When Emerging Market Growth Stock Investing Fails: Fundsmith Emerging Equities Trust plc to Liquidate

Terry Smith's ("the English Warren Buffett") mature growth stock investing style hit some snags when applied to emerging markets as he prepares to liquidate his Fundsmith Emerging Equities Trust plc.

In theory, investing in established and relatively mature growth stocks in emerging markets should be a winning investment strategy. After all, what might otherwise be a stodgy or slower growing mature growth stock in a developed market would still have significant opportunities for faster growth if based in a rapidly growing emerging market.

However, the recently announced plans for the Fundsmith Emerging Equities Trust plc (FEET:LN) to liquidate has highlighted the pitfalls of both funds and investors attempting to do growth investing in mature emerging market stocks.

Emerging Market Skeptic is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Terry Smith and the Fundsmith Emerging Equities Trust plc

Terry Smith, the founder and chief executive of British fund manager Fundsmith, is probably not well known outside of the UK where he is referred to as "the English Warren Buffett" for his style of growth investing. His core Fundsmith Equity Fund (FSMEQTA:LN) could best be described as an English version of the Fidelity Magellan Fund (MUTF: FMAGX) managed by Peter Lynch for having a strong early performance and rapid growth (thanks in part to good marketing). Its also the largest UK retail fund at around £24bn in size.

On June 25, 2014, Smith launched his Fundsmith Emerging Equities Trust plc which maintains a portfolio comprising of 25 to 40 emerging market stocks. His bullishness about emerging markets even reportedly had him saying that “the emerging markets trust should be able to outperform Fundsmith over 10 years."

However and in a note published on September 14th, 2022, the Board of FEET announced their intentions to liquidate the emerging market fund. Smith (who apparently has not managed the fund’s day-to-day since 2019) was quoted as saying:

"We have always maintained that we would only run funds where we felt we had a particular edge that would allow us to deliver superior risk-adjusted returns. Whilst FEET has made a positive return since launch in 2014 it has fallen below our expectations and, unlike other fund managers who might seek to hold onto the fund for the sake of the fee income, we feel it would be in the best interests of shareholders to receive their investment back in cash through a liquidation of the portfolio and wind-up of the Company."

Given the underperformance since launch, it may be said then that the fundamental thesis underpinning the launch of the trust was wrong, that is, the idea that emerging markets would outperform developed markets, and that this would be reflected in stock market growth.

Smith has always been a confident and forthright character, and indeed Smith lives in an emerging market economy (Mauritius), but the failure of this trust may be a function of the fact that the skills and process the fund manager uses in developed markets to find the type of large cap, mature businesses he craves, simply do not work in the emerging world when it comes to stock selection.*

*All bold emphasis will be ours…

Why this investing strategy failed when Smith applied it to emerging markets is worth a much closer look.

On the surface, FEET’s core focuses (as outlined in its Factsheet dated August 31, 2022) makes investment sense when it comes to investing in emerging markets:

To provide shareholders with an attractive return by investing in a portfolio of shares issued by listed or traded companies which have the majority of their operations in, or revenue derived from, Developing Economies and which provide direct exposure to the rise of the consumer classes in those countries or to the broader social and/or economic development of those countries.

And:

The Investment Manager intends to find companies which make their money by a large number of everyday, repeat, relatively predictable transactions. Its strategy is to not overpay when buying the shares of such companies and then do as little dealing as possible in order to minimise the expenses of the Company, allowing the investee companies' returns to compound for Shareholders with minimum interference.

Unpredictable cashflows tends to be a common problem for all companies operating in emerging markets. Its a major reason why emerging market stocks tend to pay dividends on a half year or annual basis rather than a quarterly basis. So again, FEET’s focus on emerging market consumer orientated stocks with predictable cashflows makes investment sense.

