Emerging Market Links + The Week Ahead (October 14, 2024)

Jim Cramer's curse strikes again, HK crash dissected, Beijing sparked retail stock trading frenzy, dollar dropping as global reserve currency, EM stock picks and the week ahead for emerging markets.

Before you get too excited about Chinese or Hong Kong stocks, beware of the inverse Cramer effect or the curse of Jim Cramer:

And just to add…:

Investors need to remember that China and the CCP are not exactly in the position to do anything too radical to fix things without breaking more things or causing more problems or unintended consequences - like adding a retail stock market bubble to the property market one e.g. ‘Cutting leeks’: Beijing sparks a retail stock trading frenzy FT 🗃️.

Finally, as mentioned yesterday, Sunday posts emailed out will cover new fund updates and research from specific funds added to a continuously updated EM Fund Stock Picks & Country Commentaries utilizing that also utilizes Substack’s new autogenerated post table of contents feature. I am also cleaning up emerging market stock indices posts or pages & will improve/expand the monthly China and Korea stock picks posts.

🔬 Emerging Market Stock Pick Tear Sheets

$ = behind a paywall

🇨🇳 CMBI Research China & Hong Kong Stock Picks (September 2024) Partially $

China Hongqiao Group, ANTA Sports Products, Haier Smart Home, EVA Precision Industrial Holdings, Topsports, Binjiang Service Group, JNBY Design, NIO Inc, New Hope Service Holdings, China Pacific Insurance, Haidilao International Holding, Jinmao Property Services, Wingtech Technology, Maxscend Microelectronics, China Life Insurance, Shanghai United Imaging Healthcare, Atour Lifestyle Holdings, Shenzhen Mindray Bio-Medical Electronics, Sany Heavy Equipment International Holdings, Zoomlion Heavy Industry, Guangzhou Automobile Group, Jinxin Fertility Group, Joinn Laboratories China, China Yongda Automobile Services Holding & China MeiDong Auto Holdings

20+ high conviction stock ideas: Li Auto, Geely Automobile, Zoomlion Heavy Industry, Zhejiang Dingli, Bosideng, JNBY, Xtep, Proya Cosmetics, Kweichow Moutai, BeiGene, Shenzhen Mindray Bio-Medical Electronics, China Pacific Insurance (Group), PICC Property and Casualty, Tencent, Alibaba, PDD Holdings, Greentown Service Group, CR Land, FIT Hon Teng (Foxconn Interconnect Technology), Xiaomi, BYD Electronic International, Zhongji Innolight, NAURA Technology Group & Kingdee International Software Group

🌐 EM Fund Stock Picks & Country Commentaries Partially $

This post compliments our EM Fund Stock Picks & Country Commentaries posts (emailed weekly) & all contains stock names/tickers until there is a fund update + fund research for the last 2+ months.

🌐 EM Fund Stock Picks & Country Commentaries (October 13, 2024) Partially $

China's stimulus (or more of the same?), why growth stock investors can't ignore China, foreigner investors still cautious on South Africa, EM local currency bonds, fund Q3 updates start to drop, etc.

📰🔬 Emerging Market Stock Picks / Stock Research

$ = behind a paywall / 🗃️ = Archived article

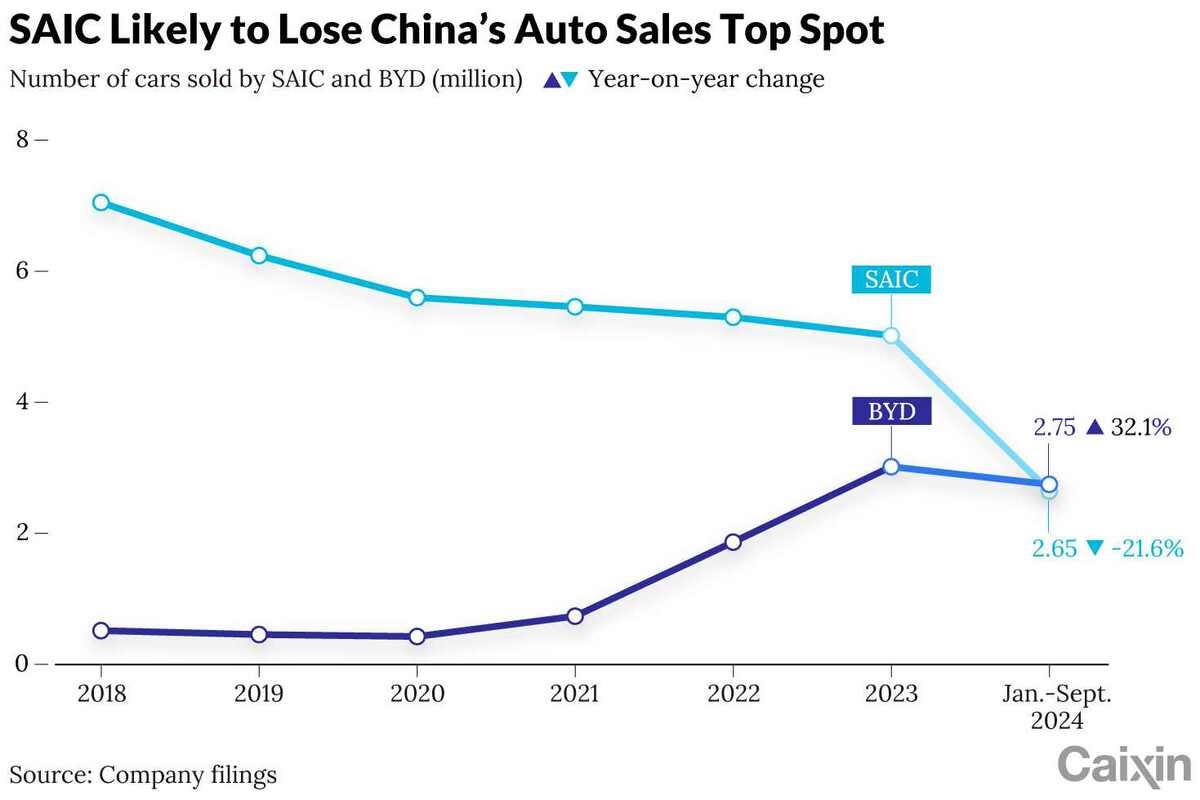

🇨🇳 Chart of the Day: SAIC Likely to Lose Yearly Car Sales Crown to BYD (Caixin) $

State-owned SAIC Motor Corp (SHA: 600104) is likely to be knocked off its perch as China’s biggest auto seller for the full year by electric vehicle (EV) giant BYD Company (HKG: 1211 / SHE: 002594 / OTCMKTS: BYDDY / BYDDF), ending a nearly two-decade run of dominance.

From January to September, SAIC sold about 2.65 million vehicles, down 21.56% year-on-year, according to a stock exchange filing. Of those, 748,027 were new-energy vehicles (NEVs), up 15.28% year-on-year. The NEV category includes battery-electric cars, plug-in hybrids and fuel cell vehicles.

🇨🇳 In leaked reports, Baidu shows it’s in the global robotaxi race (Bamboo Works)

Media reports said the autonomous driving aspirant plans to take its robotaxis global, though it’s likely to stay focused on its home China operations for now

Baidu (NASDAQ: BIDU)’s reported international robotaxi expansion plans look more like strategic narrative to show future potential rather than an immediate priority

The company’s robotaxi operation aims to break even in Wuhan by year-end, with overall profitability for the business projected for 2025

🇨🇳 🇻🇳 🇧🇳 Temu’s entry in Vietnam (Momentum Works)

PDD Holdings (NASDAQ: PDD) [Pinduoduo and Temu]

Temu has launched in Vietnam and Brunei, bringing the ecommerce platform’s number of markets in Southeast Asia to 5.

Many industry stakeholders heard about Temu’s potential entry in Vietnam as early as in July. Back then it was anticipated that the launch would happen in October – and it seems now Temu has made it on time.

That said, the launch version of Temu Vietnam site is rudimentary: it is currently only available in English (not Vietnamese); only credit card payments are accepted (not local wallets); and only two logistics players (Ninja Van and Best Express) are plugged in.

