Emerging Market Links + The Week Ahead (March 17, 2025)

Asian stocks valuation mean reversion, Brookfield's & PM Carney's China ties, Baidu's challenges, Singapore construction stocks, Dino Polska, more EM stock picks & the week ahead for emerging markets.

I have removed the “📰🔬 Further Suggested Reading” section of this post so I can spend more time and focus on the stock section before that (who’s section I have added some geographic headers as on desktop browsers, an autogenerated table of contents will appear on the left side of the screen) and to try to clean out my email inbox.

It looks like the investment writing ecosystem has grown on Substack to the point where it will start to rival Seeking Alpha’s who’s 20-something year old English major editors can be a real pain to deal with (trust me on that! … albeit SA has clear format standards and its their prerogative to enforce them for consistency…) - someone messaged me a link to an article included below about a Chinese stock rejected by them that they published on this platform.

If anyone has found a good way or tricks to find certain types of Substack pieces without subscribing to hundreds of Substacks or cluttering up a Notes feed (since the focus here is on emerging market and international stocks), let me know in the comments - not sure how useful AI or whether feed reader services I have already experimented last year (as discussed here and here) might help...

🔬 Emerging Market Stock Pick Tear Sheets

$ = behind a paywall

🌐 Emerging Market Stock Picks (Mid-March 2025) Partially $

Testing Grok AI

🇮🇩 Indonesia: GoTo Gojek Tokopedia PT Tbk, Mayora Indah Tbk PT, BFI Finance Indonesia Tbk PT & Bumitama Agri Ltd

🇸🇬 Singapore: IFAST Corporation Ltd, AIMS APAC REIT, GuocoLand Limited, Singapore Telecommunications Ltd, SEA Ltd, SembCorp Industries & OKP Holdings Ltd

🇹🇭 Thailand: Global Power Synergy PCL, Siam Wellness Group PCL, Bangkok Dusit Medical Services PCL, BGrimm Power PCL, Chularat Hospital PCL, Ngern Tid Lor PCL & Bangkok Chain Hospital PCL

🇿🇦 South Africa: Grindrod Limited, Curro Holdings, Stadio Holdings Ltd, Combined Motor Holdings (CMH), Mustek & Italtile

🇲🇽 Mexico & Central America: El Puerto de Liverpool SAB de CV, Fomento Economico Mexicano SAB de CV, Genomma Lab Internacional SAB de CV, Gentera SAB de CV, Alsea SAB de CV, La Comer SAB de CV & Grupo Aeroportuario del Sureste (ASUR)

🌐 EM Fund Stock Picks & Country Commentaries (March 16 2025) Partially $

Aberdeen brings back vowels, red flags for investing in emerging markets, Taiwan trip report, SA budget, why consider frontier markets debt, Europe 2025 stocks, fund updates & annual reports, etc.

📰🔬 Emerging Market Stock Picks / Stock Research

$ = behind a paywall / 🗃️ = Link to an archived article

Asia

🌏 Asian Equities: Valuation Mean Reversion - The Winners and Losers (Smartkarma) $

Valuations across Asia are mean reverting - expensive markets derating and the cheap ones rerating. We think this is likely to continue somewhat longer.

We think HK/China could rerate more; India and Taiwan could derate slightly further. India looks interesting. Valuation range has structurally shifted upwards. But another 5-10% relative valuation correction is warranted.

Principal stock choices in HK/China, Korea and India pertain to themes of domestic consumption, AI resilience and unloved sectors. Some of the companies have mitigating strategies for the tariff war.

🇨🇳 China

🇨🇳 Is Baidu fumbling it again? Again! (The Great Wall Street - Investing in China)

Not Just Autonomous Driving and AI are under attack—PDD Holdings (NASDAQ: PDD) or Pinduoduo Is Coming for Baidu (NASDAQ: BIDU) Too

I was skeptical enough about Baidu’s future in AI, given its recent missteps with large language models. But with Pinduoduo’s latest attack on Baidu—things are even worse with their AI business. But I’m getting ahead of myself. After taking a closer look at the autonomous driving landscape, I realized Baidu’s self-driving unit is basically the sequel to their AI saga: same plot, same shaky execution

Take their core search business, for instance—once the crown jewel of China's internet landscape. It’s painful to watch it gradually crumble, overshadowed by sharper competitors. Pinduoduo’s recent attack might be the final blow to Baidu’s cash cow. Not too long ago, Baidu was part of China's elite BAT trio—Baidu, Alibaba (NYSE: BABA), and Tencent (HKG: 0700 / LON: 0LEA / FRA: NNND / SGX: HTCD / OTCMKTS: TCEHY)—each roughly equal in market cap. Now, Alibaba and Tencent are giants nearly ten times the size of Baidu. The reason isn't complicated: execution.

Yet, the competitor that makes me most concerned for Baidu is Xiaomi (HKG: 1810 / SGX: HXXD / FRA: 3CP / OTCMKTS: XIACF). Led by Lei Jun—a man whose operational prowess genuinely impresses me—Xiaomi excels precisely because they dominate markets that have brutal competition and razor-thin margins, like smartphones. Even Apple, with seemingly unlimited resources, threw in the towel after years of unsuccessful attempts at car-building. Xiaomi, in contrast, entered the automotive arena just two years ago and impressively delivered 135,000 vehicles in only nine months.

🇨🇳 Alibaba Group’s AI Power Move—Can It Outpace DeepSeek and OpenAI? (Smartkarma) $

Alibaba (NYSE: BABA) has made a significant move in the AI space with the release of its latest artificial intelligence model, QwQ-32B, as it seeks to establish itself as China’s leading AI developer, challenging DeepSeek.

The model, which excels in mathematical reasoning, coding, and problem-solving, demonstrates capabilities comparable to both DeepSeek’s R1 and OpenAI’s latest technology.

However, a key differentiator is its size, as QwQ-32B operates with only 32 billion parameters compared to DeepSeek R1’s 671 billion.

🇨🇳 How Tencent Became the Most Powerful Tech Investor in the World (Coughlin Capital)

Tencent (HKG: 0700 / LON: 0LEA / FRA: NNND / SGX: HTCD / OTCMKTS: TCEHY)'s 1,200+ investment portfolio includes over 120 unicorns valued at $1B+.

Over the past decade, Tencent has strategically invested billions in over 1,200 companies worldwide, amassing a diverse portfolio that reads like a who's who of tech darlings. Epic Games (creators of global phenomenon Fortnite)? Check. Elon Musk's Tesla? Yep. Music streaming giant Spotify? You bet.

What sets Tencent apart is its uncanny ability to spot winners early. The company has a knack for backing promising startups before they become the next big thing. And with each prescient pick, Tencent not only strengthens its own hand but also gains valuable insights into the latest tech trends.

🇨🇳 Lenovo: Focus On PC Growth And Server Profitability (Seeking Alpha) $ 🗃️

🌐 Lenovo Group (HKG: 0992 / FRA: LHL / LHL1 / OTCMKTS: LNVGY / LNVGF) - Designing, manufacturing & marketing consumer electronics, PCs, software, servers, converged & hyperconverged infrastructure solutions, etc. 🇼

🇨🇳 Tianju Dihe quietly tallies big profits on latest China tech boom (The Bamboo Works)

The low-profile company posted strong double-digit profit growth last year on rising demand for its data-transfer services

Tianju Dihe Suzhou Technology Co Ltd (HKG: 2479) said its net profit last year increased as much as 51% on the back of solid revenue growth

Demand for the company’s services is on the rise as China’s digital economy expands, helped by favorable government policies

🇨🇳 JD.com: Still Severely Undervalued (Bulls On Parade)

The Silent Giant Powering China’s Online Shopping Boom

Chinese equities are starting 2025 strong. In a previous post I outlined why I started investing in JD.com (NASDAQ: JD) and Alibaba (NYSE: BABA) in 2024. I am still very bullish on both companies and the Chinese economy overall, I believe there is still plenty of room for these equities to run from a value perspective. JD recently released earnings on March 6th, 2025 and I thought I would spend some time examining the results as well as analyzing JD more in depth in this post.

🇨🇳 Investment thesis on JD.com (Black Swan Investor)

Chinese E-commerce Giant focused on Quality

JD.com (NASDAQ: JD) and Alibaba (NYSE: BABA) on the other hand, focuses more on direct sales and providing a robust logistics network. Customers generally go to them for larger ticket items like electronics and appliances. While this results in additional capital needs to manage inventory, it also comes with much better control over the product sold. For China, where counterfeiting and product quality is often a big concern, I think this offers a unique and significant advantage.

🇨🇳 China Yuchai: Deep Value Meets Growth (NYSE:CYD) (Maius Partners)

With undervalued assets, a newly enhanced strategic JV with Rolls-Royce, and exposure to booming data center demand, CYD is a deep value investor’s dream.

China Yuchai International Limited (NYSE: CYD) is one of China’s largest diesel engine manufacturers, boasting strong global partnerships, including a 50/50 joint venture (JV) with Rolls-Royce’s MTU division. The company is poised for an earnings inflection driven by surging data center demand for backup power generation solutions. Despite 20% p.a. earnings growth potential over the next five years, CYD trades at an astonishingly low valuation of 2x EBITDA, 0.3x book, 30% free cash flow yield, and a net cash balance sheet that supports 90% of the company’s market cap. This stands in contrast to its peers, which have experienced substantial re-ratings. Enhanced corporate governance, coupled with a long-term activist investor on board, has led to significant buybacks, with the company repurchasing nearly 10% of its outstanding shares in recent months to take advantage of the valuation discount.