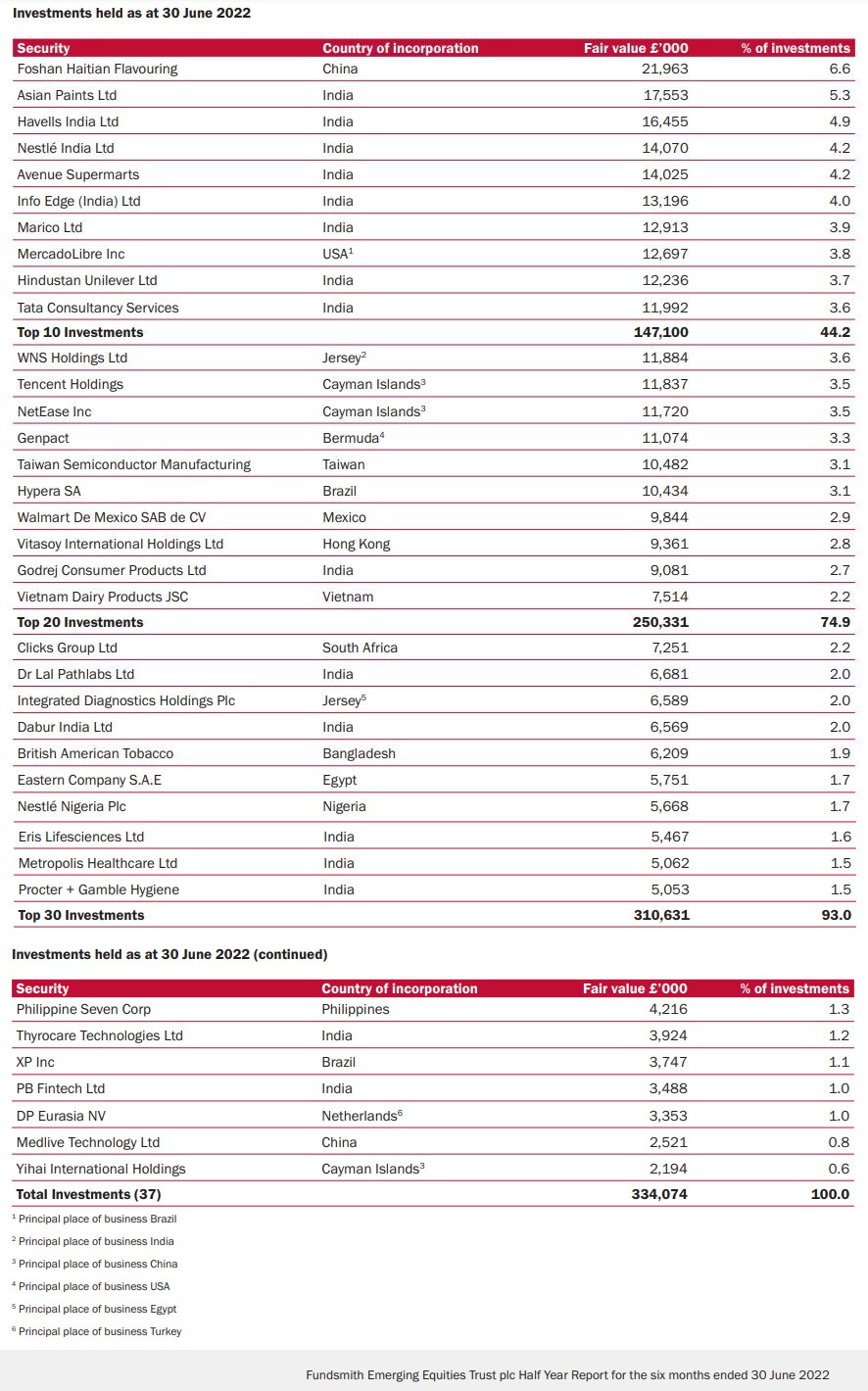

The Factsheet also had this portfolio comment for the month with the top 10 holdings all being solid growth stock names (NOTE: I have added tickers and weblinks to the company investor pages):

The Investment Manager will avoid the financial sector and heavily cyclical sectors such as construction and manufacturing, utilities, resources and transport, and will instead focus almost exclusively on consumer stocks and in any event only on stocks in companies which will benefit from the rise of the consuming class in the Developing Economies.

The companies in which the Company will seek to invest have relatively predictable revenues and low capital intensity, and correspondingly high returns on capital. The targeted companies will also deliver most or all of their profits in cash. They will have defensible and strong market positions, typically derived from a combination of brands, trademarks and distribution systems or networks. The Investment Manager believes this combination will deliver compound growth in shareholder value over the long term.

Once again, everything outlined above makes investment sense - except when many emerging market consumers are getting hit by a double whammy of inflation (as in rising energy and food costs) and depreciating local currencies. When that happens, consumers (no matter where they are located) tend to spend less money; or they buy generic non-branded consumer items or substitutes made locally; or they go without the product.