🇨🇳 🌍 Synagistics holds potential to enliven moribund Hong Kong SPAC market (Bamboo Works)

The Southeast Asian e-commerce company backed by Alibaba (NYSE: BABA) is inching closer to completing a backdoor listing using a special purpose acquisition company

Shareholders of a SPAC backed by a former head of Hong Kong’s de facto central bank will vote Oct. 25 on a merger with Singaporean e-commerce firm Synagistics

The deal would mark the first completion of a merger for Hong Kong’s fledgling SPAC market, which has failed to gain traction since its launch at the start of 2022

🇨🇳 Qifu fends off short-seller assault over its earnings record (Bamboo Works)

The online loan facilitator found itself under fire from Grizzly Research [We Believe Qifu Technology, Inc. (NASDAQ: QFIN) is a China Hustle Stock with Outright Fake Financials, Fraudulent Backers, and an Imploding Business], accused of inflating its profits, but the claims failed to dent the company’s share price or deliver a resounding blow to shareholder Zhou Hongyi

The credit services company disputed Grizzly’s claim of overstated profits, saying a discrepancy between its U.S. and Chinese filings was due to differing reporting requirements

Qifu (NASDAQ: QFIN) reported cash flow of 1.96 billion yuan last quarter and is buying back $350 million worth of shares, lending support to the stock price

🇨🇳 Lenovo gains market share in computing race to reap profits from AI (Bamboo Works)

The company boosted its share of the global PC market in the third quarter, even as its sales of other products like servers and storage look set to overtake its PC business

Lenovo Group (HKG: 0992 / FRA: LHL / LHL1 / OTCMKTS: LNVGY / LNVGF) consolidated its place as the world’s leading PC maker in the third quarter, boosting its share of the market to 24% from 22.7% a year earlier, according to IDC

The company’s gross margins trail its rivals as it sacrifices profitability to gain a foothold in the business of providing infrastructure for cloud and data center operators

🇨🇳 ZJK crafts small but sturdy IPO with its focus on nuts-and-bolts (Bamboo Works)

The Shenzhen-based company’s strong Nasdaq debut banked on the star power of its all-star client listing including names like BYD, Nvidia and DJI

ZJK Industrial Co Ltd (NASDAQ: ZJK)’s shares rose as much as 36% in their first week of trade on the Nasdaq, despite its relatively small IPO with only 2% of its shares sold

The maker of fasteners and other components plans to use some of its IPO proceeds to set up a new foundry, possibly in Vietnam

🇨🇳 Akeso Placement - Opportunistic Raise, past Deal Record Has Been Mixed but Relative Size Is Small (Smartkarma) $

Akeso (HKG: 9926 / FRA: 4RY / OTCMKTS: AKESF) is looking to raise around US$200m from its primary placement. Proceeds from the placement will be used for R&D.

Past deals in the name haven’t done well recently but the shares have been doing well and the deal size remains small.

In this note, we talk about the deal dynamics and run the deal through our ECM framework.

🇭🇰 Mandarin Oriental (MAND SP) (Asian Century Stocks) $

World-class luxury hotel group at 76% discount to NAV

Mandarin Oriental (SGX: M04 / FRA: 1C4 / OTCMKTS: MAORF)—US$2.2 billion) five-star hotels are some of the best in the world.

But what many do not know is that Mandarin Oriental is a publicly listed entity. You can get exposure to the brand through its primary listing in London or secondary listings in Singapore or Bermuda. The company is part of the Jardine Matheson Group - an Asia-focused conglomerate with a rich history as a British trading house.

🇭🇰 Hong Kong stocks too cheap to ignore (part 3) (Leahi Capital Substack)

Dah Sing Banking Group (HKG: 2356 / FRA: RY2 / OTCMKTS: DHSBF)

With Hong Kong shares finally receiving some love (benchmark index +39% from the mid-January low) this may be the finale of the ‘Hong Kong stocks too cheap to ignore’ series. With that introduction, let’s look at Dah Sing Banking Group, a small yet solid lender which continues to trade on exceptionally low multiples (0.3x P/TB, 5x P/E, 11% dividend yield) despite a pop from the bottom. Its fair value may be HKD 17 per share, ~140% above the current price. The bank has a strong funding and capital position and is well-regulated. Low multiples protect the shares from downside risk – a perfect asymmetrical opportunity.

🇲🇴 Macau pull for China clients strong, can grow: MGM CEO (GGRAsia)

China economic stimulus policy is “relevant” to Macau, but the city is still “unique” in terms of its appeal, and the penetration rate for the city’s services is still modest on the Chinese mainland, says Bill Hornbuckle (pictured), chief executive and president of casino group MGM Resorts International (NYSE: MGM), the parent of Macau operator MGM China Holdings Ltd (HKG: 2282 / FRA: M04 / OTCMKTS: MCHVF / MCHVY).

He stated in an interview: “I want to remind everybody… the key focus for all of us is premium mass [gambling customers] and the actual penetration rate into Macau – it does about 20-odd million visitors a year – is really folks coming three or four times a year.”

“So it’s like less than 1 percent penetration” in terms of market potential, he added.

Mr Hornbuckle was speaking in a Tuesday interview conducted on the sidelines of the Global Gaming Expo (G2E) casino industry trade show and conference in Las Vegas, Nevada, in the United States.

🇹🇼 Himax Technologies: Navigating The Down Cycle (Seeking Alpha) $ 🗃️

Himax Technologies (NASDAQ: HIMX) [Fabless semiconductor company providing display imaging processing technologies]

🇰🇷 Korea Zinc: Latest Stockholder Record for Proration Risk (Smartkarma) $

If NPS and passive funds each tender half, it could hit 24%, pushing investors to consider both sides. The market’s eyeing a ratio of about MBK 3 to Choi 7.

This tight vote could drag out the event longer than expected, and MBK might scoop up more shares if they miss their minimum target.

MBK will likely go for open market buys against Korea Zinc (KRX: 010130)’s buyback. Consider tendering to MBK Monday and spread trading futures, or push Korea Zinc to raise their buyback offer.

🇰🇷 Korea Zinc Raises Share Buyback and Tender Offer Price to 890,000 Won (Douglas Research Insights) $

Korea Zinc (KRX: 010130) raised the share buyback and tender offer price from 830,000 won to 890,000 won. Korea Zinc's share price closed up by only 0.6% today to 794,000 won.

As a result, the amount of capital involved in this share buyback and tender offer would increase from 2.7 trillion won to 3.2 trillion won.

Despite higher share buyback/tender offer of Korea Zinc by Choi family, we believe that this fight for the control of Korea Zinc is increasingly in favor of MBK/Jang family.

🇰🇷 T'Way Air: Increasing Possibility of an M&A Fight Between Yearimdang and Daemyung Sono Group (Douglas Research Insights) $

In the past several days, there have been an increased speculation in the local media about a potential M&A fight for T'Way Air (KRX: 091810) between [book publisher] Yearimdang Publishing (KOSDAQ: 036000) and Daemyung Sono Group.

The difference in ownership of T'Way Air by Daemyung Sono Group and Yearimdang Group is only 3.2%, which could lead to an intensified management rights dispute.

According to local sources, Daemyung Sono Group has recently contacted several law firms to review plans to potentially conduct a tender offer on T'Way Air.

🇰🇷 Concerns About Transferring Doosan Bobcat Shares Held by Doosan Enerbility to Doosan Robotics (Douglas Research Insights) $

In the process of transferring Doosan Bobcat (KRX: 241560) shares held by Doosan Enerbility (KRX: 034020) to Doosan Robotics (KRX: 454910), there are increasing concerns about negatively impacting minority shareholders of Doosan Enerbility.

This current restructuring structure could potentially benefit the Park family/relatives which is the largest shareholder group of Doosan Corp but could negatively impact minority shareholders of Doosan Enerbility.

On 25 September, Doosan Enerbility announced that 10 October will be the shareholder confirmation date (shareholder register closing date) for the spin-off NEWCO merger agreement with Doosan Robotics.

🇰🇷 Sung Woo IPO Valuation Analysis (Douglas Research Insights) $

Our base case valuation of [cathode for HMC hydrogen fuel cell electric vehicle batteries] Sung Woo is target price of 27,981 won per share, which is within the IPO price range of 25,000 won to 29,000 won per share.

Given the lack of upside relative to the IPO price range, we have a Negative view of this IPO.

Our base case valuation of 27,981 won per share is based on a P/E of 16.9x based on net profit of 24.9 billion won in FY23.

🇰🇷 Orum Therapeutics IPO Preview (Douglas Research Insights) $

Orum Therapeutics is getting ready to complete its IPO in KOSDAQ in November 2024. The IPO price range is from 30,000 won to 36,000 won.

The expected market cap after IPO is from 648 billion won to 778 billion won. The book building for the institutional investors starts on 24 October.

Orum Therapeutics' main pipelines include 'ORM-6151', a new drug candidate for acute myeloid leukemia, 'ORM-5029', a HER2-targeting breast cancer treatment candidate, and 'ORM-1023', a small cell carcinoma tumor candidate.

🇯🇵 Tokyo Metro IPO Valuation Analysis (Douglas Research Insights) $

Tokyo Metro set the IPO price range at 1,100 to 1,200 Yen per share. At the top end of the range, Tokyo Metro would raise 349 billion yen ($2.35 billion).

Our base case valuation of Tokyo Metro is implied target price of 1,178 yen per share. This is within the top end of the IPO price range (1,200 yen).

Given the lack of upside relative to the IPO price range, we have a Negative view of this IPO.

🇲🇾 Autocount Dotcom Berhad (KLSE:ADB) (Hurdle Rate)

Malaysian Accounting Software

With the introduction of access to the Malaysian Bursa on Interactive Brokers I was pleased to be able to look further into Autocount Dotcom Bhd (KLSE: ADB) in preparation. Autocount was founded in 1996 and has the largest and fastest growing accounting software in Malaysia. The founders were existing executive directors Choo Chin Peng (CCP) and Choo Yan Tiee (CYT) along with another who has moved on. For background on these two I recommend reading this article [Cover Story; An unlikely duo who found success].

🇵🇭 Puregold Price Club: A Defensive Retailer Amidst The Rising Threat Of Hard Discount Stores (Seeking Alpha) $ 🗃️

Puregold Price Club (PSE: PGOLD / OTCMKTS: PGCMF / PRGLY)

🇸🇬 DBS Group Could Continue To Deliver Returns, But Safety Margin Is Thin (Seeking Alpha) $ 🗃️

🇸🇬 Sea: There's Still Steam Left In This Rally, But Watch Some Key Risks (Seeking Alpha) $ 🗃️

Sea Limited (NYSE: SE)

🇸🇬 Real Estate Series Part I: OUE REIT (Modern Value Investing)

Singapore Trophy Assets at a 45% NAV Discount

Summary

OUE Real Estate Investment Trust (SGX: TS0U / OTCMKTS: OUECF) owns a mixed asset portfolio in the finest locations of Singapore

Conservative financial structure with a loan-to-value ratio of 38%

6% dividend yield for 2024 with significant mid-term upside

I’m laying out what it takes for a 100% total return over 3-4 years

🇸🇬 These 4 Singapore Stocks’ Share Prices Are at 52-Week Highs: Can They Sustain Their Momentum? (The Smart Investor)

Here are four Singapore stocks that recently touched their 52-week highs, and we review their business to determine if they can sustain this momentum.