🇨🇳 ECARX reports its first profit, expects added revenue from Volkswagen tie-up (Bamboo Works)

The maker of digital cockpits used in smartcars reported its revenue rose 4% in the fourth quarter, as one of its main profit metrics turned positive for the first time

A new partnership between Ecarx Holdings (NASDAQ: ECX) and ‘a well-known European OEM’ could bring the digital cockpit maker up to 10 billion yuan in revenue, according to UBS

ECARX reported its first-ever adjusted EBTIDA profit in the fourth quarter and indicated confidence at maintaining that profitability, as its quarterly net loss narrowed sharply

🇨🇳 Leapmotor jumps to first-ever quarterly profit (Bamboo Works)

Investors have grown bullish on the NEV maker after it delivered more than 40,000 vehicles last December

Zhejiang Leapmotor Technology Co Ltd (HKG: 9863) reported its first ever quarterly profit in last year’s fourth quarter, as its loss for the year narrowed by 33%

The company’s newly launched B10 model will be a key product targeting the lower end of the new energy vehicle market

🇨🇳 Hello Group takes its matchmaking skills beyond China (Bamboo Works)

The operator of the Momo dating app said revenue from its global business could potentially double to 2 billion yuan this year

Hello Group (NASDAQ: MOMO)’s revenue fell 12% in the fourth quarter, while its net income plunged 59%, hurt by a livestreaming crackdown and declining users

The company is pivoting to international markets through its Soulchill and other new apps, targeting overseas revenue growth of up to 100% this year.

🇨🇳 Can a stale Ajisen float back to the top of China’s noodle pot? (Bamboo Works)

The once-dominant ramen house’s business has slumped on a mix of intensifying competition and lower consumer spending

Ajisen (China) Holdings Ltd (HKG: 0538 / FRA: AJN / OTCMKTS: AJSCF) said it lost up to 40 million yuan in 2024, reversing a profit of 180 million yuan in the previous year

The former ramen noodle king’s store count sank to 575 in the first half of 2024 from a peak of 799 in 2019

🇨🇳 Xiabuxiabu gets chilled by China’s weak economy (Bamboo Works)

The personal hotpot restaurant chain warned its revenue fell and its losses grew last year as increasingly cautious Chinese consumers cut back their spending

Xiabu Xiabu Catering or XBXB (HKG: 0520 / FRA: 0XI / OTCMKTS: XIAXF) said it expects to report its revenue slid by 20% last year, while its net loss doubled

The restaurant operator’s weak performance accelerated in the second half of the year, after its revenue slid 15.9% and it fell into the red in the first half

🇨🇳 ATRenew launches major store expansion to raise service accessibility, company profile (Bamboo Works)

The recycling specialist said it plans to nearly triple its national network of brick-and-mortar AHS Recycle stores to 5,000 over the next three years

ATRenew (NYSE: RERE) has launched a major expansion of its brick-and-mortar store network to boost its brand and retail sales, and increase its supply of recycled products

The recycling specialist is still tweaking several of its newer initiatives, including its iPhone partnership with Apple and expansion outside China

🇨🇳 The Nationalism Factor, and a Forced Asset Sale (Bamboo Works)

Nationalism: A fleeting catalyst

Nationalism and geopolitics are increasingly shaping the investment landscape in China, as recent events are showing. The remarkable box office success of “Ne Zha 2” is more than just a cinematic triumph — it’s a manifestation of national pride that has spurred significant market movements. The film’s domestic performance, with revenues approaching $2 billion and widespread repeated viewings, even leading to theaters being entirely rented out by wealthy businessmen for free mass screenings, has been a key factor in the near tripling for the stock of its producer, Beijing Enlight Media Co Ltd (SHE: 300251). While such enthusiasm can drive short-term gains, it’s important to recognize that investing purely on the basis of patriotic sentiment is inherently risky and unsustainable over the long term.

🇨🇳 Brookfield’s Deep Ties to Chinese Land, Loans, and Green Deals—And a Real Estate Tycoon With CCP Links—Raise Questions as Carney Takes Over from Trudeau (The Bureau via Zerohedge)

[Brookfield Infrastructure Corp (NYSE: BIPC) / Brookfield Infrastructure Partners L.P. (NYSE: BIP) / Brookfield Renewable Partners L.P. (NYSE: BEP) / Brookfield Renewable Corporation (NYSE: BEPC)]

Brookfield Bet Billions on Shanghai Land as China’s Market Peaked and Secured $276 Million Bank of China Refinancing Under Mark Carney as Market Crashed

A review of corporate documents reveals that Brookfield—the influential $900 billion Canadian investment fund from which Liberal Prime Minister-to-be Mark Carney stepped away from in order to replace Justin Trudeau as Canada's leader—maintains over $3 billion in politically sensitive investments with Chinese state-linked real estate and energy companies, along with a substantial offshore banking presence. One of its major real estate ventures, a $750 million entry into high-end Shanghai commercial property in 2013, involved a Hong Kong tycoon affiliated with the Chinese People's Political Consultative Conference (CPPCC)—which the CIA labels a central "united front" entity of Beijing.

The investment occurred while China's real estate bubble was peaking. Last year, as China's market crashed, and vacancies soared in Shanghai, Brookfield under Carney secured hundreds of millions of dollars in loans from the Bank of China to refinance its Shanghai commercial land holdings. According to The Bureau's research, this emergency loan came a decade after Carney, serving as Governor of the Bank of England, aided Beijing by facilitating the Bank of China's expansion of its global financial footprint. In his 2013 speech, UK at the Heart of Renewed Globalisation, Carney announced that "The Bank of England [has] signed an agreement with the People's Bank of China … Helping the internationalisation of the Renminbi is a global good."

🇨🇳 No respite for RemeGen as problems and losses pile up (Bamboo Works)

The developer of innovative drugs has sustained a series of blows to its finances, corporate partnerships, management team and star product, leaving investors jittery

Despite rising revenue, RemeGen (HKG: 9995 / SHA: 688331 / FRA: REG / OTCMKTS: REGMF) is grappling with losses amounting to 4 billion yuan over the past three years

The company has failed to complete a planned private placement and is facing a cash flow crunch

🇨🇳 52Toys taps China’s designer toy boom in play for Hong Kong IPO (Bamboo Works)

As China’s collectible toy market surges, the company is hoping to fund an aggressive expansion and build iconic IPs with a new listing

52Toys has hired investment banks for a planned Hong Kong IPO, following the listing of rival Bloks Group Ltd (HKG: 0325) earlier this year

The collectible toymaker faces growing competition abroad and lags its domestic rivals in developing its own intellectual property

🇭🇰 CK Asset Has Rebounded, But 2025 Still Offers A Lot Of Challenges (Seeking Alpha) $ 🗃️

🌐 CK Asset Holdings (HKG: 1113 / FRA: 1CK / OTCMKTS: CHKGF) 🇰🇾 - Property development & investment, hotel & serviced suite ops, property & project management, pub operation & investment in infrastructure & utility asset operation. 🇼

🇭🇰 ESR Group (1821 HK): Steady Progress (Smartkarma) $

ESR Group Ltd (HKG: 1821 / FRA: 3K6 / OTCMKTS: ESRCF)’s preconditional scheme offer from the consortium is either cash (HK$13.00), scrip or a combination of cash/scrip. The offer is final.

On 7 March, the consortium disclosed two additional irrevocable (3.47% of outstanding shares) and satisfied two regulatory preconditions (UK FCA and Singapore MAS).

Since announcing the offer, peers have materially derated, lowering the vote risk. At the last close and for an end August payment, the gross/annualised spread is 4.5%/10.1%

🇭🇰 Goldlion Holdings (533 HK) Privatization - The Offer Price Is Acceptable (Smartkarma) $

In recent years, [manufactures and distributes apparel] Goldlion Holdings Ltd (HKG: 0533 / FRA: GLH / OTCMKTS: GLLHF) is facing performance headwinds. Both revenue and net profit have shown a downward trend due to declining consumption, real estate crisis and unfavorable external factors.

In short term, the weak consumer confidence and market momentum are unlikely to improve. Goldlion's performance may gradually pick up in 2026 and 2027 but is still in downward trend.

Considering the low trading liquidity, weak fundamentals, uncertainties on performance brought by Goldlion's potential strategic transformation and the concerns on the outlook, we think the Cancellation Price is acceptable.

🇲🇴 Studio City International: Rolling The Dice In Macau's Jackpot Jungle (Seeking Alpha) $ 🗃️

🇲🇴 Studio City International Holding Ltd (NYSE: MSC) - Operates Studio City Casino (gaming, retail & entertainment resort) in Cotai, Macau. 🇼

🇲🇴 HK-listed Melco parent flags minimum US$107.8mln non-cash impairment on some Studio City assets (GGRAsia)

Melco International (HKG: 0200 / FRA: MX7A / OTCMKTS: MDEVF), Hong Kong-listed parent of casino operator Melco Resorts & Entertainment Ltd (NASDAQ: MLCO), says it expects to have a non-cash impairment of at least HKD838 million (US$107.8 million ) on “certain assets” from the overall group’s majority interest in the Studio City casino resort (pictured) in Macau’s Cotai district.

🇲🇴 MGM China ‘under levered’ so good bet as Thailand investment vehicle: Halkyard (GGRAsia)

The balance sheet of Macau casino operator MGM China Holdings Ltd (HKG: 2282 / FRA: M04 / OTCMKTS: MCHVF / MCHVY) is considered by its parent MGM Resorts International (NYSE: MGM) to be “under-levered”, which is a factor making the Macau unit an attractive vehicle for any foray into Thailand by the MGM casino brand.

That is according to Jonathan Halkyard (pictured in a file photo), chief financial officer (CFO) of the parent.

He stated: “The MGM China balance sheet is… under-levered compared to the performance of that business… thus the appeal potentially of using that balance sheet as a vehicle to develop a property in Thailand.”