And finally:

The Investment Manager is also cognisant of the additional risks of investing in Developing Economies as opposed to developed economies, both in terms of the countries in which the companies operate and the standard of corporate governance within the companies themselves. The Investment Manager will take into account the degree of economic freedom, particularly the measure derived by the Heritage Foundation, of the country in which the companies are listed and/or operate in assessing the risks of any particular opportunity.

As you can see, the Fundsmith Emerging Equities Trust plc has avoided China and is heavily invested in India - an investment strategy that has weighted down recent performance.

IF you believe in such rankings, neither of these rankings are particularly great (and the Factsheet’s mention of “degree of economic freedom” might just be for marketing and ESG purposes). This means we need to consider investor or market perceptions about these two countries.

Life + Liberty Indexes Founder Perth Tolle brought up BlackRock CEO Larry Fink's 2011 Bloomberg interview, in which he said that, "Markets don't like uncertainty. Markets like, actually, totalitarian governments where you have an understanding of what's out there."

Fink had also added that “democracies are messy with opinions changing back and forth…”:

In other words, markets (or rather large western asset management firms like BlackRock and their CEOs who move the markets) LIKE authoritarian China over democratic India (where they have a sometimes messy uncertainty called elections with “opinions changing back and forth……”).

The article also pointed out:

For instance, in the S&P 500, sophisticated and gigantic institutional investors often trade between each other, but international markets have more retail stockholders.

"You're not going to earn alpha from anyone, right? Not consistently," Rayliant Global Advisors Founder Jason Hsu said. "In retail markets, especially the Asian retail markets, there's retail gambling. In China, it's 85% retail. In Taiwan and South Korea, it's 50% to 60% retail. So you kind of have a willing reservoir of losers on the other side."

With one billion+ people, there are many retail investors in India and plenty of them will inevitably know more about what is going on in the local stock market, with local consumer brands (or local buying habits), in the economy and/or with a particular local stock than an international fund manager like Smith - even if he is living in Mauritius making regular visits to the country.

The Company underperformed the index during the period under review, primarily due to investor sentiment moving away from more expensive ‘growth’ companies. There has also been a net outflow of funds from emerging markets in anticipation of US dollar strength in a rising interest rate environment. India, which had seen strong fund flows in 2021 into overly buoyant capital markets saw a sharp reversal in this trend.

India is also a commodity importer at a time when commodity prices are rising. In other words, India (or rather its consumer stocks) is probably the wrongemerging market to be invested in when commodity prices are rising and potentially the right one to be in when commodity prices are falling.

Nevertheless, the Half-Year report noted:

For reasons we have stated in the past, the Company is unlikely to invest in financials, materials, energy and real estate which were the four areas of the index to perform positively in the first half of the year. The Company’s split of investments, as measured by the Global Industry Classification Standard (GICS), is shown below;

Avoiding those four key sectors outright has also proven to be a problem for FEET. Those tend to be the primary sectors where you might find mature emerging market growth stocks benefiting from rising commodity prices rather than suffering from them.

The Half-Year report went on to note:

The nature of the companies we typically buy gives us a degree of insulation against inflation, although of course we are not immune. Despite us generally seeking to avoid comparison with the index, the companies which the Company owns have significantly higher gross margins than that of the index others seek to compare us with. Those gross margins help insulate a business against input cost pressures. All other things being equal, a 5% increase in the cost of goods sold for a business with 50% gross margins will reduce profit by 5%. A 5% increase for a business with a 20% gross margin will reduce profits by 20% - four times as much.

In addition, the majority of the businesses we own are less likely to see consumption forgone in more chastened economic times; you may opt not to go on holiday in more difficult financial times, but I strongly suspect you will continue to brush your teeth. The businesses we own also typically have strong market positions, giving them a degree of pricing power.

As mentioned earlier, emerging market consumers under pressure from commodity prices and falling local currencies can switch to generic brands or alternatives or go with out when hard pressed.

The next paragraph is more interesting and worth keeping in mind if you decide to invest in emerging market consumer stocks:

The businesses we own will also typically have professional procurement operations and will be major consumers of commodities. As well as giving them buying power and the ability to find alternate supply, we would also suggest that in times where raw material supplies are tight, they are at a significant sourcing advantage, both in terms of price and availability relative to smaller and, quite often, formal manufacturers.

