China's Problems That Few People Talk About (And Investor Implications)

If you build it, you must maintain it. What happens when land use rights start to decay? Does Beijing even know what the real numbers are (b/c “heaven is high and the Emperor is far away")? etc.

China observers often fall into two camps:

The China cheerleaders (who are probably on a China payroll)…

The “coming collapse of China” crowd (who are probably on some anti-China or anti-CCP payrolls)...

In the past, China’s cheerleaders include much of the American corporate business media (when they are told to be cheerleaders), corporate America, the big Wall Street players, and “experts” like Shaun Rein (who was even the subject of a parody article, Shaun Rein to be ‘discontinued’: CCP, by a defunct China parody site that’s still on Twitter) of the China Market Research Group (CMR). All are China cheerleaders thanks to their extensive investments or business dealings there. And some individual China experts, academics, or journalists are no doubt directly or indirectly paid by the CCP to promote China.

Then there is the coming collapse of China crowd personified by Gordon G. Chang and his 2001 book, The Coming Collapse of China (Full Disclosure, I have not read any of his books…), along with people like Peter Zeihan. The problem with this crowd is how they have been predicting the coming collapse of China for more than two decades now.

Many (like the Falun Gong-affiliated Epoch Times, who otherwise writes thorough and well-researched articles) are probably on the payrolls of anti-CCP groups or individuals. And the payroll is getting bigger:

500 million dollars. That's the sum of money the US congress planned to allocate to churn out negative news coverage on China. First reported by American Prospect on Feb. 9, the bill was stuffed into the China-centered America COMPETES Act that just got passed by the US House of Representatives earlier this month. A majority of the half-billion-dollar fund will go to the US Agency for Global Media (USAGM), a state-run media service that oversees Voice of America (VOA), Radio Free Europe (RFE), and Radio Free Asia (RFA), which have a record of "blurring the line between objective news coverage and pro-American propaganda," the article wrote.

Having travelled enough around China (see my YouTube China travel channel), I tend to fall somewhere between the two extreme camps. On the one hand, the infrastructure is impressive, and the CCP (like them or not) has clearly raised people's living standards over the past couple of decades.

On the other hand, China can feel like a cross between a Potemkin Village and the Matrix because the country clearly has serious problems - just like the USA and the EU have serious political and economic problems (with the EU mostly likely to collapse first).

The General Crisis Watch Substack (which now appears to be inactive) has an excellent series of articles that go in-depth about China's problems (The Coming Removal of the Mandate of Heaven, Part 0: Founding Myths, Part 1: Food, Part 2: Water, Part 3: Political Infighting, and Part 4: Oil). I don’t necessarily agree with them on all their points and I do not want to cover the same ground again.

However, the following are problems or issues faced by China that few experts seem to talk about that I will cover in this post:

If You Build It, You Must Maintain It (And Eventually Replace It)…

For Westerners, China is Often a Potemkin Village…

What Will Happen When Land Use Rights Start to Decay and Run Out?

What Will Happen to Property Values as China’s Population Falls?

To Solve Demographic Problems Like Falling Birth Rates, You Must Give People Reasons to Live and Reproduce…

Does Beijing Even Know What the Real Economic Numbers Are (Because “Heaven is High and The Emperor is Far Away…”)?

When Xi Talks About “Common Prosperity,” etc. He Means It…

Implications for Investor Portfolios…

All of these problems or issues will have implications for investors in China and their portfolios.

If You Build It, You Must Maintain It (And Eventually Replace It)…

There is no denying that China now has some of the best infrastructures in the world. But when anti-China westerners talk about China’s infrastructure and construction in general, they look for every example of shoddy construction they can find. However, you can find plenty of examples of shoddy construction all over Asia.

The real problem China (along with the rest of Asia) will face is maintaining all the gleaming high rise buildings and infrastructure. For example, I am renting a condo in Kuala Lumpur (Malaysia) in a well-maintained complex built by a reputable developer (who left enough money in the sinking fund) almost twenty years ago. All the elevators were recently replaced because they could no longer easily find spare parts to maintain the original ones. But this is nothing unusual - a quick Internet search reveals that elevators have a 20 to 25-year lifespan.