🇲🇴 Galaxy, Sands saw 2024 Cotai mall net revenues dip y-o-y amid citywide retail biz retreat (GGRAsia)

Two operators of large Macau shopping malls – casino firms Galaxy Entertainment (HKG: 0027 / OTCMKTS: GXYEF) and Sands China (HKG: 1928 / FRA: 599A / OTCMKTS: SCHYY / OTCMKTS: SCHYF) – respectively saw their fourth-quarter and full-year 2024 net revenues from their Cotai mall businesses decline year-on-year. That is according to their latest annual financial results.

Mall net revenue at Galaxy Macau – Galaxy Entertainment’s flagship casino resort property in Cotai – amounted to HKD348 million (US$44.8 million) in the three months to December 31, a flat performance compared to the previous quarter. Galaxy Macau’s fourth-quarter mall net revenue saw a 4.4-percent year-on-year decline.

🇹🇼 Taiwan

🇹🇼 Silicon Motion: Upbeat Outlook, Attractive Share Price (Seeking Alpha) $ 🗃️

🌐 Silicon Motion Technology Corporation (NASDAQ: SIMO) - Designs, develops, & markets NAND flash controllers for solid-state storage devices. 🇼

🇹🇼 Automotive Drives Solid Revenue Base For Himax Technologies (Seeking Alpha) $ 🗃️

🌐 Himax Technologies (NASDAQ: HIMX) 🇰🇾 - Fabless semiconductor company providing display imaging processing technologies. 🇼

🇹🇼 Taiwan Semiconductor ($TSM) – This is now an absolute bargain (Rijnberk InvestInsights)

Here's my updated view of Taiwan Semiconductor Manufacturing Company (TSMC) (NYSE: TSM) after recent price pressure.

Mounting Chinese export fears, upcoming tariffs, and a global trade war are among the many factors currently impacting the market. Semiconductors are leading the decline, with the SMH semiconductor ETF losing about 18% since its January 22 high.

This includes one of the most important companies globally, Taiwan Semiconductor Manufacturing Company (TSM). After setting a well-deserved all-time high in late January, TSM shares have been on the decline, losing 23% since, giving up about four months of well-deserved gains and resulting in shares down about 10% YTD.

Is it justified?

Let’s find out!

🇹🇼 TSMC: Buy Case Remains Strong Despite DeepSeek Risks (Seeking Alpha) $ 🗃️

🇹🇼 TSMC: Don't Fear AI Investments (Seeking Alpha) $ 🗃️

🇹🇼 Taiwan Semiconductor: Company Is Selling The Shovels To The AI Race (Seeking Alpha) $ 🗃️

🇹🇼 TSMC: Solidifying Market Dominance (Seeking Alpha) $ 🗃️

🇹🇼 Taiwan Semiconductor: Thank You, Mr. Market, For The Gift (Seeking Alpha) $ 🗃️

🇹🇼 Taiwan Semiconductor: Set To Capture Majority Of AI Profits (Seeking Alpha) $ 🗃️

🌐 Taiwan Semiconductor Manufacturing Company (TSMC) (NYSE: TSM) - World's largest dedicated independent (pure-play) semiconductor foundry. 🇼 🏷️

🇰🇷 Korea

🇰🇷 Paradise Co to invest nearly US$400mln to build new Seoul hotel, announces financing (GGRAsia)

Paradise Co Ltd (KOSDAQ: 034230), an operator in South Korea of foreigner-only casinos, announced on Wednesday a plan to invest KRW575.0 billion (US$396.4 million) to build a new hotel in eastern Seoul’s Jangchung neighbourhood. The aim is for the new hotel to open in 2028, stated the firm in a filing to the Korea Exchange.

In a separate announcement, Paradise Co said it had secured a KRW550.0-billion loan facility from Woori Bank [Woori Financial Group (NYSE: WF)] to fund the construction of the new property in South Korea’s capital.

The financing is structured as a five-year loan, with a “lump-sum repayment due at maturity,” said the firm.

🇰🇷 Korea Electric Power: Dividends Are Back And Outlook Is Positive (Seeking Alpha) $ 🗃️

🇰🇷 KEPCO (NYSE: KEP / KRX: 015760 / FRA: KOP) or Korea Electric Power Corporation - Integrated electric utility company. Generation, transmission & distribution of electricity in Korea where it’s the largest electric utility. 🇼 🏷️

🇰🇷 An Update on the Potential KOSPI 200 Rebalance Candidates in June 2025 (Douglas Research Insights) $

We discuss the potential KOSPI 200 rebalance candidates in June 2025. In recent years, there have been some alpha generating stocks arising from the KOSPI 200 rebalances.

We include eight companies as potential inclusion candidates including LG CNS Co Ltd (KRX: 064400), HD Hyundai Marine Solution (KRX: 443060), Shift Up Corp (KRX: 462870), and Hanwha Engine Co Ltd (KRX: 082740).

The top 5 potential deletion candidates for KOSPI 200 rebalance in June 2025 include Iljin HySolus Co Ltd (KRX: 271940), Hansae Co Ltd (KRX: 105630), Foosung Co Ltd (KRX: 093370), Sama Aluminium Co Ltd (KRX: 006110), and TKG Huchems Co Ltd (KRX: 069260).

🇰🇷 Is Homeplus Debacle a Key Negative Tipping Point for MBK? (Douglas Research Insights) $

In this insight, we discuss how the Homeplus debacle is causing a major negative sentiment on MBK Partners from both the Korean government and the media.

This negative sentiment has grown so much that it could have a legitimate negative impact in the upcoming proxy vote for the control of Korea Zinc (KRX: 010130).

The Korean government has targeted MBK for tax probe. Plus, a coalition of securities firms is expected to file a lawsuit against Homeplus and MBK.

🇰🇷 Kakao Corp: Insiders Are Buying and Cancellation of Treasury Shares (Douglas Research Insights) $

Kakao Corp (KRX: 035720) has two near-term positive catalysts. First is treasury shares cancellation. Second is insiders buying of its shares.

These moves suggest the management's confidence in the company's outlook ahead of the AGM on 26 March.

In our view, one of the major reasons why the insiders are buying could be due to Kakao's collaboration with OpenAI.

🇰🇷 Hoban Group Purchases LS Corp Shares - Is This a Hanjin Kal 2.0? (Douglas Research Insights) $

In this insight, we discuss a new catalyst on the share price of LS Corp (KRX: 006260 which is the purchase of its shares by the Hoban Group.

Hoban Group has recently purchased shares of LS Corp. Although the exact percentage of shares has yet to be made public, it is estimated to be less than 3%.

LS Corp could improve shareholder returns. Plus, the ongoing litigation between Taihan Electric Wire (KRX: 001440) and LS Cable may be the real reason why Hoban decided to invest in LS Corp.

🇰🇷 Samsung SDI: Announces a 2 Trillion Won Rights Offering Capital Raise (Douglas Research Insights) $

On 14 March, Samsung SDI (KRX: 006400 / 006405 / FRA: XSDG) announced a 2 trillion won (US$1.4 billion) rights offering capital raise plan.

Samsung SDI's 2 trillion won capital raise is likely to have a near-term negative impact on the company's share price.

We are negative on Samsung SDI's rights offering capital raise mainly due to shares dilution. We also remain concerned that weak demand for EVs globally could last longer.

🇰🇷 SoCar: A Partial Tender Offer by SOQRI (Douglas Research Insights) $

After the market close on 13 March, it was reported that SOQRI Co will be doing a partial tender offer public offering of 171,429 common shares of [ride-hailing company] SOCAR Inc (KRX: 403550).

The tender offer period is from 14 March to 2 April. The tender offer price is 17,500 won which is a 21% premium to current price.

Socar's founder Lee Jae-Woong is pushing for a tender offer to solidify the control of Socar from Lotte Rental (KRX: 089860) which has recently been purchased by Affinity Equity Partners.

🇰🇷 Initial Thoughts on the Hanwha Energy IPO (Douglas Research Insights) $

Hanwha Energy, which is 100% owned by the Hanwha Group owner family members, has started the process of going public. Hanwha Energy could complete its IPO in 2025/2026.

One of the scenarios involving Hanwa Energy is that once it completes its IPO, it could merge with Hanwha Corp (KRX: 000880).

Hanwha Energy generated revenue of 4.7 trillion won (up 20% YoY) and operating profit of 215 billion won (up 306.5% YoY).

🇰🇷 DN Solutions IPO Preview (Douglas Research Insights) $

[Machine tool industry] DN Solutions is getting ready to complete its IPO in Korea in May 2025. The IPO price range is from 65,000 won to 89,700 won.

The book building for the institutional investors will last from 22 to 28 April. The expected IPO offering amount is from 1.14 trillion won to 1.57 trillion won.

The IPO price range is based on DN Solutions' net profit of 317.4 billion won, P/E of 25.2x, and IPO discount rates of 29.1% to 48.6%.

SE Asia

🇰🇭 🇻🇳 Hong Kong-based fund Argyle, investor in Southeast Asian casino operator Donaco, proposes a full buyout of firm (GGRAsia)

Donaco International Ltd (ASX: DNA), an operator of border casinos in Cambodia and Vietnam, has announced that it has entered into a binding agreement with one of its investors – a Hong Kong-based investment fund – for the latter to acquire 100 percent of Donaco’s shares.

Donaco stated in a filing to the Australian Securities Exchange on Monday morning that it had “entered into a binding scheme implementation deed with On Nut Road Ltd” for the latter’s “proposed acquisition of 100 percent of the shares in Donaco that it does not already own, via a scheme of arrangement for AUD0.045 [US$0.028] cash per Donaco share.”