The above may be true, but when commodity prices are rising rapidly and the value of local currencies are going in the other direction, even the biggest and most professionally managed procurement operation will struggle.

And then there is this paragraph:

Inflation in emerging markets has also been driven by the impact of terms of trade on those countries that either do not have developed export economics (China, South Korea & Taiwan) or are major resource exporters (Indonesia, Brazil and South Africa). Terms of trade for an emerging (and frontier) market economy can deteriorate rapidly in a high inflationary environment, as countries which are net importers and running sustained deficits see higher import costs feeding through into a weaker currency, with the subsequent impact of a further increase in trade deficits and even further currency weakness. It is not uncommon for governments to then try to reduce the economic pressure on their populations by the use of subsidies - leading to both market distortion and increased government deficits, funded at ever-higher borrowing costs.

Note: India heavily subsidizes all sorts of things e.g. for farmers to grow rice and wheat as well as their fertiliser and diesel for fuel water pumps. Fuel, electricity and transportation (e.g. Indian Railways) are also subsidized and have market distortions.

On a side note, the half year report did have this interesting comment for anyone thinking of investing in Nigeria (an interesting African emerging market) or perhaps in the Nigerian ETF:

Nestlé Nigeria is our sole holding in Nigeria after having exited the brewing sector in the country on fiscal concerns. Nigeria, in our opinion, remains very much a curate’s egg for investors – ticking all the demographic boxes (the country’s population is forecast to double to 400m by 2050) but consistently underperforming in policy implementation. The company reported very strong sales performance in the first half of the year and retains both attractive margins and returns.

NOTE: A "curate's egg" is a British idiom where something is described as partly bad and partly good - a good idiom to use for many an emerging or frontier market.

Finally, here is a list of Fundsmith Emerging Equities Trust plc’s half-year portfolio holdings (followed by a list with web links that can also be cut and pasted or sorted in Excel etc) as some individual stocks (those with listings in New York or London) may still be a fit for a retail investor’s emerging market component of their portfolio:

NOTE: The ticker links prioritizes NYSE/NASDAQ listings, then OTC listings (which may be the pink sheets) and then local exchange listings. Country names link to our lists of ADRs or ETFs with more resources for the specific country:

Again, plenty of mature solid emerging market growth stocks can be seen in the above list that might be worth checking out further.

Key Takeaways About Mature Growth Stock Investing in Emerging Markets

Here are some key takeaways from Terry Smith closing his Fundsmith Emerging Equities Trust plc or about applying growth stock investing to emerging markets:

Trying to build an active fund portfolio of 25 to 40 good mature emerging market growth stocks will be a challenge for any fund manager - especially one with severe constraints on what sectors they invest in. In other words, FEET’s strategy was a flawed one at the fund level, but still might work for a retail investor or small family office operating with a fraction of the capital looking to make a couple of investments.

India has enormous potential and comes without many of the problems China is or will soon be grappling with. HOWEVER,the market (as in BlackRock et al) is currently in love with (authoritarian…) China versus (democratic…) India…

If you do your research as an individual retail investor, you can definitely find a couple of good mature growth stocks in a country like India that might end up beating the selections of a market that still prefers to invest in China. But again, you are not going to be able to fight a market that prefers China if operating at the scale or with the amount of capital a fund like FEET operates at.

Financials aside, don’t forget about retail investors in emerging markets and the fact that they would still know more about what is going on locally than any foreign based fund manager or the market (as in BlackRock et al).

Again, there are some good emerging market growth stocks in the FEET portfolio - some of which might make sense for a retail investor with a strong stomach for emerging market investing risks. And I would give FEET’s fund managers the benefit of the doubt that they have done some on-the-ground research and due diligence about these stocks and their financials.

Nevertheless and if you are thinking of investing in an active emerging market fund, keep the problems faced by the Fundsmith Emerging Equities Trust plc in mind when you review the fund’s strategy.

I have changed the front page of www.emergingmarketskeptic.com to mainly consist of links to other emerging market newspapers, investment firms, newsletters, blogs, podcasts and other helpful emerging market investing resources. The top menu includes links to other resources as well as a link to a general EM investing tips / advice feed e.g. links to specific and useful articles for EM investors.

Disclaimer: EmergingMarketSkeptic.Substack.com and EmergingMarketSkeptic.com provides useful information that should not constitute investment advice or a recommendation to invest. In addition, your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content.