I am also starting to have problems with my toilets as their wax seals (which cost a couple of Ringgit) are wearing out (and it sounds like the building may have further plumbing problems involving the pipes or waste water disposal system…). A quick Internet search reveals that wax seals have a 20 to 30-year lifespan. In a wooden and stucco house, this would be a minor repair. However, in a concrete and steel high rise with tiled bathrooms, a plumber has already told me this will not be an easy (nor cheap!) repair. [I could go on by mentioning my other maintenance problems e.g. my sliding glass door problems - another not so easy or clear fix in a concrete high rise… Or most of my window handles - now replaced with ones that break even faster…]

Kuala Lumpur itself recently opened another MRT line. However, in October, FMT reported that Rapid Rail Sdn Bhd (the sole operator of five rapid transit lines) had 22 of the 362 elevator units not functioning, while 49 out of 707 escalators were out of order.

Citing recent disruptions on one transit line, transport minister Loke Siew Fook remarked last December:

“We have the best public transport facilities. Since the time of former prime minister Abdullah Ahmad Badawi, we’ve been saying that we have first class infrastructure but when it comes to maintenance, we’re still a third world country.”

[In Malaysia’s defense, infrastructure maintenance seems no worse than elsewhere in Asia or the rest of the world…]

Meanwhile, at KLIA, the 1.2 km Aerotrain system between the two airport terminals opened in 1998. After a growing number of breakdowns shuttling more than 300 million passengers in 23 years of service, the trains and the entire track system are getting replaced for RM700+ million.

I won’t even comment on this particular “maintenance” situation I encountered in KLIA arrivals back in 2017:

Now imagine all the elevators, toilets, high rise buildings, high-speed trains, and other infrastructure in China that needs expensive continual maintenance and eventual replacement.

And then there is all the infrastructure being financed or built as part of the Belt and Road Initiative (BRI) which (host countries?) need to maintain (and eventually replace).

When economies and populations are still growing, performing expensive maintenance and replacements should not be a financial burden. But what happens when the economy and population are no longer growing? And what about the so-called ghost cities the Western media likes to talk about?

In the case of my condo complex, condo dues payment delinquencies and defaults have risen as expat tenants left due to the pandemic, and landlords struggle to replace them (often with guest workers…). And some landlords or owner occupiers are (no doubt) struggling financially after COVID lockdowns weakened the economy.

Again, I am lucky the building is still well managed (some expat owners are very proactive and involved on the management committee), and the developer left enough money in the sinking fund to deal with major maintenance issues like the elevators. But when I look around my neighborhood at other buildings around the same age, it’s clear which ones are being properly maintained and which are not (albeit in the city center, these are often the investment or AirBnB condo complexes that are not owner occupied)…

Now imagine these scenarios playing out in China and other cities across Asia…

For Westerners, China is Often a Potemkin Village

Some years ago, I chatted with a Brazilian (of Taiwanese descent) acquaintance. He thought there could be no place more corrupt and bureaucratic than Brazil (or with businessmen, oligarchs, and government officials more voraciously greedy and ruthless than Brazilian ones). Then he went to work for a relative's business interests in China. What he experienced working there (as an Asian from Brazil) shocked him as he said that doing business there was worst than "dealing with Mafia!"

If he were a White Westerner or American or working for an American MNC, my Brazilian acquaintance would have had a much different experience. Why? Remotely sophisticated Chinese officials and businessmen are probably aware of laws like the Foreign Corrupt Practices Act and of the need to use a more “indirect” approach (e.g. through local intermediaries or the legal/regulatory system) when they want "something" out of Westerners and their businesses (especially the MNC ones). With non-westerners and their businesses, they are free to take a more “direct” (and Mafia like) approach…

What Will Happen When Land Use Rights Start to Decay and Run Out?

Since China is a Communist or Socialist country, the Chinese government (or “the people”) owns all the land, and individuals own the buildings. There is a system of land use rights where you can buy and sell the right to build something on urban land (there are different rules for agricultural land).