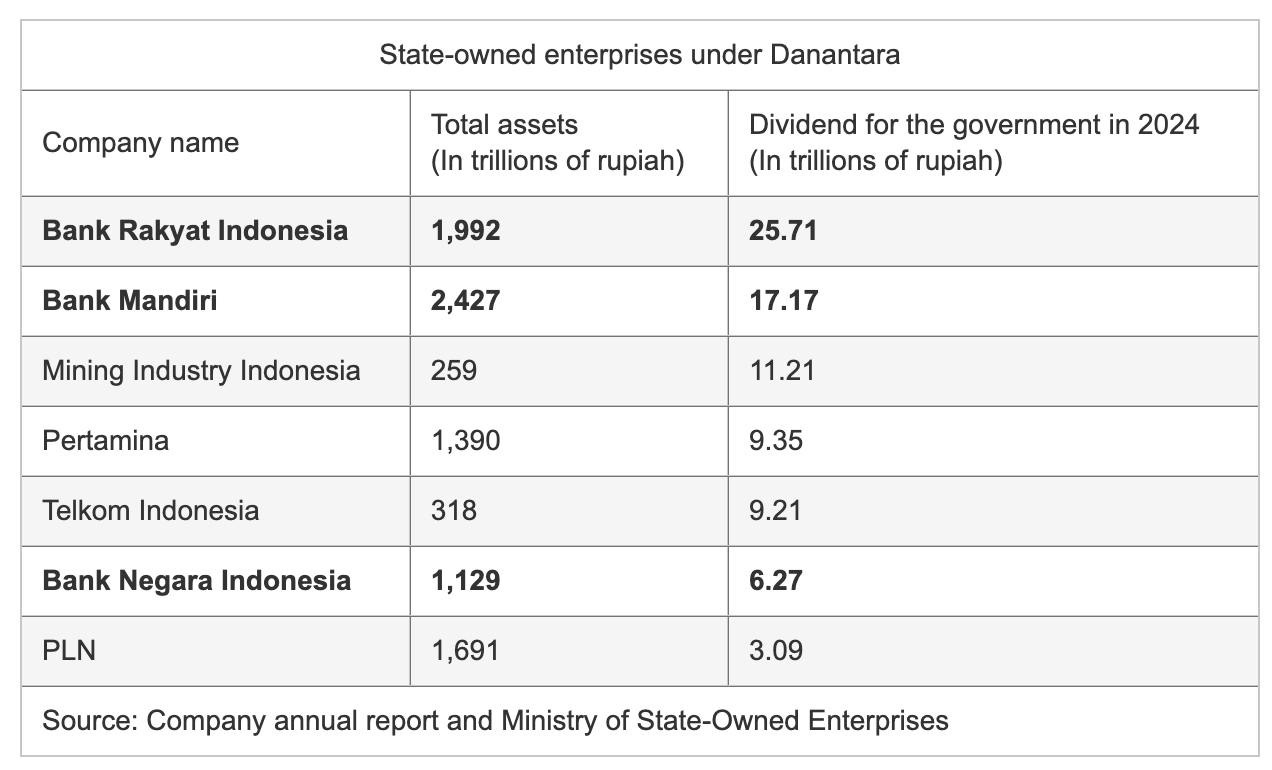

🇮🇩 Bottom-fishing in Indonesia (Asian Century Stocks) $

Indonesians seem disgruntled by the new administration. There have been reports of corruption in his school lunch program. High interest rates and recent austerity measures have hurt consumer confidence. People are suspicious of Prabowo’s new sovereign wealth fund

I’m aware that many of you don’t have trading access to Indonesian equities. For those of you who don’t have access, I suggest you set up a pan-Asian brokerage account with Phillip Securities in Singapore or Boom Securities in Hong Kong.

Instead, Danantara has been set up to take control of 65 state-owned enterprises from the Ministry of State-Owned Enterprises. The total amount of SOE assets to be injected into Danantara will amount to nearly US$1 trillion — a significant number, even for Indonesia.

🇲🇾 Rebranded bailout of Sapura Energy (Murray Hunter)

The Malaysian government, under Prime Minister Anwar Ibrahim, has introduced new terminologies and justifications to rationalize the bailout of troubled Bumiputra-linked companies.

The latest case in point is Sapura Energy Bhd (KLSE: SAPNRG), which recently received a RM1.1 billion capital injection from the government through Management Development Holdings Sdn Bhd (MDH), an agency under the Ministry of Finance.

Sapura Energy’s financial troubles are well-documented. While it is now under new management, there is little indication that the company has a clear pathway to long-term financial viability.

🇸🇬 5 Singapore Stocks That Could Benefit from the Construction Resurgence (The Smart Investor)

It’s looking positive for Singapore’s construction sector as the government and private sector line up a host of projects for the island.

The sector is experiencing a resurgence as demand for public housing has spurred the HDB to build more flats. From 2025 to 2027, 50,000 new flats are slated to be released.

There are also major projects announced such as Changi Airport’s Terminal 5 expansion, Tuas Megaport, and Marina Bay Sands expansion plans.

Here are five Singapore stocks that could ride on the construction upswing to do well.

Lum Chang Holdings Ltd (SGX: L19) owns businesses in property development, investment, and interior finishing works.

Tiong Woon Corporation Holding Ltd (SGX: BQM) is a one-stop integrated heavy lift specialist and service provider.

Boustead Singapore (SGX: F9D / OTCMKTS: BSTGF), or BSL, is a conglomerate with four key divisions – energy engineering, real estate, geospatial technology, and healthcare.

Koh Brothers Eco Engineering Ltd (SGX: 5HV) is a sustainable engineering solutions group providing engineering, procurement, and construction (EPC) services for water and wastewater treatment, bio-refinery, and hydro-engineering.

Hock Lian Seng Holdings Limited (SGX: J2T), or HLS, has undertaken a wide range of civil engineering and infrastructure projects for both the public and private sectors in Singapore.

🇸🇬 4 Attractive Mid-Cap Companies Posting Higher Profits (The Smart Investor)

Here are four mid-sized companies that reported better profits during the recent earnings season.

Audience Analytics Ltd (SGX: 1AZ) is a business enabler with products ranging from printed publications and online portals to exhibitions and business award programmes.

Tai Sin Electric Ltd (SGX: 500) is a cable manufacturer for Singapore and the Southeast Asian region.

Spindex Industries Ltd (SGX: 564) is an integrated solutions provider of precision-machined components and assemblies.

Isoteam Ltd (SGX: 5WF) is an established player in Singapore’s building maintenance and estate upgrading industry and has successfully undertaken more than 900 refurbishment and upgrading projects since inception.

🇸🇬 CDL Plunged to a New 16-Year Low Amid Boardroom Dispute: Can the Blue-Chip Property Group Recover? (The Smart Investor)

City Developments Limited (SGX: C09 / FRA: CDE / OTCMKTS: CDEVY), or CDL, used to be Singapore’s largest listed developer.

However, a boardroom tussle which broke out in late February caused shares of CDL to plunge to a 16-year low of S$4.76.

With this decline, UOL Group Limited (SGX: U14 / FRA: U1O / OTCMKTS: UOLGY / UOLGF) has now overtaken CDL as Singapore’s largest listed developer.

Can CDL retake its crown as Singapore’s largest developer? What will it take for the property giant to regain its former glory?

Continued infighting

A downbeat set of earnings

“GET” strategy in place.

Get Smart: Sentiment will remain weak

🇸🇬 SATS: Integrating WFS –Key to Acquisition Success (Corporate Monitor)

The acquisition of WFS by SATS Ltd (SGX: S58 / FRA: W1J / OTCMKTS: SPASF) is undeniably transformational, propelling SATS—once primarily a Singapore-based company focused on food solutions and ground handling—into the global stage. The WFS acquisition not only boosts revenue substantially, but it also expands SATS’s geographic reach, multiplies its workforce, and expands its air cargo operations to a global scale.

We commend SATS’s management and board for making this bold decision during the challenging COVID period, especially when many doubted the return of air travel to pre-pandemic levels. SATS chose action over inaction, even though the error of omission was likely not apparent.

Our reservation lies in the reported valuation of the acquisition. WFS enjoyed a temporary boost in earnings before interest, tax, depreciation, and amortization (“EBITDA”) due to COVID-related relief measures. While traditional metrics might suggest an EV/EBITDA ratio of 9.7x, based on the previous 12 months’ EBITDA, a more realistic multiple—after discounting the COVID boost—could be as high as 14.3x. This discrepancy suggests that the acquisition may not have been as attractively priced as it initially appeared.

🇸🇬 Sea Limited FY2024 Earnings (Saadiyat Capital)

Analysis of Earnings and Potential Catalysts Investors can Look out for

Regular readers on Substack must have seen the buzz around Sea Limited (NYSE: SE)’s 4Q-24 earnings where the company outperformed across many metrics. Not only were revenues up 28.8% YoY, GMV reached $100 billion and the E-commerce segment was profitable on an Adjusted EBITDA basis for the first time on a full year basis. This highlights an inflection point in the business which was burning through cash not too long ago after coming out of COVID and was struggling to convince investors about its chances of achieving profitability. 4Q-24’s earnings provide a lot of interesting insights into the business and provide potential catalyst points investors can take advantage of. In this writeup, I will go through the earnings and then delve into commentary from the earnings call and notes from the documents to analyse points relevant for investors interested in Sea limited.

🇹🇭 Airports of Thailand: A Buy Despite Concerns About Retail Revenues (Seeking Alpha) $ 🗃️(?)

🇹🇭🏛️ Airports of Thailand PCL (BKK: AOT / SGX: TATD / FRA: NYVQ / OTCMKTS: AIPUY / AIPUF) - Managing, operating & developing airports. 6 international airports: Don Mueang, Phuket, Chiang Mai, Hat Yai, Chiang Rai & Suvarnabhumi. 🇼 🏷️

🇮🇳 India

🇮🇳 Inside Infosys’ $18.6B Revenue Engine: Hidden 31.9% Gross Margin Exposed (Business Model Mastery)

Discover How 64.7% Digital Services Propel Growth Despite Margin Pressures

Before we dive in, let me share two notable figures that set the stage. Infosys (NYSE: INFY) holds an 8.4% share in the global IT services market, placing it third in the industry after Accenture and TCS, and it earns around 64.7% of its revenue from digital services—an area experiencing substantial growth as more companies migrate to the cloud and explore advanced AI tools. You might already sense how critical these figures are. But there’s a lot more to unpack, from how Infosys prices its projects to which sectors are fueling its growth. Stick with me, and by the end, you’ll see exactly why these numbers matter.