Civmec Ltd (SGX: P9D / ASX: CVL / FRA: 1CV) is an Australian multi-disciplinary construction and engineering services firm that serves the energy, resources, infrastructure, and marine & defence sectors.

Fraser and Neave (SGX: F99 / FRA: FNV2 / OTCMKTS: FNEVF), or F&N, is a food and beverage (F&B) giant that sells soft drinks, beer, dairies, juices, and ice cream.

SATS Ltd (SGX: S58 / FRA: W1J / OTCMKTS: SPASF) is an aviation food services provider and also provides ground handling and cargo services.

Hongkong Land Holdings (SGX: H78 / LON: HKLJ / FRA: HLH / OTCMKTS: HKHGF / HNGKY), or HKL, owns and manages more than 850,000 square metres of prime office and luxury retail properties in Hong Kong, Singapore, Beijing, and Jakarta.

🇸🇬 5 Singapore Stocks Providing a Tantalising Mix of Growth and Higher Dividends (The Smart Investor)

Here are five Singapore stocks that promise attractive growth along with higher dividends.

Here are five choice stocks that not only display steady growth but also paid out higher dividends.

CapitaLand Integrated Commercial Trust (SGX: C38U / OTCMKTS: CPAMF), or CICT, is a retail and commercial REIT with a portfolio of 21 properties in Singapore, two in Frankfurt, and three in Australia.

Sembcorp Industries (SGX: U96 / FRA: SBOA / OTCMKTS: SCRPF), or SCI, is an energy and urban solutions provider.

iFAST Corporation Limited (SGX: AIY / FRA: 1O3 / OTCMKTS: IFSTF) is a financial technology company operating an online platform that allows customers to buy and sell unit trusts, equities, and bonds.

Tiong Woon Corporation Holding Ltd (SGX: BQM) is an integrated heavy lift specialist and service provider supporting the oil and gas, petrochemical, infrastructure, and construction sectors.

Genting Singapore (SGX: G13 / FRA: 36T / OTCMKTS: GIGNF / GIGNY) owns and operates Resorts World Sentosa (RWS), an integrated resort (IR) that boasts a casino, six hotels with around 1,600 hotel rooms, a Universal Studios Singapore theme park, a SEA aquarium, and a wide selection of dining, retail, and entertainment options.

🇸🇬 Trouble Brewing for Mapletree Logistics Trust: Can the Logistics REIT See its DPU Recover? (The Smart Investor)

Many Singapore REITs saw their operating and finance expenses surge, causing their distributable income to fall and their distributions to decline.

Mapletree Logistics Trust (SGX: M44U / OTCMKTS: MAPGF), or MLT, is no exception.

The industrial REIT saw its distribution per unit (DPU) get badly hit in its latest quarter.

Can MLT turn the situation around the start posting higher DPU? Let’s find out.

A stellar track record

A confluence of negative events

Active capital recycling

Some respite in the near term

Get Smart: Patience is the key

🇸🇬 4 Singapore Stocks Paying a Dividend Yield That Exceeds Your CPF Special Account Interest Rate (The Smart Investor)

Here are four stocks that provide a higher dividend yield than the CPF Special Account that you can consider for your buy watchlist.

Far East Hospitality Trust (SGX: Q5T), or FEHT, is a hospitality trust with a portfolio of 12 properties totalling 3,015 hotel rooms and serviced residence units.

CapitaLand Ascendas REIT (SGX: A17U / OTCMKTS: ACDSF), or CLAR, is an industrial REIT that owns 229 properties across Singapore, the US, Australia, and Europe/the UK.

Aztech Global (SGX: 8AZ) is a designer and manufacturer of Internet of Things (IoT) devices and data communication products.

Food Empire (SGX: F03) is a food and beverage (F&B) manufacturing and distribution group with a portfolio comprising instant beverages, snack foods, and food ingredients.

🇸🇬 DBS backs Chinese firms expanding into Asean (The Asset) 🗃️

DBS Group (SGX: D05 / FRA: DEVL / DEV / OTCMKTS: DBSDY / DBSDF) and the China Council for the Promotion of International Trade (CCPIT), one of China’s largest trade bodies, have signed a memorandum of understanding (MOU) to boost foreign investment and trade between China, Singapore and the Asean region.

The partners aim to help Chinese enterprises internationalize their businesses, strengthen supply chains in the region, enable job creation and accelerate sustainable development.

DBS’ regional clients will be able to tap CCPIT’s network to expand into China, while Chinese companies can take advantage of the bank’s extensive presence in the region to grow their businesses.

🇹🇭 Five groups seek to open digital banks in Thailand (The Asset) 🗃️

Central bank will only award three licences by mid-2025 as applications close

The applicants include: a collaboration between Siam Commercial Bank [SCB X PCL (BKK: SCB / SCB-F / FRA: OU80 / OU8)], and China-based WeChat as well as South Korea-based Kakao Bank; a partnership between Thai conglomerate Charoen Pokphand Group-backed Ascend Money and China-based Ant Group; a joint venture made up of Singapore-based Sea Limited (NYSE: SE), the operator of e-commerce giant Shoppee, along with Bangkok Bank (BKK: BBL / OTCMKTS: BKKLY), Thailand Post, Sahapat Group, and VGI; a joint venture between Gulf Energy Development (BKK: GULF / SGX: TGED), telco giant Advanced Info Services (BKK: ADVANC / SGX: TADD) and Krungthai Bank Plc; and Lightnet, a collaboration between fintech firm Lighthub Asset and Hong Kong-based digital banking pioneer WeLab.

🇮🇳 The Beat Ideas: GPIL- Low Cost Mining with Upcoming Steel Plant (Smartkarma) $

Godawari Power and Ispat Limited (NSE: GPIL / BOM: 532734) is fully integrated steel manufacturer with a diverse portfolio encompassing iron ore mining, pellet production, sponge iron, steel billets, ferroalloys, and power generation.

Net Cash Balance Sheet, Mining Expansion, and upcoming Integrated Steel Plant provide huge potential for the captive consumption.

Execution of the capex plan within the stipulated timeframe is the key risk.

🇮🇳 Ola Electric: Price-Cut Gamble, Social Media Blunders, Slipping Sales – Is the Spark Fading? (Smartkarma) $

Ola Electric Mobility Ltd (NSE: OLAELEC / BOM: 544225)'s aggressive price cuts on its S1 scooter aim to fend off competition and boost sales but risk alienating existing customers and damaging brand perception.

Ola Electric’s mishandling of online criticism—capped by its CEO’s heated spat with a well-known comedian—has tarnished the brand’s image.

With market share and stock prices dropping, concerns loom over how the company will fare after lock-up expiry in November/February and whether it will qualify for global index inclusion.

🇮🇳 The Beat Ideas: HIL Limited - Turnaround Play in Building Material (Smartkarma) $

Change in [comprehensive building materials and solutions] HIL Ltd (NSE: HIL / BOM: 509675) started after the appointment of professional CEO Mr. Akshat Seth.

HIL is turning around its acquisition of Parador and Topline, which were Loss making. The company was not performing due to lower demand in US, EU etc.

Aiming for 14-16% Revenue growth and 2-3% EBITDA Margin improvement due to distribution growth, Parador Turnaround and high demand in real estate segment.

🇮🇳 The Beat Ideas: Vishnu Chemicals- Niche Business with High Growth Levers (Smartkarma) $

Vishnu Chemicals (NSE: VISHNU / BOM: 516072) is now backward integrated with the soda ash, CO2 Gas plant and ore requirement to overcome the challenge of raw material price volatility.

Company operated in niche & specialty chemical segment and will launch detailed capex plan in Q2 for forward integration.

Management aims to consolidate EBITDA margins around 17.5%-18% by year-end, with a target of achieving consistent margins at 20% over the next 2-3 years.

🇮🇳 Hyundai Motor India IPO: Upsized Valuation Driven by Strong Investor Interest (Smartkarma) $

Hyundai Motor India (1342Z IN)’s IPO, launching next week, is expected to be priced between Rs1,865 and Rs1,960, valuing the company at USD 18-19 billion.

At this valuation, Hyundai’s India unit will account for over 40% of its parent company's market cap, potentially unlocking significant value for Hyundai Motor (KRX: 005380 / FRA: HYU / OTCMKTS: HYMTF).

Despite a weak growth in India's passenger vehicle sales ytd, investor interest in the IPO is reportedly strong thanks to India's booming equity market and robust fund inflows.

🇮🇳 Hyundai Motor India Sets IPO Price Range (Douglas Research Insights) $

Hyundai Motor India (1342Z IN) has set an IPO price range of 1,865 to 1,960 rupees per share, aiming for a valuation as high as US$19 billion.

Hyundai Motor (KRX: 005380 / FRA: HYU / OTCMKTS: HYMTF) is selling a 17.5% stake in Hyundai Motor India in this public offering. Hyundai Motor India IPO is scheduled to trade starting 22 October.