However, these land use rights come with different lengths of time attached to them:

Therein lies the problem. Nobody knows what will happen when land use rights expire. But everyone assumes the government will come up with something… that is reasonable… And what that will be is anybody’s guess…

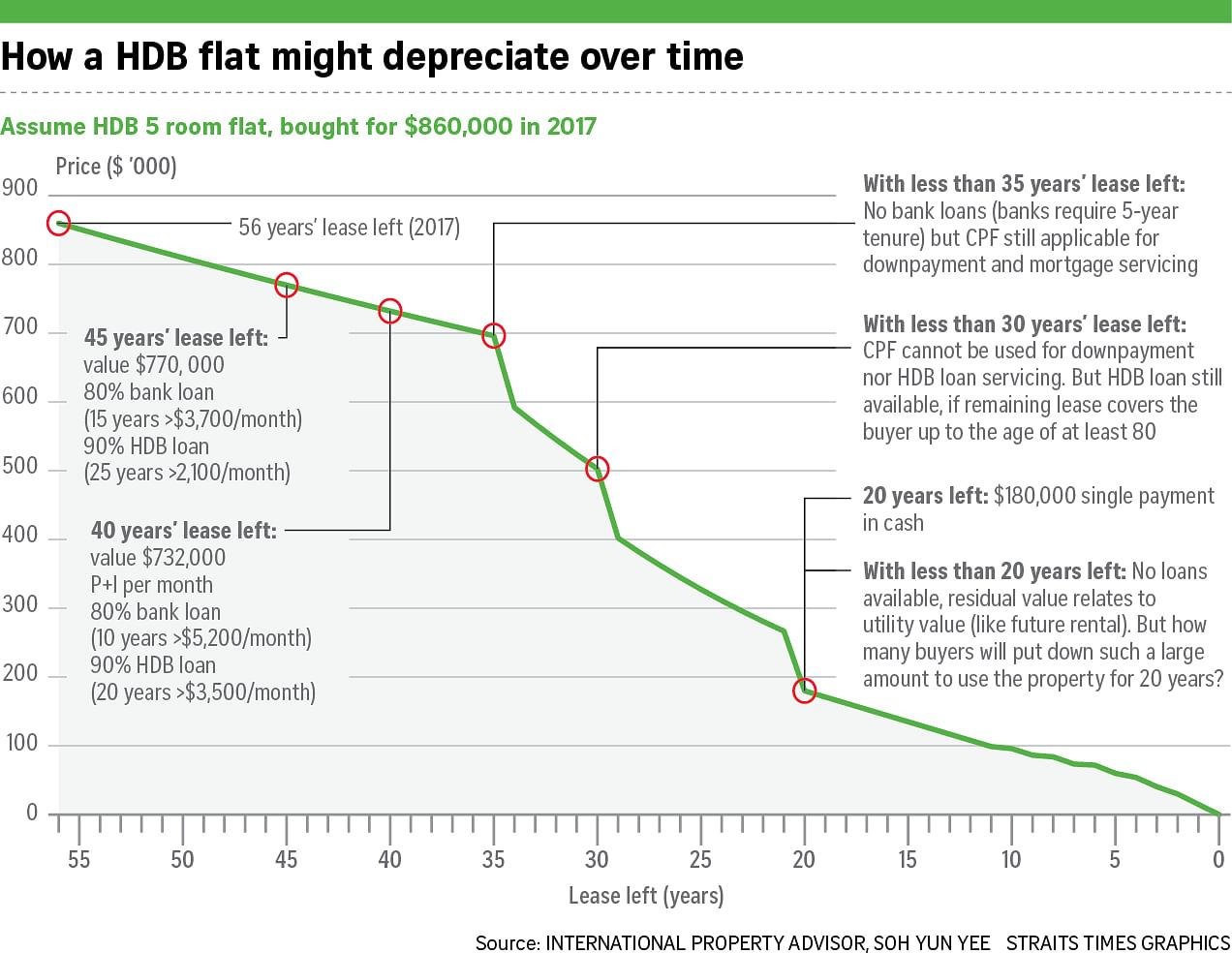

However, before any land use rights expire, their values will start to decay (e.g. refer to any old Accounting and Finance 101 textbooks you may have lying around). Singapore, where most citizens live in Housing & Development Board (HDB) flats on 99-year leases, is already grappling with this problem:

A question of time: The great HDB lease decay debate (Business Times)

The idea that the value of one's home can eventually run down to zero is a terrifying thought, one which increasingly more researchers are studying in an attempt to quantify the relationship between dwindling leases and Housing & Development Board (HDB) resale prices. Crudely put, the studies so far have pointed to a unanimous finding - that the decline of resale prices is certain as the length of lease decreases, especially as limits on financing kick in.