🇮🇳 MakeMyTrip: Stretched Valuations Point To Further Correction (Seeking Alpha) $ 🗃️

🇮🇳 Makemytrip (NASDAQ: MMYT) - Online travel services. 🇼

🇮🇳 Coal India (COAL IN) Value Trap (Smartkarma) $

Coal India (NSE: COALINDIA / BOM: 533278)'s production growth during Apr-Feb 25 has slowed to 1.5% yoy due to a high base effect and is unlikely to grow significantly in the near future

Regulated pricing mechanism means low correlation to international price movements. E-auction (10-12% of volumes) prices crash -25% yoy in line with international trends, impacting profitability

Single digit PE is in line with historic multiples. Wage renegotiations due in June 2026, rising coal production from captive producers, surge in renewable capacities are headwinds

🇮🇳 The Beat Ideas: Narayana Hrudayalaya Ltd (NHL) ~ Driving Growth from India to Cayman Islands (Smartkarma) $

Narayana Hrudayalaya (NSE: NH / BOM: 539551) is a prominent player in the Indian healthcare sector, distinguished by its commitment to providing affordable, high-quality medical services.

The company established its first international hospital in the Cayman Islands in 2014, targeting patients from the Americas and Caribbean regions by offering competitively priced medical services

Management has outlined a capex guidance of around INR 4,000 crores over the next 3 to 4 years, funded by healthy cash flows and stable operating margins.

🇮🇳 The Beat Ideas: Shilpa Medicare (Smartkarma) $

Shilpa Medicare Ltd (NSE: SHILPAMED / BOM: 530549) will begin commercializing new molecules across segments, driving growth to new heights as older products are phased out, ensuring sustained progress and innovation in its business.

In recent years, the company has experienced growth stagnation and declining profitability due to US FDA issues affecting both the company and its key client in the API segment.

The company's pipeline of new molecules offers significant growth potential, with a single successful molecule poised to elevate the company to unprecedented levels over the next five years.

🇮🇳 The Beat Ideas: Gujarat Flurochemicals 2.0: From Fluoropolymer Powerhouse to Battery Technology (Smartkarma) $

Gujarat Fluorochemicals Ltd (NSE: FLUOROCHEM / BOM: 542812) is executing a INR 6,000 crore capex plan through FY28 to expand into battery materials, fluorospecialties etc. with commercial production of Battery Chemicals expected to start in Q4 FY25.

This marks a strategic shift from a cyclical chemicals business to a high-margin, clean energy materials play positioning GFL at the core of the EV value chain as China+1 sourcing.

Company is becoming a structural clean-tech growth story. The business could double its revenue base and become global EV materials supplier over the next 3-4 years.

🇮🇳 Copper Up 26% YoY, Now at All-Time Highs – Key Drivers (Smartkarma) $

Hindustan Copper (NSE: HINDCOPPER / BOM: 513599) India’s only pure-play copper miner – could see earnings surge >60% if current price buoyancy sustains.

Copper rally appears drive by fundamentals with several large miners such as Freeport-McMoRan Inc (NYSE: FCX), BHP Group (NYSE: BHP) and Anglo American Plc (LON: AAL / JSE: AGL / OTCMKTS: NGLOY) guiding declines.

Mining costs are largely location-specific and track inflation trends, supporting significant topline buoyancy.

🇮🇳 Hindustan Zinc (HZ IN) Silver Rally Is a Sweetener (Smartkarma) $

Hindustan Zinc Ltd (NSE: HINDZINC / BOM: 500188) is set to see significant earnings upgrades driven surge in silver prices (40% EBITDA share), local currency weakness and benign costs.

Planning for major US$2-2.5b growth expenditure to double output over next 3=5 years.

Valuations: Entering a strong earnings upgrades cycle. Stock can re-rate despite trading at slight premium to historic averages. Stake sales by key holders is a risk.

🇮🇳 Eicher Motors (EIM IN) | Why Exports Are on Fire (Smartkarma) $

Eicher Motors (NSE: EICHERMOT / BOM: 505200), through its brand Royal Enfield, is experiencing strong export performance driven by strategic global expansion in the middleweight motorcycle segment.

The unit in Thailand, serves as a key manufacturing hub, with a CKD assembly facility supporting both local and Asia-Pacific markets.

Royal Enfield's focus on retro design and competitive pricing attracts customers in Europe and Brazil, filling a niche left by premium brands.

🇮🇳 The Beat Ideas: Salzer Electronics: Smart Meter Play, A Proxy to India’s Electrification Story (Smartkarma) $

Salzer Electronics Ltd (NSE: SALZERELEC / BOM: 517059) is aggressively scaling its smart meter business with INR 600–700 crore revenue targeted in FY26, aiming to sell up to 8 lakh units annually.

This diversification into B2B smart metering could double revenues, boost margins, and improve ROCE, transforming Salzer from a niche switchgear player to a full-stack energy solutions provider.

Salzer is no longer a slow-growing industrial supplier: it’s evolving into a high-growth, government-aligned, tech-driven player with strong export and R&D-led optionality.

Middle East

🇮🇱 A Quick Take on Mobilicom (Shareholdersunite Essentials)

Huge opportunity, modestly priced shares

We did provide you with our Primer and subsequent Quick Take on Mobilicom (NASDAQ: MOB), the Israeli provider of communications hardware and cybersecurity software for drones. Here are simply some additional considerations:

Europe Faces a Huge Bill to Defend Ukraine. Investors Are Thrilled.

The company won a new contract with a $4B Tier-1 supplier to the defense industry.

Mobilicom’s SkyHopper PRO & PRO Lite were added to the Defense Innovation Unit’s Blue UAS Framework, opening up a host of opportunities in the US and other countries.

🇦🇪 Yalla revenue growth returns to double-digits ahead of new gaming push (Bamboo Works)

The Middle Eastern social media company reported its strongest revenue growth in two years as it prepares to launch two new self-developed games later this year

Yalla Group (NYSE: YALA)’s revenue grew 12.2% in the fourth quarter, while its profit rose nearly 10% on cost controls and better monetization of its users

The Middle Eastern social media company is currently testing two self-developed mid-core games, which could start contributing revenue in the second half of this year

Eastern Europe & Emerging Europe

🇵🇱 Orlen: A Strategic Bet On A Balanced, Undervalued Energy Major (Seeking Alpha) $ 🗃️

🇪🇺🏛️ Orlen SA (WSE: PKN / FRA: PKY1) or Polski Koncern Naftowy ORLEN Spólka Akcyjna - Poland’s state-controlled MNC oil refiner & petrol retailer providing energy & fuel 100M+ Europeans. Biggest network of fuel stations in CEE - Poland, Germany, Czechia, Slovakia & Lithuania. 🇼 🏷️

🇵🇱 Dino Polska: Strong Execution Continues (Seeking Alpha) $ 🗃️

🇵🇱 Dino Polska (WSE: DNP / FRA: 5Y2 / OTCMKTS: DNOPY) - Nationwide network of medium-sized supermarkets. 🇼 🏷️

🇵🇱 Dino Polska: Master Capital Allocator (Compound & Fire)

Dino Polska (WSE: DNP / FRA: 5Y2 / OTCMKTS: DNOPY) is on a mission to roll-out their store plan for Poland. Cash is allocated in growth capex returning more cash in the future.

Leadership Track Record: Biernacki’s frugality is legendary—he once personally selected the cheapest basket maker for store garbage collection. His strategic vision transformed Dino from one store to 2,340, with a 2010 partnership with Enterprise Investors fueling early growth. The 2017 IPO further solidified his long-term focus, delivering a 44.2% CAGR to shareholders since then.

If you want to read more about Biernacki, I can highly recommend this article.

Latin America

🌎 MercadoLibre: Strong Growth Potential At A Cheap Valuation (Seeking Alpha) $ 🗃️

🌎 MercadoLibre (NASDAQ: MELI) - Uruguay HQ’d. The largest online commerce & payments ecosystem in Latin America. 🇼 🏷️

🌎 Liberty Latin America: WiFi Optimization And Video Enhancements Likely Stock Price Drivers (Seeking Alpha) $ 🗃️

🌎 Liberty Latin America Ltd (NASDAQ: LILA / LILAK) - Communications company. 20+ countries across Latin America & Caribbean (consumer brands Flow, Liberty, Más Móvil & BTC). 🇼

🌎 Company Snapshot: dLocal Ltd (NASDAQ: DLO) (Sabar Capital)

Unlocking Emerging Market Payments for Global Businesses

This week’s company is Dlocal (NASDAQ: DLO), a ~$2b market cap payment processor that’s focused on handling payments for global enterprise merchants in emerging markets. This is a fairly young company, having IPO-ed on the NASDAQ in 2021. Considered to be one of the “pandemic darlings”, its stock price fell from a high of $69 in 2021 to around ~$9 today, while revenues grew approximately 3x. I hope you enjoy!

Founded in 2016 and headquartered in Montevideo, Uruguay, dLocal provides a payments platform designed for global enterprise merchants operating in emerging markets. Through a single API, platform, and contract — known as the One dLocal model — the company enables businesses to seamlessly receive payments (pay-ins) and make payouts (pay-outs) worldwide.

🌎 DLocal, a new invest and investigate! (The Reservist)

$2B company that could 3x?