Our updated base case valuation of Hyundai Motor India is market cap of US$19.7 billion based on P/E of 25.9x our estimated net profit of 64.1 billion INR.

🇮🇳 Hyundai Motor India IPO: Analysis of Latest Financials Signal Challenging Year Ahead (Smartkarma) $

After 3 years of strong revenue and profits growth, Hyundai Motor India is likely to face a challenging year ahead based on the analysis of 1QFY2025 financials provided in RHP.

Hyundai Motor India (1342Z IN)'s strong exports growth in FY2025 will not offset the weakness in domestic sales. This could result in low single-digit revenue growth for the year.

Increased royalty costs starting in FY2025, coupled with impact of lower cash reserves after special dividend paid out to parent will likely compress profit margins compared to the previous year.

🇮🇳 Swiggy Pre-IPO - The Negtives - Neither Food nor Quick Commerce Was the Largest Revenue Driver (Smartkarma) $

Swiggy is planning to raise around US$1.25bn through its upcoming India IPO.

Swiggy Limited (Swiggy) is a business to commerce (B2C) marketplace company offering users a platform for ordering grocery and household items (Instamart) and food delivery, through its on-demand delivery network.

In this note, we talk about the not-so-positive aspects of the deal.

🇮🇳 Quiddity Leaderboard BSE/SENSEX Dec 24: Some Changes to Expectations + Zomato Question Mark (Smartkarma) $

In this insight, we take a look at the Potential ADDs/DELs for the BSE SENSEX, 100, and 200 indices in the December 2024 index rebal event.

We expect six ADDs/DELs for BSE 100 and six ADDs/DELs for BSE 200.

Zomato Limited (NSE: ZOMATO / BSE: ZOMATO) is one of the six BSE 100 expected DELs but its fate will depend on when its expected F&O list inclusion takes place and the index provider's discretionary choices.

If Zomato gets deleted from BSE 100, there could be an index outflow of US$144mn. This is the largest flow name among our expected ADDs and DELs in this insight.

🇮🇳 Shriram Pistons and Rings Ltd- Forensic Analysis (Smartkarma) $

Shriram Pistons & Rings Ltd (NSE: SHRIPISTON) is into the business of manufacturing auto components including pistons, piston pins and rings, engine valves, electric motors etc.

On an overall scheme of things, balance sheet and forensics look good and healthy.

However, one must pay attention to goodwill and related assumptions; one of the recent acquisitions has turned loss making.

🇰🇿 Deconstructing Culper's Short Report on Kaspi.kz (The Very Good Value Blog)

KASPI (NASDAQ: KSPI / LON: 80TE / FRA: KKS)

30 pages of exaggerations, strenuous links and false allegations, demonstrating a severe misunderstanding of Russian sanctions - with a couple of valid points sprinkled in.

I wrote an in-depth analysis of Kaspi.kz - the Kazakh fintech and super-app - back in April, and subsequently made it the largest allocation in the VGV Portfolio, at 40%.

On September 19th, Culper Research, an ‘activist short-seller’ (I find journalist short-seller to be a more appropriate description, but alas), published a short report on Kaspi, which sent the stock down from $120 to the mid-90s (it closed most recently at $103 as I write this). There were quite a few accusations, but the gist of it was basically that despite claiming otherwise, Kaspi has many links to Russia and a massive amount of Russian deposits; and also that the CEO and Chairman are a pair of dodgy self-dealers. Culper concluded there is a significant risk of Kaspi being the subject of secondary sanctions, and that delisting from the NASDAQ may be on the cards. Scary stuff.

Kaspi’s initial response was cookie-cutter

🇦🇪 Wynn says to have 15yr casino licence for Ras Al Khaimah (GGRAsia)

Wynn Resorts Ltd (NASDAQ: WYNN) will have an exclusive, renewable 15-year casino licence for Ras Al Khaimah in the United Arab Emirates (UAE), and could generate a minimum of US$1.33 billion annually in gross gaming revenue (GGR), according to an investor update issued on Tuesday by the company.

The local gaming licence for the Wynn Al Marjan Island complex (pictured in an artist’s rendering) was confirmed in a Friday statement from the group. Wynn Resorts is the parent of Macau casino operator Wynn Macau Ltd (HKG: 1128 / FRA: 8WY / OTCMKTS: WYNMY / WYNMF).

🇿🇦 Varun Beverages gains green light for acquisition of The Beverage Company (IOL)

The Competition Commission has approved the acquisition of The Beverage Company, commonly known as Bevco, by Varun Beverages (NSE: VBL / BOM: 540180), a significant player in the global beverage market.

Varun Beverages, incorporated in India, operates a variety of beverages, predominantly carbonated soft drinks under familiar trademarks owned by PepsiCo. Currently, Varun Beverages does not have any active operations in SA, with a dormant subsidiary—Varun Beverages South Africa—having never conducted operations since its establishment.

Bevco, on the other hand, is a well-established SA company based in Johannesburg, recognised for its production of carbonated soft drinks, mixers, energy drinks, water, and serving as a registered bottler for Pepsi in SA. This merger positions Varun Beverages to potentially enhance and expand Bevco’s product offerings and distribution channels in the competitive South African market.

🇿🇦 Sibanye-Stillwater faces legal setback as court rules on $1.2bn Appian dispute (IOL)

PRECIOUS metal producer Sibanye Stillwater Ltd (NYSE: SBSW) has encountered a legal setback in its ongoing $1.2 billion (R15 billion) dispute with Appian Capital Advisory LLP following a ruling delivered in the High Court of England and Wales.

The proceedings, which began in June 2024, focused on the termination of share purchase agreements (SPAs) between Sibanye-Stillwater and Appian, associated with the acquisition of the Santa Rita and Serrote mines in Brazil.

The root of this dispute lies in a geotechnical event that occurred at the Santa Rita nickel operation in Brazil in November 2021, which Sibanye-Stillwater argued was significant enough to adversely affect the mine’s business and finances.

🇿🇦 Are the traditional South African insurers about to disrupt the retail banking market? (IOL)

Despite these advantages, however, most insurance products are still sold as opposed to bought and require intensive face to face advice, favouring the traditional life insurers who are adept at managing large forces of tied and independent financial advisers. These intermediaries though do lead to high distribution costs, which are largely passed onto clients via higher premiums.

However, this is changing, most notably in the funeral insurance market, where banks are finding that cheaper (sometimes up to 30%+) direct branch and digital sales are proving effective. The result now, according to Swiss Re, is that Capitec Bank (JSE: CPI / OTCMKTS: CKHGY / CKHGF) has over 36% market share of funeral sales (measured by sum assured).

Discovery Bank [Discovery Ltd (JSE: DSY / FRA: D3H / OTCMKTS: DCYHF)]: Disrupting the mortgage market with innovative pricing

Old Mutual Ltd (JSE: OMU / LON: OMU / FRA: 2KS / OTCMKTS: ODMUF) and Sanlam (JSE: SLM / FRA: LA6A / FRA: LA6S / OTCMKTS: SLLDY)’s bold banking moves

🇿🇦 Mondi expands European footprint with €634 million acquisition of Schumacher Packaging assets (IOL)

Mondi (LON: MNDI / JSE: MNP / OTCMKTS: MONDY / MONDF)’s footprint in Europe will almost double with the announcement yesterday of the acquisition of packaging assets of Schumacher Packaging in the region, for €634 million (R12.3 billion), to be financed from Mondi's existing facilities.

Mondi said in a statement yesterday the deal with the family-owned Schumacher would strengthen its corrugated converting footprint in Europe with “highly complementary assets”, increasing capacity by over 1 billion square metres.

🇧🇼 Chobe Holdings Limited (BSE: CHOBE) Part 2 (Possible Value)

See: Chobe Holdings Limited (BSE: CHOBE) Part 1 (Possible Value)

The steps I took to obtain scuttlebutt on Chobe Holdings Limited (BSE: CHOBE)’s yielded some valuable information. There were two main takeaways. First, the luxury travel and safari market in Botswana is thriving. Second, all three subsections apply to and bode well for Chobe’s. It has lodges/safaris/camps in the premier locations in Botswana. It can’t help but benefit from a restricted supply of wealthy travelers who mostly don’t care about price.

There was a downside. I didn’t find what is at the core of Chobe’s robust financial performance. While the subsections above apply to it, they’re also beneficial to its competitors.

🇬🇷 The Curious Case of Karelia (Invariant)

For those familiar with the tobacco landscape, it is no secret the industry’s vilification and ESG-driven divestments have fostered considerable aversion. Karelia Tobacco Company Inc (ASE: KARE) is only a fraction of the size of the tobacco majors. While it could be argued that the company has fewer resources in absolute terms, its track record suggests no issues navigating the markets it operates in. But, its small size, alongside its Greek listing, certainly further restricts access and interest. Further, the name is stupendously illiquid. Daily volume is frequently only 10-20 shares. On occasion, 250 or so will trade hands. Often, it’s as low as 0-5.

Karelia has 27.6 million shares outstanding, providing a market capitalization of €943 million. Trailing twelve-month net earnings places the equity at just over 9x. As of Q2’24, the company sported almost zero debt and held net cash, short-term investments, and securities of €617 million, representing roughly 65% of market capitalization. If that isn’t tantalizing enough, know there is insider ownership of gigantic proportions.