Buying an old HDB flat? Here are some things to consider (The Straits Times)

Data shows that buyers don't mind old HDB flats, paying similar prices for units whether they are 25 or 50 years old.

But beware a potential sharp fall when flats cross 64, with less than 35 years of lease remaining. That's when financing restrictions kick in.

Minister for National Development Lawrence Wong cautioned last month that the vast majority of flats will be returned to HDB when their leases run out.

Flat buyers would best not think of the 99-year lease as a clock that can be reset, The Straits Times' Wong Siew Ying wrote in a commentary.

Will you still love your HDB flat when it's over 64? (The Straits Times)

Data shows that buyers don't mind old HDB flats, paying similar prices for flats whether they are 25 years old or 50. But beware a potential sharp fall when flats cross 64, with less than 35 years of lease remaining. That's when financing restrictions kick in.

Govt taking back 191 homes in Geylang when lease ends (The Straits Times)

In a first for residential properties in Singapore, 191 private terraced houses in Geylang Lorong 3 will be returned to the state when their leases run out at the end of 2020, with no extension allowed.

Are Singapore’s 99-year leases and falling prices for older flats about to become an election issue? (SCMP)

Public housing owners in Singapore fear heavy losses as their leases run out

But with an election looming, the government will surely step in. Won’t it?

Singapore’s government already has a variety of (complicated…) schemes in place to address these issues to ensure affected HDB flat owners have time to make plans. However, Singapore has a population of only 5.6 million people with a relatively efficient and corruption-free government.

Now imagine (in a couple of decades) trying to sort out land use rights in a country (that will still have a population) of around one billion people. But do not worry. China’s government will come up with something "that is reasonable..." It's just that (right now) nobody has any idea what that will be…

What Will Happen to Property Values as China’s Population Falls?

As if China won’t have enough problems dealing with what will happen to land use rights a couple of decades from now. They will approach expiration after the country’s demographic time bomb has exploded:

What happens to property values when a country’s population is in freefall? The Roman Empire and plague stricken Europe are too far back in time to provide appropriate reference points.

However, we can look to Japan and the Konichi-Value Substack (focused on investing in Japan) where Rei Saito has some good insights (emphasis his):

Should I Invest in Real-Estate in Japan? Three Arguments Against (Konichi-Value)

In the second part of this 3-part series, I tell you the best arguments for why you should NOT invest in real estate in Japan

This is bad for real estate pricing, especially considering that at average, a 1% decrease in population has a 5% decrease in property prices (Hashimoto et al., 2020).

However, major cities and popular tourist destinations in Japan are experiencing rapid population growth as people from rural areas are migrating for better opportunities.

In fact, despite the declining population since 2009, the total number of households in Japan continues to increase.

This is due to the share of “three generation” type families declining dramatically as younger people move into major cities, whereas the sum of one-person and couple-only increased to exceed 50%. Less people living together = more demand for property!

So in the short- to medium term (10 to 20 years), property prices in major cities will likely go up with the population influx, but eventually, if the population decreases at the same rate, the influx will stop and they will also fall…

[Contrarian Investing] How Tokyo Avoided the Affordable Housing Crisis (Konichi-Value)

Tokyo's population is growing faster than New York and London, but its housing prices are less than half. How?

News headlines might make you believe that this is due to Japan’s declining and aging population. After all, less people means less competition for existing housing.

But this isn't the case; the population of Tokyo is still growing! In fact, the population of the city grew by about 1 million people in the past 5 years. This is a higher growth rate than New York and London, and yet rents only rose by 20% compared to over 100% for those cities.