While I've been happy with reducing the number of companies in my portfolio, I've recently been exploring a new name that has the potential to fit my long-duration growth portfolio and is currently trading at what seems to be a very very good value to enter and investigate further.

That name is Dlocal (NASDAQ: DLO), who offer a one-stop shop payment processing solution in emerging markets from Latin America through Africa and Asia.

What interests me is that they've managed to grow their Total Payment Volume (TPV) at an astounding 92% CAGR over the past 6 years. This has been coupled with strong earnings, gross profit dollars, and EBITDA growth. The company is profitable and growing.

🇦🇷 Loma Negra: Argentina's Cement Market Is Bleeding (Seeking Alpha) $ 🗃️

🇦🇷 Loma Negra: Improving Margins Leave A Note Of Optimism In The Face Of An Imminent Acquisition (Seeking Alpha) $ 🗃️

🇦🇷 Loma Negra Compañía Industrial Argentina Sociedad Anónima (NYSE: LOMA) - Production & commercialization of cement in Argentina. 🇼 🏷️

🇦🇷 Grupo Supervielle: A High-Growth, High-Risk Position On Argentina's Banking Sector (Seeking Alpha) $ 🗃️

🇦🇷 Grupo Supervielle SA (NYSE: SUPV) - Provides a range of financial & non-financial services. 🏷️

🇦🇷 Central Puerto: Energy In Evolution, Looking To The Future (Seeking Alpha) $ 🗃️

🇦🇷 Central Puerto (NYSE: CEPU) - Makes investments in the national & international energy market. 🏷️

🇧🇷 PagSeguro: Undervalued Fintech In Cheap Brazil (Seeking Alpha) $ 🗃️

🇧🇷 PagSeguro Digital (NYSE: PAGS) 🇰🇾 - Financial services & digital payments. 🇼 🏷️

🇧🇷 StoneCo Q4 Preview: A Low Bar And A High Reward Play (Seeking Alpha) $ 🗃️

🇧🇷 StoneCo Ltd (NASDAQ: STNE) 🇰🇾 - Fintech. Financial technology & software solutions to merchants for eCommerce.

🇧🇷 Nu. Servicing the Underserved! Equity Research Part! 1/3 (Global Equity Briefing)

The Story of Nu Holdings (NYSE: NU) and Business Model

By 2023, in large part thanks to Nu, the number of unbanked people had fallen to 91 million, 21% of the adult population!

In this 3-part Deep Dive, I will tell you why I think Nu is one of the most promising long-term investments in the market!

In Part 1, I will tell you their origin story, and explain Nu’s business model.

Part 2 will tackle challenges and competition.

I will close out this Deep Dive in Part 3 by taking a look at their opportunities, financials, and valuation!

🇧🇷 JBS S.A. Q4 Preview: I Need To Get More Details On Operations In 2025 (Seeking Alpha) $ 🗃️

🌐 JBS SA (BVMF: JBSS3 / FRA: YJ3A / OTCMKTS: JBSAY) - Largest meat processing enterprise in the world. 🇼

🇧🇷 Ultrapar Q4: Still Not Convincing, But The Case Has Improved (Rating Upgrade) (Seeking Alpha) $ 🗃️

🌐 Ultrapar Participaçoes (NYSE: UGP) - Energy & logistics infrastructure conglomerate. 🇼

🇧🇷 Petrobras' Valuation Hides Potential (Seeking Alpha) $ 🗃️

🇧🇷 Petrobras: Everything Is In Place, But The Price (Seeking Alpha) $ 🗃️

🌐🏛️ Petrobras (NYSE: PBR / PBR-A / BCBA: PBR / PETR4) or Petróleo Brasileiro SA - Explores, produces & sells oil & gas. 🇼

🇨🇴 🇨🇦 Parex Resources: Prudent Guidance, Strong Rerating Potential (Seeking Alpha) $ 🗃️

🇨🇴 Parex Resources (TSE: PXT / FRA: QPX / OTCMKTS: PARXF) - Largest independent exploration & production company in Colombia. 🏷️

🇲🇽 Grupo Bimbo Appears To Be Going Nowhere Fast (Seeking Alpha) $ 🗃️

🌐 Grupo Bimbo SAB de CV (BMV: BIMBOA / FRA: 4GM / OTCMKTS: GRBMF / BMBOY) - Largest baking company in the world & a relevant participant in snacks. 🇼 🏷️

🇲🇽 America Movil Is Finally Turning A Corner (Seeking Alpha) $ 🗃️

🌎 America Movil SAB de CV (NYSE: AMX) - Leading Latin America telecommunication service provider. 🇼 🏷️

🇲🇽 Aeroportuario Del Sureste Stock Remains Extremely Undervalued (Seeking Alpha) $ 🗃️

🇲🇽 🇵🇷 🇨🇴 Grupo Aeroportuario del Sureste (ASUR) (NYSE: ASR) - operates 9 airports in the southeast of Mexico + the main airport in San Juan, Puerto Rico & six airports in Colombia. 🇼 🏷️

🇵🇦 Bladex's Growth Cannot Offset Spread Contraction And Cycle Risks; Moving To Hold (Seeking Alpha) $ 🗃️

🌎 Banco Latinoamericano (NYSE: BLX) or the Foreign Trade Bank of Latin America or Bladex - Founding shareholders were the Central Banks & government entities of 23 countries in the region. Specialized in addressing trade finance needs. 🇼 🏷️

Global

🌐 Nebius: Small Fish In A Big Pond (Seeking Alpha) $ 🗃️

🌐 Nebius Group NV (NASDAQ: NBIS) - AI-centric cloud platform built for intensive AI workloads. Sold Yandex to a consortium of Russian investors. Retains several businesses outside of Russia. 🇼 🏷️

🌐 Nebius: Under The Radar AI Infrastructure Stock Poised For 600% Revenue Growth! (Capitalist-Letters)

Market still ignores it but institutions doubled their position last quarter.

Here are some metrics for you:

No debt with near $2.5 billion cash on hand.

Investing $1 billion in growth this year.

It is set to quadruple capacity by 2026.

And lately management has publicly confirmed that the annual recurring revenue is on course to increase sixfold this year…

So, let me cut the BS and dive deep into this gem!

In February 2024, Yandex N.V. agreed to sell its Russian businesses—about 95% of its revenue—for $5.4 billion to a Russian consortium called Consortium. They paid $2.5 billion in cash and the rest in Yandex shares.

Yet, Arkady kept the international assets — most notably the data center in Finland and Yandex Cloud.

Post divestment, the Dutch parent company —Yandex NV— changed its name to Nebius and got the ticker NBIS in Nasdaq.

🌐 EP103: Market Shakeups & Hidden Value—12 Stocks to Watch Now (Elevator Pitches) $

Greenhaven Road Capital started a new position in Delivery Hero (ETR: DHER / FRA: DHER / OTCMKTS: DLVHF), the German-headquartered food delivery company. Their thesis is quite simple: the market is giving multiple pieces of the business away for free. Greenhaven provides much more depth in their latest investor letter, which we include below.

📅 Earnings Calendar

Note: Investing.com has a full calendar for most global stock exchanges BUT you may need an Investing.com account, then hit “Filter,” and select the countries you wish to see company earnings from. Otherwise, purple (below) are upcoming earnings for US listed international stocks (Finviz.com):

📅 Economic Calendar

Click here for the full weekly calendar from Investing.com containing frontier and emerging market economic events or releases (my filter excludes USA, Canada, EU, Australia & NZ).

🗳️ Election Calendar

Frontier and emerging market highlights (from IFES’s Election Guide calendar):

GreenlandGreenland Diet2025-03-11 (d) Confirmed 2021-04-06Cayman Islands Referendum 2025-04-30 (d) Confirmed

Cayman Islands Cayman Legislative Assembly 2025-04-30 (d) Confirmed 2021-04-14

Romania Romanian Presidency 2025-05-04 (d) Confirmed 2024-12-08

Philippines Philippine Senate 2025-05-12 (d) Confirmed 2022-05-09

Philippines Philippine House of Representatives 2025-05-12 (d) Confirmed 2022-05-09

Poland Polish Presidency 2025-05-18 (d) Confirmed 2020-07-12

Venezuela Venezuelan National Assembly 2025-05-25 (d) Date not confirmed 2020-12-06

Macau Chinese Legislative Council (Macau) 2025-09-21 (t) Date not confirmed 2021-09-12

Côte d'Ivoire Ivorian Presidency 2025-10-25 (d) Confirmed 2020-10-31

Argentina Argentinian Chamber of Deputies 2025-10-26 (t) Date not confirmed 2023-10-22

Argentina Argentinian Senate 2025-10-26 (t) Date not confirmed 2023-10-22

Czech Republic Czech Chamber of Deputies 2025-10-31 (t )Date not confirmed 2021-10-08

Chile Chilean Chamber of Deputies 2025-11-16 (d) Confirmed 2021-11-21

Chile Chilean Presidency 2025-11-16 (d) Confirmed 2021-12-19

Chile Chilean Senate 2025-11-16 (d) Confirmed 2021-11-21

Singapore Singaporean Parliament 2025-11-30 (t) Date not confirmed 2020-07-10

Hong Kong Hong Kong Legislative Council 2025-12-31 (t) Date not confirmed 2021-09-05

📅 Emerging Market IPO Calendar/Pipeline

Frontier and emerging market highlights from IPOScoop.com and Investing.com (NOTE: For the latter, you need to go to Filter and “Select All” countries to see IPOs on non-USA exchanges):

Baiya International Group BIYA Cathay Securities/ Revere Securities, 2.5M Shares, $4.00-6.00, $12.5 mil, 3/17/2025 Week of

(Incorporated in the Cayman Islands)

We, Baiya International Group Inc. (“Baiya”), are an offshore holding company. As a holding company, we have no material operations and conduct all of our operations in China through the VIE, Shenzhen Gongwuyuan Network Technology Co., Ltd. (“Gongwuyuan”), and its subsidiaries, collectively, “PRC operating entities”. We entered into a series of Contractual Arrangements with the VIE and certain shareholders of Gongwuyuan, and this structure involves unique risks to investors. See “Risk Factors — Risks Relating to Doing Business in China” for more information. Neither we nor our direct and indirect subsidiaries own any equity interests in the PRC operating entities.