🇵🇱 Resultados Spyrosoft Q2 y H1-2024 (Gekko Capital)

[In Spanish - use a browser translator]

This week Spyrosoft SA (WSE: SPR / FRA: 2NP) published its Q2 and H1 2024 results. We will analyze these results to see how the company continues to navigate in this difficult environment of the IT sector where the end of the tunnel is getting closer but we still don't see the light clearly.

As for the different verticals, we see that Automotive continues to clearly lead revenue from Spysoft with 27% of income, followed by other verticals such as Media & Entertainment, Financial Services or Geospatial with 11% each.

As conclusion, the results are still not wonderful, with little growth and depressed margins, it is time to continue waiting for the IT sector to recover. It is true that with the drop in interest rates, that return in demand is getting closer, we should see it in 2025 unless a strong recession comes, which does not seem very likely either. As positive points, the reduction of the bench, the adjustments in costs that have made the EBITDA above 10%, and a promising Q3 with the first income of the contract with the BBC and the consolidation of Codibly. We remain confident in Spysoft

🇷🇴 🇧🇬 🇲🇩 Moldova’s wineries shift away from Russian gas (FT) $ 🗃️

Vineyard founded by Joseph Stalin joins country’s westward pivot and green transition

Purcari Wineries (BSE: ROWINE), a Moldovan brand that has a strong presence on western markets after turning its back on Russia, is also going green.

“Fool me once, shame on thee, fool me twice, shame on me,” said Tofan. The Russian bans initially put Purcari “on our knees” but eventually proved “a blessing in disguise” as it accelerated the westward pivot.

🌎 MercadoLibre: The Ultimate 'GARP' Opportunity (Seeking Alpha) $ 🗃️

MercadoLibre (NASDAQ: MELI)

🌎 MercadoLibre: Fintech Operation In Mexico Promises (Seeking Alpha) $ 🗃️

🌎 MercadoLibre: Back To Its Margin Expansion And Hyper Growth Path (Rating Upgrade) (Seeking Alpha) $ 🗃️

🌎 The Most Sleep Well Investment of Latin America (Sleep Well Investments) $

If anti-fragility is a moat, this Latin America Tech Titan has plenty of it.

Since its IPO, it has grown

revenue at 43% CAGR

free cash flow per share at 45% CAGR, and

the stock has risen by 33% CAGR.

Impressively, business can triple in size in the middle term, yet shares are available at the cheapest level!

🌎 🇰🇾 Patria Investments: The Alternatives King Of Latin America (Seeking Alpha) $ 🗃️

Patria Investments Limited (NASDAQ: PAX) [Private market investment firm focused on investing in Latin America]

🇧🇲 Ocean Wilsons (OCN.LN) - Deep Value “Sum of the parts” Special Situation with a Catalyst (Memyselfandi007’s Substack)

Elevator pitch:

Ocean Wilsons (LON: OCN), a UK listed, Bermuda domicile HoldCo which owns a 56% stake in a listed Brazilian Port/Maritime company called Wilson Sons Holdings Brasil SA (BVMF: PORT3) and an investment portfolio, is trading a a deep discount (-48%) to its SOTP value. Now however it seems very likely that the Brazilian Asset will be sold by year end 2024, which could potentially trigger a re-rating of the stock on top of any premium paid in the sale.

🇧🇷 Cosan Q2: This IPO Can Unlock Value (Seeking Alpha) $ 🗃️

🇧🇷 Nu Holdings - a blueprint for Fintech Success (Value Punks)

But what about valuation?

In October 2022, we published our analysis [Deep Dive: NU Holdings (NU US)] on Nu Holdings Ltd (NYSE: NU) when its stock was trading at just $4 per share. At that time, it was flying under the radar, with little to no discussion about it on fintwit. Fast forward to today, and the stock has surged to $15 per share, capturing the attention of the broader investment community. Now, it seems like everyone on fintwit has something to say about Nu Holdings!

Several key lessons emerge from Nu Bank's journey, applicable both to its current trajectory and other similar institutions.

🇧🇷 Ambev: A Quintessential Value Stock With Low Multiples And Strong Financials (Seeking Alpha) $ 🗃️

🇲🇽 PINFRA: Stable High Margin Business Growing With Mexico, Trading At Attractive Yields (Seeking Alpha) $ 🗃️

Promotora y Operadora de Infraestructura SAB de CV (BMV: PINFRA / FRA: AKY / OTCMKTS: PYOIF) [Construction, operation, maintenance, financing & promotion of toll roads & port projects + production of asphalt mixes]

🇲🇽 GCC: Operations Valued At Attractive Average Yield, And Company Can Grow During Slumps (Seeking Alpha) $ 🗃️

GCC SAB de CV (BMV: GCC / FRA: AK4 / OTCMKTS: GCWOF) [Gray Portland cement, ready-mix concrete, aggregates, coal & construction-related services]

🇲🇽 2 Quality Mexican food companies. Gruma vs Herdez (Bos Invest Substack)

The Mexican stock exchange has quality companies with good exposure to the US. They benefit from favorable demographics & have reasonable valuations.

Unfortunately, I found some less appealing companies as well. Those stocks I will cover briefly. Focus will be on Gruma & Herdez. Two strong food companies with better growth prospects than their developed market peers & lower valuations.

Grupo Gigante SAB de CV (BMV: GIGANTE / OTCMKTS: GPGNF) is a retail & restaurant company. With retail being the largest segment with 73% of revenue. Important brands are Office Depot & RadioShack de Mexico.

Hoteles City Express SAB de CV (BMV: HCITY) is considered the leading and fastest-growing limited-service hotel chain in Mexico in terms of number of hotels, number of rooms, geographic presence, market share and revenues.

Grupo Hotelero Santa Fe SAB de CV (BMV: HOTEL) is an owner and operator of 26 hotel properties.

Desarrolladora Homex SAB de CV (BMV: HOMEX / OTCMKTS: DHHXF): - Mexican construction company that is struggling to stay afloat.

Gruma SAB de CV (BMV: GRUMAB / FRA: 3G3B / OTCMKTS: GMKKY / GPAGF) is the world leader in corn flour & tortillas. With the majority of sales & earnings coming out of the USA.

Grupo Herdez SAB de CV (BMV: HERDEZ / OTCMKTS: GUZOF) has collaborations with famous international food companies like McCormick, Hormel & Barilla… Herdez was covered in March by Alluvial Capital.

📰🔬 Further Suggested Reading

$ = behind a paywall / 🗃️ = Archived article

🇨🇳 ‘Cutting leeks’: Beijing sparks a retail stock trading frenzy (FT) $ 🗃️

Small investors have piled into Chinese equity markets but many have already been burnt by wild price swings

🇨🇳 China's Tech Sector - The Pendulum Swings Back (Investing in China)

From crackdown to collaboration—how government support for Chinese tech giants could unlock new growth and investment opportunities

I’m going to briefly review the increased regulations on Chinese tech companies, often referred to as the “tech crackdown.” While I don’t particularly like the term, it has become widely used, so let’s go with it for now.

Next week, I’ll be writing another article where I’ll elaborate further on recent developments with Chinese tech companies and why I believe even more government support could be in the pipeline. So, stay tuned for more details.

🇭🇰 Hong Kong Crashes As China's Stimulus Frenzy Ends With A Bang (Zerohedge) 🗃️

There is some good news and some bad news for China bulls this morning (local time).

First the good news: since mainland China (aka A-shares) were closed for the past week, mainland Indexes such as the Shanghai Shenzhen CSI 300 are up - just barely - because after opening up almost 11% to catch up with the frenzied rally in offshore markets and ETFs, the index has erased almost all gains since it closed for trading on Sept 30.

... and it means that with the market having called Beijing's bluff, Xi has two options:

Do another half-assed attempt to stimulate the economy with the very limited measures already unveiled, which he knows - and more importantly the market knows - will achieve nothing, and spark another market crash and economic meltdown, or

Do what Goldman trader Borislav Vladimirov laid out yesterday, when he said that China Must Do QE Now, "Or It Will End Up In A Bigger Hole In 12 Months."

🇭🇰 Biggest Hong Kong Crash Since 2008 On Record Volumes: What You Need To Know (Zerohedge) 🗃️

Yesterday when commenting on Goldman's recent upgrade of China's market to Overweight, only after a furious 30% rally had already taken place, we said this suggested that the "move in China has peaked and it's all downhill from here, which incidentally none other than Goldman's trading desk already predicted! Indeed, as we reported this weekend, while Goldman's sellside desk was finally set to recommend China, the bank's much more actionable FICC/S&T desk was already warning that the move in China is over unless Beijing does QE immediately, or else China "will end up in a bigger hole in 12 months." And just a few hours later, that's precisely what happened on Tuesday morning when China A-shares reopened from a week-long holiday and tried to catch up to the meltup only to see their gains slashed. Meanwhile, Hong Kong markets which were open the entire time, and which soared as much as 30% since the Beijing Bazooka was unveiled on Sept 26, cratered the most since the Lehman bankruptcy!

For those who missed it, here is a full rundown of everything that happened in China overnight courtesy of Goldman's trading desk:

🇲🇴 Macau daily GGR US$135mln Oct 1-6, best since 2019: JPM (GGRAsia)

The daily run-rate of Macau’s casino gross gaming revenue (GGR) for October 1 to October 6 – all within China’s seven-day National Day holiday – was estimated at just above MOP1.08 billion (US$135.4 million), the highest level in five years since the comparable October Golden Week holiday in 2019. So suggested JP Morgan Securities (Asia Pacific) Ltd in a Monday memo, citing its channel checks.