Part of the answer is surprisingly simple, yet very complex: Tokyo has kept the cost of living stable because a lot of housing is being built!

When applied to China, a 1% decrease in the population having a 5% decrease in property prices sounds like a nightmare - especially when combined with decaying land use right values. But as Rey pointed out, Japan’s property values have held firm or increased in major cities and popular tourist destinations.

Issues surrounding land use rights aside, property values in centrally located areas of big (mostly coastal) Chinese cities should hold their value. I also suspect that fertile agricultural land will also hold its value because China will still need to import food for the foreseeable future.

The biggest losers? Everyone who owns property in secondary cities or not-so-good or convenient areas of (or just outside) big Chinese cities. And they will not be happy about that...

They will also not be happy when it comes time to replace elevators (and toilet seals… sliding glass doors… plumbing and wastewater systems…) - assuming there are still enough residents to pay any necessary special assessments.

To Solve Demographic Problems Like Falling Birth Rates, You Must Give People Reasons to Live and Reproduce…

Much has been written about China’s demographic problems caused by their “one child” policy. The following chart showing India’s population growth illustrates the trajectory of China:

Putin’s Russia and Orbán’s Hungary are the only two countries I can think of that have achieved some success in slowing population decline by encouraging traditional (Christian-based) values and religion along with monetary awards or tax breaks for having children. However, neither Russia or Hungry appear to be above the replacement rate yet.

Then there was Romania under Ceausescu and his Decree 770 which restricted abortion and contraception. The birthrate surged right after the decree was signed - only to return to its previous trend as people found ways to circumvent it while those who couldn't would abandon their unwanted children into state-run orphanages.

Why is it nearly impossible to reverse declining populations? Educated urban professionals (globally…) simply do not want to have many children - if any at all. An article in The Spectator (Baby bust: China’s looming demographic disaster) also sums up the predicament facing China and Chinese families (emphasis mine):

Chinese families with their own apartments find that the space is tight and that having more than one child is tricky. Government propaganda is no substitute for spare bedrooms and spacious living quarters, which are in short supply, as is affordable childcare.

China’s middle class – the professional, high-skilled workforce on which future growth depends – has become wary about the future. A new phrase is circulating on social media – ‘graduation then unemployment’. (It rhymes in Chinese – biye jiu shiye.) One reason for China’s growing unemployment is the immediate effects of the Covid lockdowns: the private sector, the engine of China’s economic growth, has found it difficult to create jobs when it can’t predict business conditions.

Then there is this tweet that I have seen as a meme:

You can decide whether or not the incident happened or whether this feeling is widespread among younger Chinese.

With that said, pronatalist policies timed to take affect when previous big population cohorts enter childbearing years can help avert demographic catastrophe a couple of decades down the road as this Twitter thread concerning Russia [Trigger Warning: The thread may contradict western narratives!] and these two tweets from it point out:

And:

As with western and other East Asia countries, it appears China has missed the boat and it’s demographic problems will be extremely difficult to reverse.

One idea might be for many of the workers who have moved from the countryside to work in factories in the cities to return home and turn the countryside into a baby factory. After all, small towns and rural areas are much better environments for raising children and large families (e.g. you have more space, less pollution, can grow your own food, etc.). And as exports fall, automation takes hold, and new construction projects slow, something will need to be done to help those who loose their jobs.

However, I am not aware of any Chinese policies to encourage a reverse migration back to the countryside.

Does Beijing Even Know What the Real Economic Numbers Are (Because “Heaven is High and The Emperor is Far Away…”)?

Anybody who shops at a supermarket in a Western country knows what the real rate of inflation is and it’s not what governments, politicians, or the corporate business media tells us. We also know how bad, for example, the US economy is thanks to alt-experts and websites like John Williams' Shadow Government Statistics.