Gongwuyuan started to provide job matching services in 2017. In November 2019, Gongwuyuan began developing its cloud-based internet platform to provide one-stop crowdsourcing recruitment and SaaS-enabled HR solutions on the Gongwuyuan Platform to supplement its offline job matching services and started to position itself as a SaaS-enabled HR technology company by introducing its Gongwuyuan Platform in the flexible employment marketplace. We have been and will continue to strategically develop and improve the Gongwuyuan Platform with product features that work together with our traditional offline service model to improve the job matching and HR related services in the flexible employment marketplace.

Currently our business focuses on four (4) primary services: (i) job matching services; (ii) entrusted recruitment services; (iii) project outsourcing services; and (iv) labor dispatching services in the flexible employment market within China, primarily in the core manufacturing regions including the Pearl River Delta and Yangtze River Delta region. With respect to labor dispatching services, however, we are strategically reducing this service, considering the negative gross profit historically. Gongwuyuan plans to pursue its business growth by continuing to supplement its existing offline service model by introducing and integrating its Gongwuyuan Platform to provide better services in the flexible employment market throughout China. In addition, we plan to improve our services by continuing to develop and integrate digital technologies including crowdsourcing, big data and artificial intelligence to enhance the Gongwuyuan Platform. We believe these efforts will allow us to provide sufficient job matching and one-stop SaaS-enabled HR solutions to Customers, Employing Companies and workers in the flexible employment marketplace throughout China.

Note: Net loss and revenue are for the 12 months that ended June 30, 2024.

(Note: Baiya International Group cut its IPO’s size to 2.5 million shares – down from 3.0 million shares initially – and kept the price range at $4.00 to $6.00 to raise $12.5 million, according to an F-1/A filing dated Sept. 10, 2024. In that same SEC filing, Cathay Securities was added as the “lead left” joint book-runner to work with Revere Securities.)

Epsium Enterprise Ltd. EPSM D. Boral Capital (ex-EF Hutton), 1.3M Shares, $4.00-5.00, $5.6mil, 3/17/2025 Week of

(Incorporated in the British Virgin Islands)

We are a holding company incorporated under the laws of British Virgin Islands. As a holding company with no material operation of its own, we conduct substantially all our operations through an indirect Macau subsidiary, Companhia de Comercio Luz Limitada in Macau, or Luz. Luz is an 80%-owned subsidiary of Epsium Enterprise Limited in Hong Kong, or Epsium HK. Mr. Son I Tam, our CEO, CFO, Chairman, principal shareholder, and the founder of Epsium and Luz directly holds (i) 89.996% ownership interest in Epsium, (ii) 19% interest in Epsium HK, and (iii) 20% ownership interest in Luz.

Luz is an import trading and wholesaler of primarily alcoholic beverages in Macau. Through Luz, we import and sell a broad range of premium beverages, primarily alcoholic beverages and, in 2022, a small quantity of tea and fruit juice. The alcoholic beverages we sell include Chinese liquor, French cognac, Scottish whiskey, fine wine, Champagne, and other miscellaneous beverage alcohol. Sales of Chinese liquor is by far our most significant operations, and we are a top wholesaler of high-end Chinese liquor in Macau. We operate only in Macau.

Note: Net income and revenue are for the 12 months that ended June 30, 2024.

(Note: Epsium Enterprise Ltd. updated its F-1/A filing on March 10, 2025, to disclose that D. Boral Capital (ex-EF Hutton) is the sole book-runner. Benjamin Securities is no longer involved as an underwriter, according to the updated F-1/A filing. Epsium Enterprise’s IPO terms remain the same: 1.25 million shares at a price range of $4.00 to $5.00 to raise $5.63 million.)

(Note: Epsium Enterprise Ltd. increased its IPO’s size to 1.25 million shares – up from 1.0 million shares – and cut the price range to $4.00 to $5.00 – down from $5.00 to $7.00 – to raise $5.63 million, according to an F-1/A filing dated Feb. 3, 2025.)

(Note: Epsium Enterprise Ltd. made a change in its joint book-running team, according to an F-1/A filing dated Jan. 8, 2025: D. Boral Capital (formerly known as EF Hutton) was named as a joint book-runner, replacing Prime Number Capital, to work with Benjamin Securities. Background: This is a micro-cap IPO – just 1.0 million shares at a price range of $5.00 to $7.00 to raise $6.0 million.)

FatPipe FATN D. Boral Capital (ex-EF Hutton), 0.7M Shares, $5.75-7.75, $5.0 mil, 3/17/2025 Week of

We provide enterprises with network software solutions. (Incorporated in Utah)

We offer secure software-defined wide area network (SD-WAN) solutions to enterprises, communication service providers, security service providers, government organizations and middle-market companies. We provide a reliable and secure platform to support mission-critical applications running on cloud, hybrid cloud and on-premise networks. We serve customers in the U.S. and India. We plan to expand throughout North America and in Southeast Asia.

Note: Net income and revenue are for the 12 months that ended Sept. 30, 2024.

(Note: FatPipe Inc. filed its S-1/A on Feb. 3, 2025, and disclosed its IPO’s terms: 0.74 million shares (740,740 shares) at a price range of $5.75 to $7.75 to raise $5.0 million, if priced at the $6.75 mid-point of its range. In that filing, FatPipe named D. Boral Capital as its sole book-runner, replacing Roth Capital Partners as the book-runner and Craig-Hallum as the co-manager. Background: FatPipe filed its S-1 without disclosing the terms for its IPO on July 2024. Estimated IPO proceeds were about $15.0 million. Background: The company submitted confidential IPO documents to the SEC on Oct. 10, 2023.)

Top Win International Ltd. TOPW Dominari Securities/ Revere Securities, 2.7M Shares, $4.00-6.00, $13.3 mil, 3/17/2025 Week of

Through our Operating Subsidiary in Hong Kong, Top Win International Trading Limited, we are a wholesaler engaged in trading, distribution, and retail of luxury watches of international brands.

As the purveyor of fine watches, we source luxury products directly or indirectly from authorized dealers, distributors, and brand owners, located in Europe, Japan, Singapore, and other locations, and sell them to our customers, comprising independent watch dealers, watch distributors, and retail buyers within the watch industry. Our strategic location in Hong Kong positions us advantageously within the Asia-Pacific luxury market. This region has seen significant growth in demand for luxury goods, driven by rising disposable incomes and a growing appreciation for high-quality, branded products. We currently offer a selection of over 30 internationally renowned watch brands, including Blancpain, Breguet, Cartier, Chopard, Hermes, IWC, Jaeger, Rolex, Omega, and Longines. We primarily trade watches within the price range of $1,900 to $7,500 with our target customers being middle to high-income earners.

Note: Net loss and revenue are in U.S. dollars for the 12 months that ended June 30, 2024.

(Note: Top Win International Ltd. is offering 2.664 million shares at a price range of $4.00 to $6.00 to raise $13.325 million, according to its F-1/A filing dated March 10, 2025.)

Waton Financial Ltd. WTF Cathay Securities, 5.0M Shares, $4.00-6.00, $25.0 mil, 3/17/2025 Week of

We are a holding company. (Incorporated in the British Virgin Islands)

We are a provider of securities brokerage and financial technology services primarily through our Hong Kong subsidiaries, Waton Securities International Limited, or WSI, and Waton Technology International Limited, or WTI.

WSI is principally engaged in the provision of (i) securities brokerage services for securities listed on the Hong Kong Stock Exchange, including shares under the Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect, the New York Stock Exchange (NYSE) and the Nasdaq Stock Market, margin financing services and other ancillary services through WSI’s electronic trading platform to its corporate and individual brokerage customers and bond distribution services; and (ii) software licensing and related support services including the licensing of trading platform APP, upgrades and enhancements, maintenance and other related services to financial institutions. Since September 2023, WTI has provided software licensing and related support services in order to focus on the expertise of operations and service areas. WSI has developed and provided Broker Cloud solutions to securities brokers with the combination of software licensing and related support services, securities brokerage services, margin financing services and other related services, where securities broker customers are provided with a perpetual on-premise licensed trading platform APP and optional related support services, with the front-, middle- and back-office operation functions and securities trading function where securities trading orders can be cleared and settled through WSI.