🇧🇷 Brazil Municipal Elections - October 2024 (Latin America Risk Report)

There were over 5,000 municipal elections in Brazil this past weekend. In attempting to make any sweeping statements about the results, there will be plenty of exceptions and outliers. With that said, here is an attempt at big picture takeaways from this weekend's election without getting into the individual races.

Candidates who identified with centrist or centrão parties were successful, with centrist referring to where politicians and parties sit on a left-right political spectrum and centrão referring to the clientelistic parties and politicians who will work with anyone across the political spectrum as long as they get a cut of the pie. Either way, the parties that did best in this election identify as one or both of those terms, with the PSD and MDB leading the way.

Given those results, you can take this one of two ways:

Brazilian politics is moving away from the polarization that has defined it in recent years and moving towards a more pragmatic center.

Local politics = local issues, but the polarization will be alive and strong when national elections are next held.

🇧🇪 🇨🇩 🌐 Radium – the rare metal worth 120,000x the price of gold (Undervalued Shares)

It's radium that would set you back US 10,000,000 for a single GRAM. Compare that to gold being worth just USD 85 per gram.

Radium occurs naturally, but there is simply very little of it.

Fancy getting yourself a bit of the valuable radioactive material?

Well, the world of Big Pharma is currently on a quest to find as much as it can get hold of.

Radium is needed to produce "the world's rarest drug", and it could single-handedly transform the treatment of cancer.

Specifically, what they were keen to hide was the fact that Shinkolobwe offered a grade of uranium unlike anywhere else in the world. While Uranium is also found in decent quantities in Canada, Australia, Kazakhstan, and the US, only the Congo's Shinkolobwe had uranium ore with 60% purity grade – far more than the attractive 0.3% purity grade found elsewhere. In Shinkolobwe, even the "waste product" still had 20% purity.

The US dollar, still the #1 reserve currency held by central banks, keeps losing share in bits and pieces ever so slowly against a mix of other reserve currencies as central banks diversify their holdings of dollar-denominated assets to assets denominated in other currencies. And they’re also adding to their holdings of gold.

The share of USD-denominated foreign exchange reserves – assets that central banks other than the Fed hold that are denominated in USD – ticked down to 58.2% of total exchange reserves in Q2, the lowest share since 1995, according to the IMF’s new COFER data.

Over the past 10 years, the dollar’s share has dropped by about 8 percentage points, from 66% in 2015 to 58.2% in 2024 so far. If this pace continues, the dollar’s share will kiss 50% in 10 years.

📅 Earnings Calendar

Note: Investing.com has a full calendar for most global stock exchanges BUT you may need an Investing.com account, then hit “Filter,” and select the countries you wish to see company earnings from. Otherwise, purple (below) are upcoming earnings for US listed international stocks (Finviz.com):

📅 Economic Calendar

Click here for the full weekly calendar from Investing.com containing frontier and emerging market economic events or releases (my filter excludes USA, Canada, EU, Australia & NZ).

🗳️ Election Calendar

Frontier and emerging market highlights (from IFES’s Election Guide calendar):

Georgia Georgian Parliament Oct 26, 2024 (d) Confirmed Oct 31, 2020

Uzbekistan Uzbekistani Legislative Chamber Oct 27, 2024 (d) Confirmed Dec 22, 2019

Uruguay Referendum Oct 27, 2024 (t) Confirmed Mar 7, 2022

Uruguay Uruguayan Presidency Oct 27, 2024 (d) Confirmed Nov 24, 2019

Uruguay Uruguayan Chamber of Representatives Oct 27, 2024 (d) Confirmed Oct 27, 2019

Uruguay Uruguayan Chamber of Senators Oct 27, 2024 (d) Confirmed Oct 27, 2019

Bulgaria Bulgarian National Assembly Oct 27, 2024 (d) Confirmed Jun 9, 2024

Sri Lanka Sri Lankan Parliament Nov 14, 2024 (t) Confirmed Aug 5, 2020

Romania Romanian Presidency Nov 24, 2024 (d) Confirmed Nov 24, 2019

Namibia Namibian Presidency Nov 27, 2024 (d) Confirmed Nov 27, 2019

Namibia Namibian National Assembly Nov 27, 2024 (d) Confirmed Nov 27, 2019

Romania Romanian Senate Dec 1, 2024 (t) Confirmed Dec 6, 2020

Romania Romanian Chamber of Deputies Dec 1, 2024 (t) Confirmed Dec 6, 2020

Ghana Ghanaian Presidency Dec 7, 2024 (t) Confirmed Dec 7, 2020

Ghana Ghanaian Parliament Dec 7, 2024 (t) Confirmed Dec 7, 2020

Thailand Referendum Dec 31, 2024 (t) Date not confirmed Aug 7, 2016

Croatia Croatian Presidency Dec 31, 2024 (t) Date not confirmed Jan 5, 2020

📅 Emerging Market IPO Calendar/Pipeline

Frontier and emerging market highlights from IPOScoop.com and Investing.com (NOTE: For the latter, you need to go to Filter and “Select All” countries to see IPOs on non-USA exchanges):

Rising Dragon Acquisition Corp. RDACU Lucid Capital Markets, 5.0M Shares, $10.00-10.00, $50.0 mil, 10/11/2024 Priced

We are a newly organized blank check company. (Incorporated in the Cayman Islands)

We intend to seek to acquire small cap businesses exhibiting substantial potential in emerging markets driven by innovative technologies or novel business models. We believe these industries are attractive for a number of reasons, including: they represent attractive markets, which are characterized by a high level of innovation and they include a large number of emerging high growth companies that have the right size as potential targets.

We believe our operating experience and industry contacts place us in a position to optimize our chances of identifying high value targets in these areas. Our target of small cap companies will be based on the concept of value investing and therefore focused on quality businesses with specific and time-based catalysts. We will remain opportunistic at considering opportunities throughout the defined targeted space however, our primary focus will be on small cap companies with one or more of the following characteristics:

Target Size: We intend to acquire one or more companies with significant revenue growth, with values between $500 million ($500,000,000) and $2 billion ($2,000,000,000).

(Note: Rising Dragon Acquisition Corp. priced its SPAC IPO in sync with the terms in the prospectus – 5.0 million units at $10.00 each – to raise $50.0 million on Thursday night, Oct. 10, 2024. Background: Rising Dragon Acquisition Corp. filed its S-1 on June 7, 2024, and disclosed the terms for its SPAC IPO: 5.0 million units at $10.00 each to raise $50.0 million. Each unit consists of one ordinary share and one right to receive one-tenth of one ordinary share upon the consummation of an initial business combination.)

Star Fashion Culture Holdings Ltd. STFS Cathay Securities/WestPark Capital, 2.2M Shares, $4.00-4.00, $8.6 mil, 10/11/2024 Priced

(Incorporated in the Cayman Islands)

Star Fashion is a content marketing solutions services provider with a mission to offer high-quality diversified services. We offer services focusing on (i) marketing campaign planning and execution; (ii) offline advertising services; and (iii) online precision marketing services. We assist customers in enhancing the effectiveness of their marketing activities and the value of their brand and products through our variety of services offered. The Group first began operations in August 11, 2015, through its operating subsidiary, Xiamen Star Fashion Culture Media Co., Ltd.

The market size of the content marketing industry has experienced fluctuations in the past five years, growing from RMB286.3 billion in 2017 to RMB312.0 billion in 2022 at a CAGR of 1.7%. From 2017 to 2019, the overall content marketing industry went through stable growth due to the continuous growth of cultural and entertainment consumption of Chinese citizens. The COVID-19 pandemic led to suspension of offline activities and the market size has represented a downward trend in 2020. The market has bounced back in 2021 at RMB317.9 billion due to the control of the pandemic. However, the market size of marketing campaign planning and execution industry has declined to RMB312.0 billion in 2022 due to the spread of Omicron carient in 2022. As travel restrictions have been released at the end of 2022, the Company believes the market is will recover rapidly along with the iteration of traditional marketing campaign planning, empowerment from new technology, and prosperity of the economy. The market size of content marketing in the PRC is expected to reach RMB419.1 billion in 2027, representing a five-year CAGR of 6.1%. For more information, please see Industry Review on page 71.

With the capabilities of project planning, design, operation and execution, we assist customers in enhancing the effectiveness of their marketing activities and the value of their brand through content marketing programs.

Our primary services include marketing campaign planning and execution, where we have marketed a variety of events, including marathons, sports events, and music festivals. We may provide in-house designed marketing solutions for customers looking to increase exposure to their product or event. We may also provide in-house designed marketing solutions for products and brand ambassadors looking to market their brand or products through traffic generated from the offline events. In implementing such marketing solutions, we may execute strategies including arranging with third-party suppliers for posters or procuring and arranging for promotional videos of the marketed product or brand to be displayed in different locations or at different times during the event. We perform design of posters or marketing material in-house, while working with third-party suppliers in order to produce the posters according to our design, as well as to produce promotional videos or performing the logistics of displaying the marketing materials. We may also integrate online media promotion strategies for our customers, including the provision of advertisement and marketing materials such as video or online articles on well-known leading online media channels, including Iqiyi, Xigua Channel, Weibo and WeChat. For online marketing content, we typically work with suppliers in order to post contents based on parameters that we provide.

Note: Net income and revenue are for the fiscal year that ended June 30, 2023.

(Note: Cathay Securities was named as the lead left joint book-runner in an F-1/A filing dated Aug. 29, 2024, to work with WestPark Capital, joint book-runner.)

