience appeals to a vast segment of the population, particularly Millennials and Gen Z.

Our co-founders, Jae Chang and David Kim, both highly experienced and successful restaurateurs, joined forces to create our new Korean barbeque concept, opening our first restaurant in 2011 in Tustin, California. Since then, we have successfully opened profitable restaurants in multiple new markets. As of May 26, 2023, we operated 32 locations across California, Arizona, Nevada, Hawaii, Texas and New York. Our revenues in the year ended December 31, 2022 surpassed the revenue levels in 2021. In 2022, we achieved a Net Income Margin of 6.3%, a Restaurant-Level Adjusted EBITDA Margin of 20.5% and an Adjusted EBITDA Margin of 13.1%. In the three months ended March 31, 2023, we achieved a Net Income Margin of 9.4%, a Restaurant-Level Adjusted EBITDA Margin of 19.2% and an Adjusted EBITDA Margin of 11.9%.

**Note: Revenue and net income figures are for the 12 months that ended March 31, 2023.

(Note: GEN Restaurant Group disclosed its IPO terms on June 14, 2023, in an S-1/A filing: 3.0 million shares at $10.00 to $12.00 to raise $33.0 million. GEN Restaurant Group filed its S-1 on May 26, 2023. The company submitted confidential IPO documents to the SEC in November 2021.)

Chi Ko Holdings Limited CKHL, 1.7M Shares, $4.00-5.00, $7.8 mil, 6/30/2023 Friday

We are a holding company incorporated in the Cayman Islands with operations conducted by our Hong Kong subsidiary, Chiu & Lee Partners. (Incorporated in the Cayman Islands)

We are a one-stop shop construction service provider and established construction contractor in Hong Kong with over 40 years of experience in the construction industry, principally providing (i) foundation and site formation work, which mainly includes piling work, excavation and lateral support work and pile cap construction, (ii) general building work and associated services, which mainly includes development of superstructures, alteration and addition work; and (iii) other construction work, which mainly includes demolition work. We are able to undertake construction work as either a main contractor or a subcontractor.

We are a company principally engaged in construction work in Hong Kong. We have obtained the relevant registration for our business operations via our key Operating Subsidiary, Chiu & Lee Partners, as a general building contractor from the Buildings Department of Hong Kong since 1999 and as a specialist contractor in the demolition work category, foundation work category and site formation work category from the Buildings Department of Hong Kong since 2006.

**Note: Revenue and net income figures are in U.S. dollars for the 12 months that ended Sept. 30, 2022.

(Note: Chi Ko Holdings Limited set terms for its IPO in an F-1/A filing dated May 30, 2023: 1.74 million shares at $4.00 to $5.00 to raise $7.83 million. Chi Ko Holdings Limited filed its F-1 on March 16, 2023, without disclosing terms for its IPO. The shares in the IPO will be offered by the Cayman Islands holding company and not by the underlying business in Hong Kong.)

Emerging Market ETF Launches

Climate change and ESG are clearly the latest flavours of the month for most new ETFs. Nevertheless, here are some new frontier and emerging market focused ETFs:

03/16/2023 - JPMorgan Active China ETF JCHI - Active, equity, China

03/03/2023 - First Trust Bloomberg Emerging Market Democracies ETF EMDM - Principles-based

1/31/2023 - Strive Emerging Markets Ex-China ETF STX - Passive, equity, emerging markets

1/20/2023 - Putnam PanAgora ESG Emerging Markets Equity ETF PPEM - Active, equity, ESG, emerging markets

1/12/2023 - KraneShares China Internet and Covered Call Strategy ETF KLIP - Active, equity, China, options overlay, thematic

1/11/2023 - Matthews Emerging Markets ex China Active ETF MEMX - Active, equity, emerging markets

12/13/2022 - GraniteShares 1.75x Long BABA Daily ETF BABX - Active, equity, leveraged, single stock

12/13/2022 - Virtus Stone Harbor Emerging Markets High Yield Bond ETF VEMY - Active, fixed income, junk bond, emerging markets

9/22/2022 - WisdomTree Emerging Markets ex-China Fund XC - Passive, equity, emerging markets

9/15/2022 - KraneShares S&P Pan Asia Dividend Aristocrats Index ETF KDIV - Passive, equity, Asia, dividend strategy

9/15/2022 - OneAscent Emerging Markets ETF OAEM - Active, Equity, emerging markets, ESG

9/9/2022 - Emerge EMPWR Sustainable Select Growth Equity ETF EMGC - Active, equity, emerging markets