Consider his Alternate Inflation Charts that better match the price jumps or shrinkflation you are seeing at American supermarkets:

Here are some of his other “alternative” charts for key economic stats:

Outside of China, there are also sites like Layoffs.fyi tracking layoffs and alternative media who still investigate and report stories like this:

With the inflation numbers, the US government has quietly been removing everything from the calculation that goes up in price and “replacing it with rubber bands” (in the words of one alt-expert I recently heard in a podcast…) or whatever is falling in price. And this has been going on since the Jimmy Carter Presidency - if not much earlier…

However and as Aleksandr Solzhenitsyn once said:

We, along with our leaders in places like Washington and Brussels, know what the real numbers are and how bad they are - even if the corporate media fails to report them.

What is far more worrisome is whether or not the leaders in Beijing even know what the real numbers are given the type of political system China has. For example: If Beijing sets a target of 5% growth, do you think provincial or local government officials are going to give a number that differs from the target rate?

Speaking of numbers that might be fake and hidden from Beijing:

China Begins Nationwide Push to Reveal Hidden Government Debt (BNN Bloomberg)

And here is a speculative piece from the anti-China crowd that’s still worth pondering (included in our May 8th post):

China, population, and lies (American Thinker)

Note: This is an interesting anti-China piece. Apparently, there are incentives for local governments to inflate birth #s, etc: Researcher questions China's population data, says it may be lower (Reuters).

Recently, the Chinese government admitted that it had "overcounted" the Chinese population by about a hundred million.

Actually, nothing of the sort happened. Chinese announcements concerning anything are generally soaked in various mixtures of bogosity, and this one is no exception. A hundred million is not a rounding error. There was, in fact, no error at all. The Chinese simply lied about their population at some unknown point in the past and continued lying until it became inconvenient or impossible to sustain.

So, comrade, you're telling me that China started the 20th century with just under 400,000,000, suffered something on the order of 463,139,000 excess deaths (remember, we're not counting ordinary, everyday mortality here) across the ensuing 80 years, and still wound up with 1.4+ billion people?

I call 废话. I say it is mathematically and physically impossible.

I don't think China has 1.4 billion. I don't think it has a billion. In fact, I have some doubt that it ever reached a billion.

The above points remind me of a famous Chinese proverb:

When Xi Talks About “Common Prosperity,” etc. He Means It…

Years ago, I would attend an annual Chamber of Commerce function where an economist (I believe from BNP Paribas) would give an overview of what was going on in China. He more or less explained Chinese monetary policy, etc. by using a salami cutting analogy: The Chinese tell you how thick they will cut the salami and proceed to methodically cut it at that size - no matter how loud the western media or economists scream that they will (or need to…) pivot and cut it to a different size. When it comes time to change the salami’s thickness, they tell you and the process is repeated…

Our August 1st post covered an interview where a fund manager discussed how they had avoided investing in education companies. They were being told by those in the business how they would not be able to list or sell their companies and that curriculum was a sensitive subject for Xi.

Unlike with western politicians, when Chinese leaders like Xi talk about “common prosperity” and the wealth gap being a problem, they mean it. And unlike western politicians, they no doubt have plans to do something about it...

Implications for Investor Portfolios

Our EM Fund Stock Picks & Country Commentaries have covered fund strategies for investing in China:

Our August 1st post covered an interview with an experienced China VC fund manager who discussed what he has learned from investing in China and how the foreign investment crowd has been consistently wrong there (e.g. foreign tech companies or their investors using the wrong business models, now they are chasing chasing AI mirages, etc.). Again, from listening to people on the ground, he avoided investing in the online education sector.

The same post covered another interview where a fund manager said looks for stocks in industries that are as “far away” from those that the Chinese government might have an interest in. He likes consumer discretionary stocks; but in China, that means trying to figure out what could go wrong e.g. he stays away from any restaurant stock serving unhealthy fried food should the government take an interest in limiting that.

Finally, a fund manager in another interview said that when it comes to investing in China, you need to sit down and try to understand the five and ten year strategies of the Chinese government and then invest along side of them. IF you can do that, then you usually make good returns.

In our July 25th post covered another podcast interview where a fund manager discussed how they pick good quality Chinese companies or rather how they cut a list of 9,000 Chinese stocks down to a more manageable list of about 700 quality stocks. Surprisingly, he commented that Twitter is a good place to monitor what is going on in China e.g. the COVID protests were being reported on there almost instantaneous despite China having a closed Internet.