(Note: Star Fashion Culture Holdings Ltd. priced its micro-cap IPO at $4.00 – the low end of its $4.00-to-$5.00 price range – and trimmed the IPO to price 2.15 million Class A ordinary shares – down from 2.6 million shares in the prospectus – to raise $8.6 million on Thursday night, Oct. 10, 2024.)

(Note: Star Fashion Culture Holdings Ltd. trimmed its IPO’s size to 2.6 million shares – down from 3.0 million shares – and kept the price range at $4.00 to $5.00 to raise $11.7 million, according to an F-1/A filing dated July 22, 2024. Background: The company filed its F-1 on June 14, 2024; it submitted confidential IPO documents in December 2023.)

ALE Group Holding Limited ALEH EF Hutton, 1.3M Shares, $4.00-6.00, $6.3 mil, 10/14/2024 Week of

We are a holding company incorporated in the BVI with all of our operations conducted in Hong Kong by our wholly owned subsidiary, ALE Corporate Services Ltd., also known as ALECS. (Incorporated in the British Virgin Islands)

We provide accounting and corporate consulting services to small and medium-sized businesses. Our services include financial reporting, corporate secretarial services, tax filing services and internal control reporting. Our business is operated through our wholly owned subsidiary, ALE Corporate Services Ltd. (ALECS), a Hong Kong company incorporated on June 30, 2014. Our goal is to become a one-stop solution for all the accounting, corporate consulting, taxation and secretarial needs of small and medium enterprises operating in Asia and the U.S.

**Note: Net income and revenue figures are in U.S. dollars (converted from Hong Kong dollars) for the fiscal year that ended March 31, 2023.

(Note: The company disclosed that E.F. Hutton was named the sole book-runner – replacing Prime Number Capital – according to an F-1/A filing dated March 26, 2024.)

FBS Global Ltd. FBGL WallachBeth Capital, 2.3M Shares, $4.50-5.00, $10.7 mil, 10/14/2024 Week of

(Note on corporate structure: The predecessor of our principal operating company was incorporated on March 9, 1996, in Singapore under the name Finebuild Systems Pte Ltd. Pursuant to a restructuring that took effect on August 2, 2022, FBS Global Limited, an exempted company incorporated in the Cayman Islands, through its wholly owned subsidiary, Success Elite Developments Limited, a company incorporated in BVI, became the ultimate holding company of our current principal operating subsidiary referred to herein as FBS SG. (Incorporated in the Cayman Islands) )

From its beginning as a construction company since 1996, FBS SG has developed into a premier integrated engineering company that provides a full suite of construction and engineering services. These services include the supply of building materials and precast concrete components, recycling of construction and industrial wastes, research, and development, as well as pavement consultancy services.

We are an established interior design and build (also referred to as “fit-out”) specialist in Singapore with a track record of over 20 years in institutional, residential, commercial and industrial building projects. Our scope of services comprises design, supply and installation of ceilings, partitions, timber deck, carpet, lead lining, acoustic wall panel, built-in furnishing, carpentry and mechanical & electrical services of a building. We also undertake main construction and building works projects.

**Note: Revenue is for the year that ended Dec. 31, 2023.

(Note: FBS Global Ltd. revived its micro-cap IPO and disclosed its revised terms on Aug. 13, 2024, in an F-1/A filing: The company increased the number of shares to 2.25 million – up from 1.88 million shares – and raised the lower end of its price range to $4.50 – up from $4.00 – so the new price range is $4.50 to $5.00 – to raise $10.69 million. The company named WallachBeth Capital as its sole book-runner, replacing Eddid Securities USA.)

(Note: FBS Global Ltd. postponed its IPO in April 2024, when it had been expected to price its micro-cap initial public offering on or around April 13, 202r. Background: FBS Global Ltd. says its assumed IPO price is $4.00 – the low end of its $4.00-to-$5.00 price range – on 1.875 million shares, according to an F-1/A filing dated Feb. 23, 2024. Background: FBS Global Ltd. cut its IPO’s size to 1.875 million shares – down from 2.75 million shares – and set the price range at $4.00 to $5.00 to raise $8.44 million, according to an F-1/A filing dated Dec. 29, 2023. In that Dec. 29, 2023, filing with the SEC, FBS Global Ltd. also disclosed that it has changed its sole book-runner to Eddid Securities USA from Pacific Century Securities.)

(Note: FBS Global Ltd. filed an F-1/A dated July 27, 2023, in which it trimmed the size of its IPO to 2.75 million shares – down from 3.75 million shares – at US$4.00 to raise $11.0 million. The number of shares – 2.75 million – will all be offered by the company – and this is the same as in the previous prospectus (F-1/A) filed on June 26, 2023. The difference: The selling stockholder’s 1.0 million shares are not highlighted in the July 27, 2023, prospectus. However, in the July 27, 2023, filing, there is a note that the selling stockholder still intends to sell up to 1.0 million shares. Background: FBS Global Ltd. filed an F-1/A on June 26, 2023, and updated its financial statements for the year ended Dec. 31, 2022. FBS Global Ltd. filed its F-1 on Jan. 30, 2023, and disclosed terms for its IPO: 3.75 million (3,750,000) shares at US$4.00 to raise $15.0 million. Of the 3.75 million shares in the IPO, the company is offering 2.75 million shares and the selling stockholder is offering 1.0 million shares. FBS Global Ltd. will NOT receive any proceeds from the sale of the selling stockholder’s shares. FBS Global Ltd. filed confidential IPO documents on Sept. 13, 2022.)

Jinxin TechnologyNAMI Craft Capital Management/ WestPark /R.F. Lafferty & Co., 1.9M Shares, $4.00-5.00, $8.5 mil, 10/14/2024 Week of

(Incorporated in the Cayman Islands)

We are an innovative digital content service provider in China. Leveraging our powerful digital content generation engine powered by advanced AI/AR/VR/digital human technologies, we are committed to offering our users high-quality digital content services through both our own platform and the content distribution channels of our strong partners.

We currently target K-9 students in China, with core expertise in providing them digital and integrated educational content, and plan to further expand our service offerings to provide premium and engaging digital contents to other age groups. We were the largest digital textbook platform and a leading digital educational content provider for K-9 students in China, both in terms of revenue in 2022, according to Frost & Sullivan. We collaborate with leading textbook publishers in China and provide digital version of mainstream textbooks used in primary schools and middle schools. Our digital textbooks primarily cover Chinese and English subjects used in K-9 schools in China. We also create and develop digital self-learning contents and leisure reading materials in-house. Our AI-generated content technology enables our comprehensive digital contents to deliver an interactive, intelligent and entertaining learning experience.

Textbooks have been the primary teaching instrument for most children. Access to an advanced and intelligent version of textbook is becoming a rising demand, particularly among K-9 students who are at early stage of learning and forming an efficient learning style. There are currently over 150 million K-9 students in China while the digitization rate of textbook remains relatively low. Since our inception in 2014, we have built expertise in creating digitized, interactive and intelligent textbooks that we believe improve K-9 students’ learning experience. Previously, CDs were the most common learning equipment used by K-9 students to assist with studying textbook in China. We are committed to replacing outdated learning materials and equipment with our intelligent, interactive digital products and resources, and eventually cultivate a fresh and innovative learning style.

We are authorized by major Chinese textbook publishers to digitize their proprietary textbooks, and design and develop the digital version. Besides digital textbooks, leveraging our deep insights in China’s childhood education sector and our technological strength, we also provide digital self-learning materials and digital leisure reading materials, catering to the evolving and diversified needs of potential users. We have strong in-house content development expertise in digitized materials, amusement features, video and audio effects as well as art design. Our products and contents are imbued with the rich operational know-how and deep understanding of China’s childhood education sector, which we believe make our digital contents highly compelling to our users.

We distribute digital contents primarily through (i) our flagship learning app, Namibox, (ii) telecom and broadcast operators and (iii) third-party devices with our contents embedded. We launched our interactive and self-directed learning app Namibox in 2014, to provide users an integrated entry point to our digital textbooks, self-learning materials and leisure reading materials. Users can access various free contents, subscribe to advanced contents and choose to become premium members through our membership programs. In addition, we partner with all mainstream Chinese telecom and broadcast operators to tap into their large user base. Our partnered telecom and broadcast operators broadcast our various programs to end users through their respective platforms, distribute our educational contents to interested users and share certain percentage of revenues with us. Through networks of our partnered telecom and broadcast operators, individual users gain easy access to our digital contents through TVs or mobile devices. Furthermore, we cooperate with well-known hardware manufacturers, such as manufacturers of digital pads and intelligent TVs, and pre-install our programs in such devices directly. The integrated distribution channels empower us to increase our brand awareness in a cost-efficient manner, grow our user base sustainably and improve our contents continuously based on users’ real time feedbacks.

Our business has evolved significantly since inception and we have never stopped reimagining and innovating our products and digital contents. We are doing this not only to cater to, but influence, the learning habits and lifestyles of our users, to fulfill their goals and enrich their lives. With innovative and high-quality educational contents, we have built a trusted and well recognized brand, as well as a large user base throughout China. Since our inception, our Namibox app has amassed over 79 million cumulative downloads and more than 39 million registered users as of December 31, 2023. The high-frequency interactions we have with users and our unique access to a large amount of mission-critical learning data further provide us deep insights in K-9 education sector.

Fueling all of these great achievements are our technologies. We deploy advanced digitization technologies, AI technologies and big data analysis to provide superior user experience. We also deploy advanced AI technologies that power various teaching and voice assessment tools, all to improve the learning effectiveness for children. Leveraging our proprietary digital content generation engine, we are able to consistently refine and upgrade our educational contents, as well as to intelligently recommend content to our users, continually improving user experience.