9/9/2022 - Emerge EMPWR Unified Sustainable Equity ETF EMPW - Active, equity, emerging markets

9/8/2022 - Emerge EMPWR Sustainable Emerging Markets Equity ETF EMCH - Active, equity, emerging markets, ESG

7/14/2022 - Matthews China Active ETF MCH - Active, equity, China

7/14/2022 - Matthews Emerging Markets Equity Active ETF MEM - Active, equity, emerging markets

7/14/2022 - Matthews Asia Innovators Active ETF MINV - Active, equity, Asia

6/30/2022 - BondBloxx JP Morgan USD Emerging Markets 1-10 Year Bond ETF XEMD - Passive, fixed income, emerging markets

5/2/2022 - AXS Short CSI China Internet ETF SWEB - Active, inverse, thematic

4/27/2022 - Dimensional Emerging Markets High Profitability ETF DEHP - Active, equity, emerging markets

4/27/2022 - Dimensional Emerging Markets Core Equity 2 ETF DFEM - Active, equity, emerging markets

4/27/2022 - Dimensional Emerging Markets Value ETF DFEV - Active, equity, emerging markets

4/27/2022 - iShares Emergent Food and AgTech Multisector ETF IVEG - Passive, equity, thematic [Mostly developed markets]

4/21/2022 - FlexShares ESG & Climate Emerging Markets Core Index Fund FEEM - Passive, equity, ESG

4/6/2022 - India Internet & Ecommerce ETF INQQ - Passive, equity, thematic

2/17/2022 - VanEck Digital India ETF DGIN - Passive, India market, thematic

2/17/2022 - Goldman Sachs Access Emerging Markets USD Bond ETF GEMD - Passive, fixed income, emerging markets

1/27/2022 - iShares MSCI China Multisector Tech ETF TCHI - Passive, China, technology

1/11/2022 - Simplify Emerging Markets PLUS Downside Convexity ETF EMGD - Active, equity, options strategy

1/11/2022 - SPDR Bloomberg SASB Emerging Markets ESG Select ETF REMG - Passive, equity, ESG

Emerging Market ETF Closures/Liquidations

Frontier and emerging market highlights:

06/23/2023 - Invesco PureBeta FTSE Emerging Markets ETF - PBEE

3/30/2023 - Invesco BLDRS Emerging Markets 50 ADR Index Fund - ADRE

3/30/2023 - Invesco BulletShares 2023 USD Emerging Markets Debt ETF - BSCE

3/30/2023 - Invesco BulletShares 2024 USD Emerging Markets Debt ETF - BSDE

3/30/2023 - Invesco RAFI Strategic Emerging Markets ETF - ISEM

2/17/2023 - Direxion Daily CSI 300 China A Share Bear 1X Shares - CHAD

1/13/2023 - First Trust Chindia ETF - FNI

12/28/2022 - Franklin FTSE Russia ETF - FLRU

12/22/2022 - VictoryShares Emerging Market High Div Volatility Wtd ETF CEY

8/22/2022 - iShares MSCI Argentina and Global Exposure ETF AGT

8/22/2022 - iShares MSCI Colombia ETFI COL

6/10/2022 - Infusive Compounding Global Equities ETF JOYY

5/3/2022 - ProShares Short Term USD Emerging Markets Bond ETF EMSH

4/7/2022 - DeltaShares S&P EM 100 & Managed Risk ETF DMRE

3/11/2022 - Direxion Daily Russia Bull 2X Shares RUSL

1/27/2022 - Legg Mason Global Infrastructure ETF INFR

1/14/2022 - Direxion Daily Latin America Bull 2X Shares LBJ

Check out our emerging market ETF lists, ADR lists (updated) and closed-end fund (updated) lists (also see our site map + list update status as some ETF lists are still being updated as of Summer 2022).

I have changed the front page of www.emergingmarketskeptic.com to mainly consist of links to other emerging market newspapers, investment firms, newsletters, blogs, podcasts and other helpful emerging market investing resources. The top menu includes links to other resources as well as a link to a general EM investing tips / advice feed e.g. links to specific and useful articles for EM investors.

Disclaimer. The information and views contained on this website and newsletter is provided for informational purposes only and does not constitute investment advice and/or a recommendation. Your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content. Seek a duly licensed professional for any investment advice. I may have positions in the investments covered. This is not a recommendation to buy or sell any investment mentioned.

Emerging Market Links + The Week Ahead (June 26, 2023) was also published on our website under the Newsletter category.