Founded in 1989, WSI is an established integrated securities broker in the Hong Kong financial services industry. WSI is licensed to conduct Type 1 (dealing in securities), Type 4 (advising on securities), Type 5 (advising on futures contracts) and Type 9 (asset management) regulated activities under HKSFO in Hong Kong. WSI is a Hong Kong Stock Exchange participant and holds one Hong Kong Stock Exchange trading right. WSI provides securities brokerage services through WSI’s integrated electronic trading platform, which is easy to access, use, and deposit to WSI’s customers. The trading platform can be accessed through WSI’s APP, which provides WSI’s customers with a seamless and secured trading experience. WSI offers its customers comprehensive brokerage and value-added services, including trade order placement and execution, account management, and customer support. WSI further provides its customers with market data, news and research, so as to help them make well-informed investment decisions. WSI has accumulated a corporate and individual customer base across the globe, including a securities brokerage company in New Zealand known as Wealth Guardian Investment Limited (“WGI”), which is a related party of the Company. We derived a substantial portion of revenues from WGI, which accounted for approximately 39.5% and 81.5% of our total revenues in the fiscal years ended March 31, 2024 and 2023, respectively, and approximately 68.0% and 98.2% of our total revenues for the six months ended September 30, 2024 and 2023, respectively. See “Related Party Transactions” and “Risk Factors — Risks Related to Our Subsidiaries’ Business and Industry — We derived a substantial portion of revenue from WGI, a single related party customer”. By capitalizing on its customer base, WSI commenced to provide bond distribution services by acting as a manager, a placement agent or a non-syndicate capital market intermediary, to procure subscribers to subscribe and pay for bonds in principal amounts during the fiscal year ended March 31, 2024 and for the six months ended September 30, 2024. As of September 30, 2024, WSI had more than 5,800 securities brokerage customers who opened trading accounts with WSI, 59 of which are corporate customers who opened corporate accounts and three of which are introducing broker customers who opened omnibus accounts. The remaining portion of the securities brokerage customers are individual customers whoopened individual accounts and typically trade through WSI’s trading platform APP. As of the same date, WSI had over 600 active customers, who were registered customers with assets in their trading accounts. We generate brokerage and commission income from WSI’s securities brokerage, bond distribution and other ancillary services and interest income from WSI’s margin financing services, and our brokerage and commission income and interest income which amounted to approximately US$9.4 million and US$2.3 million, and accounted for approximately 93.4% and 39.9% of our total revenues, for the fiscal years ended March 31, 2024 and 2023, respectively, and amounted to approximately US$1.8 million and US$1.9 million, and accounted for approximately 61.3% and 83.7% of our total revenues, for the six months ended September 30, 2024 and 2023, respectively.

Leveraging on WSI’s accumulated industry knowledge on the needs of small and medium-sized securities brokers and operational experience in online brokerage over the years, WSI started to develop the provision of fintech solutions in trading platform APP software licensing and related support services targeting the securities brokers and securities-related financial institutions in April 2021. We are a pioneer of business-to-business fintech services in the Asia-Pacific region to offer one-stop brokerage software solutions to small and medium-sized brokers, according to Frost & Sullivan Limited, or Frost & Sullivan. WSI provides one-stop, integrated and customized software solutions to develop trading platform APP that covers the front-, middle- and back-office operations of securities brokerage business such as electronic trade order placing, customer relationship management and operational data management, in addition to the business-to-business securities order clearing and settlement services provided by WSI in the Broker Cloud solutions, which enables the securities broker customers to digitalize and streamline their business operations, and interact with the financial market more efficiently. As of September 30, 2024, March 31, 2024 and 2023, WSI and WTI provided software licensing and related support services to a total of five, three and five securities brokers and securities-related financial institutions, respectively, including WGI, which is a related party of the Company. See “Related Party Transactions” and “Risk Factors — Risks Related to Our Subsidiaries’ Business and Industry — We derived a substantial portion of revenue from WGI, a single related party customer”. We generate software licensing and related support service income from WSI’s and WTI’s software licensing and related support services, which amounted to approximately US$1.4 million and US$3.5 million, and accounted for approximately 13.7% and 60.1% of our total revenues for the fiscal years ended March 31, 2024 and 2023, respectively, and amounted to approximately US$1.1 million and US$0.7 million, and accounted for approximately 38.7% and 29.0% of our total revenues, for the six months ended September 30, 2024 and 2023, respectively. WSI and WTI have outsourced the software licensing and related support services to Shenzhen Jinhui Technology Co., Ltd., a related party of the Company. See “Related Party Transactions” and “Risk Factors — Risks Related to Our Subsidiaries’ Business and Industry — WSI and WTI are dependent on a single related party supplier, Shenzhen Jinhui Technology Co., Ltd., an information technology company and a related party controlled by Mr. Zhou Kai, our Chairman of the Board, Director, Chief Technology Officer and shareholder, for providing software development and related support services”.

Note: Net income and revenue are for the 12 months that ended Sept. 30, 2024.

(Note: Waton Financial Ltd. is offering 5.0 million shares at a price range of $4.00 to $6.00 to raise $25.0 million.)

WF Holding Ltd. WFF Dominari Securities/ Revere Securities, 2.0M Shares, $4.00-6.00, $10.0 mil, 3/17/2025 Week of

We are a holding company whose business is conducted by Win-Fung, our wholly owned subsidiary in Malaysia. (Incorporated in the Cayman Islands)

We are a manufacturer of fiberglass reinforced plastic, or FRP, products based in Malaysia. For over 30 years, we have been providing high-quality and durable FRP products to various industries, including, among others, chemical processing, water and wastewater treatment, and power generation.

We sell a broad range of FRP products, including filament wound and molded tanks, thermoplastic tanks, lining products, pipes, ducting and fitting products, air pollution control equipment, gratings and other custom-made products. We also offer delivery, installation and repair and maintenance services, as well as on-site consultation services.

We use advanced production technology and equipment and have obtained various certifications, including an ISO 9001:2015 certification from NQA. Our manufacturing capabilities allow us to design and fabricate products that meet the specific needs of our clients, ensuring high-quality and reliable performance.

FRP is a composite material made up of a polymer that is reinforced with fibers. In general, the polymers used include epoxy, vinyl ester and polyester, while the fibers used include glass, carbon, aramid and basalt. The combination of fibers and polymers provide FRP with unique properties such as high strength, stiffness and durability. This has enabled FRP to be utilized in a wide and diverse range of industries and applications, including the construction, aerospace, marine, electrical, as well as chemical industries.

Within the construction industry, FRP is used in the manufacture of panels, roofing, cladding and reinforcement bars. In the automotive industry, FRP can be used in applications such as making body panels, bumpers, and spoilers. FRP is used in making aircraft parts such as wings, fuselage, and tail sections in the aerospace industry, while in the marine industry, FRP is utilized in making the body parts of boats, yachts and ships. In the electrical industry, FRP can be used for making insulators, transformers, and switchgear. FRP is also used in applications in the chemical industry including making storage tanks, pipes and ducts.

FRP is used in a growing number of applications across various industries. Designs that require lighter materials, precision engineering with higher tolerances or even simple components have increasingly been manufactured using FRP. These FRP products are cheaper, faster and easier to manufacture than cast aluminum or steel, and often have better tolerance and material strength. At the same time, FRP is also ideal for designs that require higher strength than that of non-reinforced plastics.

We sell a broad range of FRP products, including filament wound and molded tanks, thermoplastic tanks, lining products, ducting and fitting products, air pollution control equipment and custom made products. We also offer delivery, installation and repair and maintenance services, as well as on-site consultation services.

Note: Net income and revenue are in U.S. dollars for the 12 months that ended June 30, 2024.

(Note: WF Holding Ltd. is offering 2.0 million shares at a price range of $4.00 to $6.00 to raise $10.0 million, according to its F-1/A filings. Dominari Securities and Revere Securities are the joint book-runners; they replaced Pacific Century Securities, the original sole book-runner for this deal. Background: WF Holding Ltd. filed its F-1 for its IPO on Sept. 23, 2024, without disclosing the terms. Estimated proceeds are $10.0 million. Background: WF Holding Ltd. submitted confidential IPO documents to the SEC on Jan. 24, 2024.)

J-Star Holding Co., Ltd. YMAT Maxim Group, 1.3M Shares, $4.00-5.00, $5.6 mil, 3/24/2025 Week of

As a holding company with no material operations of our own, our operations are conducted through our subsidiaries in the People’s Republic of China (the “PRC”), Taiwan, Hong Kong and Samoa, with our headquarters in Taiwan, and such structure involves unique risks to investors, as the Chinese government may exercise significant oversight and discretion over the conduct of our business and may intervene in or influence our operations at any time. (Incorporated in the Cayman Islands)

Our Predecessor Group was established in 1970 and we have accumulated over 50 years know-how in material composite industry. We develop and commercialize the technology on carbon reinforcement and resin systems. With decades of experience and knowledge in composites and materials, we are able to apply our expertise and technology on designing and manufacturing a great variety of lightweight, high-performance carbon composite products, ranging from key structural parts of electric bicycles and sports bicycles, rackets, automobile parts to healthcare products. According to the industry report commissioned by us and prepared by Frost & Sullivan, we are one of the major global leading players in the carbon fiber bicycle parts industry and carbon fiber racket parts industry.

We primarily generate revenue through three divisions and revenue streams, namely (i) sales of bicycles parts of sports bicycle and electric bicycle; (ii) sales of rackets for use in tennis, badminton, squash and beach tennis; and (iii) sales of other products, which mainly include structural parts of automobile, other sporting goods and healthcare products. Our bicycle parts and rackets are mainly supplied directly or indirectly to branded customers located in Switzerland, France, Italy, the Netherlands, Germany and Japan and they market and distribute their products worldwide. Other customers who rely on our new products, such as automobile parts and healthcare products, are mainly located in Australia, Canada and Japan.

*Note: Net income and revenue are for the 12 months that ended June 30, 2024.

(Note: J-Star Holding Co. Ltd. cut its IPO’s size to 1.25 million shares – down from 2.0 million shares – and kept the price range at $4.00 to $5.00 – to raise $5.63 million in an F-1/A filing dated Aug. 2, 2024; in that same filing, the company said that Maxim Group is the new sole book-runner, replacing EF Hutton. Background: J-Star Holding Co. Ltd. reduced the size of its IPO again – to 2.0 million shares – down from 2.5 million shares – and kept the price range at $4.00 to $5.00 – to raise $9.0 million in an F-1/A filing dated June 13, 2024. In that June 13, 2024, filing, J-Star Holding Co. Ltd. disclosed that EF Hutton is the new sole book-runner, replacing the previous joint book-running team of Maxim Group LLC and Freedom Capital Markets.)

(Background: J-Star Holding Co. Ltd. cut its IPO to 2.5 million shares – down from 4.0 million shares – and kept the price range at $4.00 to $5.00 – to raise $11.25 million, according to an F-1/A filing dated Sept.19, 2023.)