We have realized steady growth with healthy financial performance since inception. Despite negative impacts caused by regulatory changes in the online education industry in 2021, our registered users increased from 29.9 million as of December 31, 2021 to 35.3 million as of December 31, 2022, and further to 39.5 million as of December 31, 2023. In addition, we recorded net income of RMB55.1 million and RMB83.5 million (US$11.8 million) in 2022 and 2023, respectively.

Note: Net income and revenue are for the year that ended Dec. 31, 2023.

(Note: Jinxin Technology Holding Company unveiled the terms for its IPO – 1.88 million American Depositary Shares – or 1,875,000 ADS – at a price range of $4.00 to $5.00 – to raise $8.46 million, according to an F-1/A filing dated Aug. 19, 2024. Each ADS represents 33.75 million ordinary shares. Background: Jinxin Technology filed its F-1 on Aug. 10, 2023 – about five months after submitting its confidential IPO documents to the SEC on March 24, 2023.)

Li Bang International Corporation Inc. LBGJ Craft Capital Management/ EF Hutton, 1.6M Shares, $5.00-6.00, $8.8 mil, 10/14/2024 Week of

Li Bang International Corporation Inc. was incorporated in the Cayman Islands on July 8, 2021. We conduct all of our operations in China through our Operating Subsidiaries in China. The main business of our Operating Subsidiaries is to design, develop, produce and sell stainless steel commercial kitchen equipment in China under our own “Libang” brand. Additionally, our Operating Subsidiaries provide customers with comprehensive services ranging from commercial kitchen design in the early stage to equipment installation and after-sales maintenance.

Our Operating Subsidiaries offer a range of commercial kitchen accessories covering steaming, cooking, baking, frying, disinfection, conditioning, refrigeration, and so on, in 13 series with more than 80 varieties, as well as stainless steel kitchen equipment, cooking and food preparation instruments, hotel supplies, and kitchen appliance accessories of more than 300 varieties. These products are used by a wide variety of customers such as governments, businesses, and public institutions. Additionally, our Operating Subsidiaries customize special products according to any customer’s project needs.

Our cookers include stoves, stir-fry stoves, steaming cabinets, and soup pots which are used in all kinds of commercial kitchens.

We also make fume and fresh air supply pipe systems as well as a waste processor.

Our production plant in China is more than 10,000 square meters. We use modern production facilities and state-of-the-art procedures. Furthermore, as a new technology enterprise in Jiangsu Province, we fall within the scope of advanced technology enterprises that benefit from key national support for residential companies that employ continuous R&D activities and transformational technical achievements to form core independent intellectual property rights.

Our Operating Subsidiaries mainly undertake projects of middle- and high-end customer groups by bidding on contracts. Our customer base consists of international hotels, companies, public institutions, educational institutions, hospitals and other facilities.

**Note: Net income and revenue are for the 12 months that ended Dec. 31, 2023.

(Note: Li Bang International Corp. named Craft Capital Management and EF Hutton as its joint book-runners, replacing WestPark Capital, in an F-1/A filing dated Aug. 23, 2024, for its small-cap IPO. Background: In an F-1/A filing dated June 18, 2024, Li Bang International Corp. cut its IPO’s size to 1.6 million shares – down from 5.0 million shares – and changed the price range to $5.00 to $6.00 – compared with $4.00 to $6.00 previously – to raise $8.8 million. Li Bang also said in the June 18, 2024, filing that the assumed IPO price is $5.00, the low end of the range; at that price, the IPO would raise $8.0 million.)

(Background: Li Bang International Corporation Inc. changed its sole book-runner to WestPark Capital – replacing Univest Securities – and updated its financial statements for the year that ended June 30, 2022, in an F-1/A filing dated June 1, 2023. Background: Li Bang International Corporation Inc. revised its IPO with a price range of $4.00 to $6.00 – with the low end of that range below its previous assumed IPO price of $5.00 and the high end of the range exceeding the previous assumed IPO price – while keeping the deal’s size at 5 million shares, according to an F-1/A filing dated Sept. 16, 2022. Li Bang International filed its F-1 on Jan. 27, 2022.)

Luda Technology GroupLUD Revere Securities/ Pacific Century Securities, 2.5M Shares, $4.00-4.00, $10.0 mil, 10/14/2024 Week of

We are a manufacturer and trader of stainless steel and carbon steel flanges and fittings products.(Incorporated in the Cayman Islands)

Our history began with Luda HK which was incorporated in Hong Kong in 2004 and is principally engaged in the trading of steel flanges and fittings. In 2005, the Company’s business expanded further upstream when Luda PRC was set up to commence the manufacturing of flanges and fittings with self-owned factory in China. We have established an operation history of over 20 years. We are principally engaged in (i) the manufacture and sale of stainless steel and carbon steel flanges and fittings products; and (ii) trading of steel pipes, valves, and other steel tubing products. We are headquartered in Hong Kong with manufacturing base in Taian City, Shandong Province of the PRC. Our sales network comprises customers from China, South America, Australia, Europe, Asia (excluding China) and North America and our customers comprise manufacturers and traders from the chemical, petrochemical, maritime and manufacturing industries.

(Note: Luda Technology Group filed an F-1/A dated Sept.20, 2024, disclosing the terms for its IPO: 2.5 million shares at $4.00 to raise $10.0 million.)

SAG Holdings LtdSAG Wilson-Davis & Co./Dominari Securities, 1.0M Shares, $8.00-8.00, $8.0 mil, 10/14/2024 Week of

We are a holding company incorporated in the Cayman Islands. The ordinary shares offered in the IPO are being offered by the holding company.

We are a Singapore-based provider of high-quality OEM, third-party branded and in-house branded replacement parts for motor vehicles and for non-vehicle combustion engines serving a number of industries. We distribute spare parts through operations primarily based in Singapore and global sales primarily generated from the Middle East and Asia. Through our On-Highway Business, we supply a wide range of genuine OEM and aftermarket parts for use in passenger and commercial vehicles bearing either the manufacturer’s brands or our in-house brands through SP Zone. Through our Off-Highway Business, we supply a wide range of components and spare parts for internal combustion engines with strong focus on filtration products through Filtec. Our Off-Highway Business serves industrial sectors that include marine, energy, mining, construction, agriculture, and oil and gas industries. Our products are sourced from genuine OEM and global premium aftermarket brands to suit the diverse needs of our customers. Over the past several years, our revenues have been relatively evenly split between our On-Highway Business and our Off-Highway Business, and approximately 10% of our revenues are derived from sale of our in-house products.

Our Group’s business can be traced back to the early 1970s, when our late founder, KE Neo, set up Chop Kim Aik, a retail shop specializing in the supply of British-made truck spare parts. KE Neo leveraged his experience as the owner of a transportation business with a fleet of trucks serving the construction industry to building a small retail shop to a large-scale operation with a solid customer base and a recognizable brand.

In 1983, we diversified into the supply of Japanese made automotive spare parts to capitalize on the increase in demand for Japanese vehicles in Singapore. Riding on this global growth of Japanese automotive exports, CE Neo, with the support of his father KE Neo, set up its first automotive spare parts retail outlet in Singapore, naming it Soon Aik Auto Parts Trading Co (which became a private limited company, Soon Aik Auto Parts Trading Co. Pte Ltd in 1995, and is now known and hereinafter referred to as “SP Zone”) specializing in trading Japanese made automotive spare parts, primarily used in passenger and commercial vehicles.

In the late 1980s, SP Zone achieved a major milestone when it was appointed as an authorized dealer of UD Trucks Corporation (“Nissan UD”) automotive genuine spare parts in Singapore, expanding our business of selling authorized genuine spare parts, beyond our historical aftermarket spare parts business model. The business gradually expanded, and the outlet grew to supply automotive spare parts for trucks operating in Singapore sold by respected Japanese brands from the manufacturers such as Nissan UD, Mitsubishi Fuso Truck and Bus Corporation, Hino Motors Ltd and Isuzu Motors Ltd.

In 1993, Jimmy Neo and CK Neo, brothers to CE Neo and sons of KE Neo, joined SP Zone, to assist with the expanding business. In 1995, Jimmy Neo was instrumental in securing the dealership with Cummins Asia Pacific Pte. Ltd (“Cummins”) for Fleetguard filters, a product used in Cummins engines, pursuant to which SP Zone started distributing filters to the marine, energy, mining, agriculture, oil and gas, and construction industries (referred to as the “Off-Highway Business”) in addition to the automotive industry (referred to as the “On-Highway Business”).

In 1995, SP Zone became a private limited company and expanded its sales channels to include exports to ASEAN markets, capitalizing on unmet demand as there were few suppliers supplying automotive spare parts to those markets at that time. Another major milestone in 1995 occurred when Edward Neo, the third brother and son of KE Neo, joined our Group to manage the local wholesale and retail business, allowing CE Neo to focus on our Group’s newly expanded export business. At this point, the business had grown from a small retail operation to regional family business run by a father and his four sons with multiple areas of focus and utilizing the family member’s different areas of expertise.

In 1999, SP Zone secured another line of filtration products when it was appointed as a distributor for Parker Racor, a line of Parker Hannifin filtration products. Subsequently, we established Filtec as a separate Singapore subsidiary to carry out sales of Off-Highway Business dedicated to handling sales to our Off-Highway customers in the industrial sectors.