Our July 18th post covered a particular framework used in India that I suppose could be modified for China:

Our July 11th post covered comments from a fund manager who was taking Chinese tech stocks out of his doghouse simply because the sector is too important for China. He also noted how self-destructive China has behaved towards their tech sector and doubts it will continue.

The post also noted general comments from a fund manager about how most emerging market investors are investing in the exact same investments. And these trades are crowded…

Our July 4th post detailed a couple of funds who have talked about focusing on the Chinese automation (as in industrial automation, robotics, digitization, etc.), healthcare (including biotech, medical devices, etc.) and/or consumer goods or services sectors. While these sectors make sense, I noted how the herd has moved into these stocks as it’s reflected in their recent performance charts.

Our June 27th post covered how one fund has pointed out how the benchmarks for investing in China includes far too many stocks that foreign investors may not want to invest in e.g. state-owned enterprises (SOEs) or state-influenced companies along with cyclicals or industrials. This fund divides their China holdings into three categories and/or sectors further discussed on the post.

The post also covered how another fund article noted how some global players in the spirits industry offer investors instant diversification across product lines and emerging markets - including China and India where they are key players. Investing in them (or some of their listed subsidiaries) rather than, for example, China based Kweichow Moutai, tends to make more sense.

Our June 13th post covered a fund who’s China stock picks fall under one of a couple of themes they have for the country. But as mentioned earlier, the foreign fund herd has moved into many of these stocks already.

Our March 21st post covered how one fund explained how “getting China right” will almost certainly be the single most important factor going forward for them. Their strategy is to identify the next Asian Warren Buffet or Peter Lynch who have on the ground experience investing in China (plus share the same investing philosophy) and to allocate them funds to invest. Instead of following the international fund herd into a few large cap stocks, these local fund managers generate original investment ideas involving well-managed smaller and medium-sized Asian or Chinese stocks based on their own extensive research and due diligence.

One idea to consider that ties back into the idea, “if you build it, you must maintain it…:” Property or infrastructure management or maintenance stocks e.g. all residential property (sold or unsold) will need to be maintained. There are some local property management companies in China and some are listed (One was covered in this post: CMBI China and Hong Kong Equity Research (June 2023)).

China does not need to build too many more high speed trains, subway lines, etc. (which will impact construction related firms who can’t get overseas projects) but they will need to maintain what they already have - something governments are usually terrible at doing.

Many local governments in China are also cash strapped as they ran (or nearly ran…) out of money during the COVID lockdowns or previous infrastructure spending binges. They have yet to figure out an appropriate local funding mechanism (other than jacking up school or infrastructure use fees, regulatory shakedowns, etc.) in a country where the state technically owns all the land. Perhaps they will be forced to sell off infrastructure to REITs or other types of property/infrastructure investors or outsource it’s maintenance.

Finally, are there any other sector or stock ideas or investing strategies for China that I may have left out? Or for that matter, China problems that are often overlooked?

Fell free to let me know in a comment…

Check out our emerging market ETF lists, ADR lists (updated) and closed-end fund (updated) lists (also see our site map + list update status as some ETF lists are still being updated as of Summer 2022).

I have changed the front page of www.emergingmarketskeptic.com to mainly consist of links to other emerging market newspapers, investment firms, newsletters, blogs, podcasts and other helpful emerging market investing resources. The top menu includes links to other resources as well as a link to a general EM investing tips / advice feed e.g. links to specific and useful articles for EM investors.

Disclaimer: EmergingMarketSkeptic.Substack.com and EmergingMarketSkeptic.com provides useful information that should not constitute investment advice or a recommendation to invest. Your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content. Seek a duly licensed professional for any investment advice. I may have positions in the investments covered. This is not a recommendation to buy or sell any investment mentioned.

China's Problems That Few People Talk About (And Investor Implications) was also published on our website under the Newsletter category.

Great post. The leasehold structure of the real estate market is something that has been on my one for a while. Lots of get through before then though.

“Expat”

Just call yourself an immigrant fam.